Market Update: Winners and losers of stabilising yields

Breadth of equity rally broadens beyond the US Mega Techs, 28 February 2024

Winners and losers of stabilising yields

The ECB meets this week, and the BoE in two weeks’ time. Interest rate and yield volatility has calmed amid signs that some can now bear the cost of new debt. Is this a sign that we’ve reached an equilibrium?

February 2024 asset returns review

The fourth good month in a row for global investors, saw stabilising bond yields and a broadening of the stock market upturn, but also a slowing G7 economies and talk of nervous optimism

Nigeria shows why reform is always difficult

Politicians and the central bank are applying some textbook remedial policies and some newer policies devised to cope with the population’s involvement with cryptocurrencies. Can they arrest the capital outflow and give themselves time for the reforms to bear fruit?

Winners and losers of stabilising yields

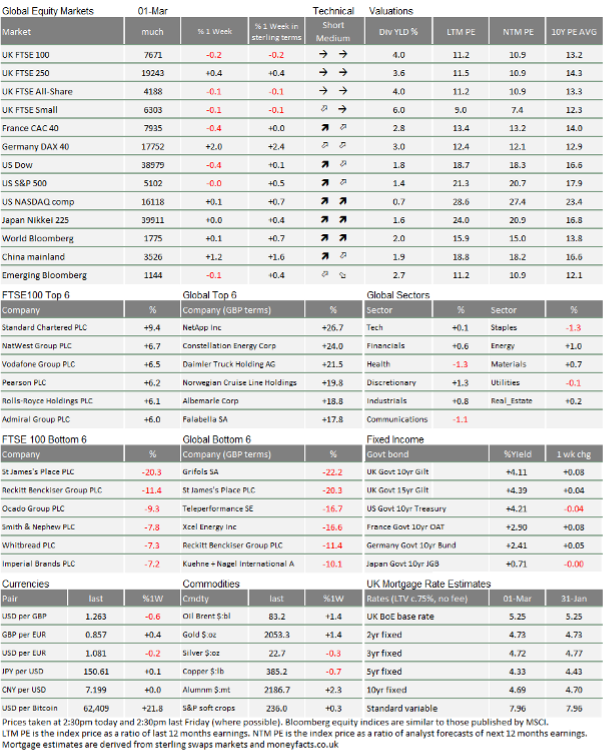

We ended February and start March with a week of positive price action in equities, although the US mega-caps did less well generally, while bond markets were rather stable. Indeed, we think stable bond markets – pretty much since the beginning of the year – are one of the reasons why equity markets can continue to edge up. Interest rates and yields appear close to equilibrium levels, a state of relative steadiness which enables activity to happen. However, these new equilibrium levels are not comfortable for everyone, and that difference seems to be driving change.

There was also another sharp rise in Bitcoin. This may be related to new US exchange-traded funds which are now allowed to invest in cryptocurrencies, although there is also an interesting link to weakness in the Nigerian currency, the naira, and its central bank’s actions to try to stem capital outflow.

There were no big mergers or acquisitions last week, but the spate from the previous week has raised expectations of more to come. It is also noticeable that companies are increasingly trying to raise equity rather than loan capital. Bloomberg pointed out that companies are finding the near-term cost of equity much more bearable now that dividend yields have fallen in relation to bond yields. While the longer-term cost of equity might be high, the improvement in balance sheet metrics in terms of credit quality is often welcomed by investors who would usually complain about dilution.

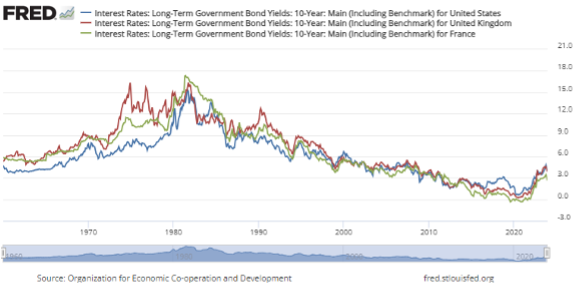

Interest rates and bond yields have stabilised, but are high, certainly compared to much of the 2010-2020 period. However, in the general scheme of history, they are very average. The graph below shows how yields have evolved here in the UK (red), in France (green) and in the US (blue) since 1960. The 10-year gilt is trading at a yield of 4.17% as we write, which is below the 6% levels prevalent through most of the 1960s before we got into the inflationary days of the 1970s.

Growth was higher in that period in Europe, as we went through the post-war rebuild. In the US, despite strong growth, yields were around the 4%-5% level, but rarely lower.

In the UK, yields averaged about 3.6% from 1785 to 1959 (according to data cobbled together by the Bank of England (BoE) in A Millennium of Macroeconomic Data for the UK, published in 2016), and ranged from 3% to 6%. Market mechanisms were much slower which may have restrained changes in rates, but there was not much volatility until we got to the 1970s.

So, although rates feel high now, they appear to be fairly normal when taking a longer view. They are a little higher than the very long-term and about in line with the past 75 years. That history gives us comfort that an economy has functioned and will function in a reasonable balance at current rates.

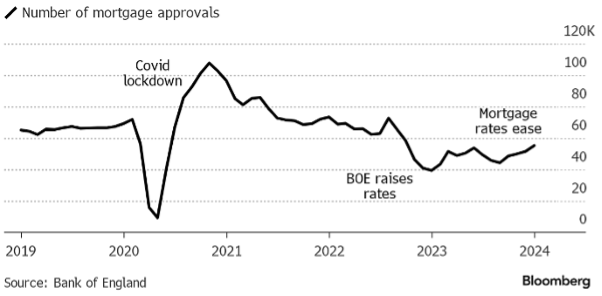

What has struck us in recent weeks is that consumer and business behaviours have become sensitive to quite small changes in rates. Small businesses are negatively sensitive and step up efforts to reduce debt on any sign of a rise. However, there is demand for debt if the interest cost comes down in the mortgage market.

Nationwide Building Society reported that the average price of a home rose to £260,420 in February, up 0.7% from January and 1.2% higher than February 2023, the first annual growth since January 2023. Meanwhile, the BoE published mortgage approval data for the previous month (January), which showed 55,227 agreed mortgages. That figure was quite a bit higher than the 52,000 consensus Bloomberg gathered. Approvals have been rising for four months, and may well get back to the pre-2020 levels as the seasonal activity increases. (It is at this point we celebrate the Met Office’s declaration that Spring starts today, although the weather forecast does not look so good for the weekend ahead).

The mortgage dynamic is very interesting. Housebuilder Taylor Wimpey released rather so-so results for the full 2023 year, doing better than expected in profit terms but with a downbeat outlook for this year. They are probably being cautious, not surprising after the general run-up in housebuilder optimism at the end of 2023. The FTSE 350 Household Goods and Home Construction Index is up from the October lows by over 30%, albeit flat this past month.

The driver has been the fallback in mortgage rates. While expectations of BoE rate cuts have diminished in the past month, the mortgage war between banks has been raging on. We track mortgage rates for the weekly data table at the end of our musings (scroll to the bottom). Swap rates are the interbank rates which define the levels at which banks borrow in order to lend to new mortgagees. These have risen slightly but the offered mortgage rates have stayed very stable. Indeed, the spreads have gone from about 1% over swap rates to less than 0.5% and, the week before last, the best offered three-year rate was the same as the three-year swap rate.

What does all this tell us?

The BoE sets the rates at which it interacts with the banks. However, we all have differing borrowing needs and different interest rates that we can bear. The collapse in spreads between the swap rates (which are closely aligned with the BoE’s target rate) and actual mortgage rates tells us (we believe) the BoE is setting rates a bit high, but not far away from the rate that normal people can bear.

Banks have had deposit balances rising, but have found there’s not much borrowing going on. If they raise mortgage rates to customers by a small amount, demand disappears. The obverse is that there’s reasonably healthy activity if they cut. They are helped in that decision to cut by the fact that the credit quality of the new borrowers is good enough to warrant lending on skinny terms. Borrowers have reasonably strong deposits and little previous borrowing; they have good ongoing income, while the outlook for house prices has stabilised.

The market has found an equilibrium rate and credit demand appears to be ‘elastic’ or price-sensitive. This is also a stable dynamic which builds healthy loan books for banks and other investors, and solid dependable growth for constructors and the economy. The need for tight lending margins also suggests there is no room for rate rises and really that rates could be lower.

This week on Thursday, the European Central Bank (ECB) conducts the first of March’s central bank meetings. Europe is in a very similar situation to the UK, and many businesses are still seeking to reduce debt levels. However, unlike in the UK, consumer/household demand for credit is low. The recent fallback in inflation will definitely spark a debate, but it is unlikely to result in any rate cut. The ECB’s researchers have published their “forward-looking wage tracker” which shows how they think wage rises are evolving on a monthly basis and thereby provides some guidance on how much inflation pressure they expect is in the pipeline. The commentary from various council members has constantly referred to still-rapidly rising wages and it does appear that the EU-wide wage growth remains around 4.5% (for comparison and perspective, the average wage growth was a little below 2% between 2011 and 2021).

The question which comes to mind is this: if wage growth is so strong, why is growth so anaemic? Inflation has now come down to 2.6% year-on-year while JP Morgan has the current real gross domestic product (GDP) growth level at -0.6% annualised. The answer is, of course, that someone in the economy is saving or, more accurately, reducing borrowing; the corporate sector continues to deleverage and private households are not picking up the slack.

We think both the BoE and ECB ought to be on the verge of rate cuts. Growth is not collapsing, but neither is it rising. By focusing on labour pricing power alone, they miss the point that it is businesses that are paying that price. It is neither being funded out of money creation not reflected in rising prices.

As we said, unfortunately for yet another month, we will analyse words, not actions.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.