Market Update: Shock, rotation, growth?

England’s football team puts paid to Biden’s re-election hopes,

Matt Pritchett, 14 July 2024

Shock, rotation, growth?

Amid shocking global events, the market rotation from large to small cap stocks continues. Will the positive effects for small caps be enough to outweigh the wealth losses for the tech giants?

Small cap rotation

We explain in more depth why investors are flocking from the ‘Magnificent 7’ to smaller US stocks: a presumed Trump victory and a shift in expected earnings momentum.

Renminbi strength is political, not economic

Given China’s weak economy, you would expect its currency to fall – but Beijing is keeping it strong. This is a political calculation more than an economic one.

Shock, rotation, growth?

Last week was an astounding week. Capital markets took the attempted assassination of Donald Trump as practical confirmation of his victory in the upcoming presidential election. Equities moved to price in his expected agenda of tax cuts and deregulation, expectations he bolstered with his speech at the Republican National Convention. Stocks of small and mid-cap US companies particularly benefitted – a continuation of the rotation that started the week before last.

Then, this morning (Friday 19th July), we saw what many are calling the largest IT outage in history. Disruption is widespread and many trading systems are down or impaired. This has inevitably caused market disruption but, as of yet, not so much price volatility. Still, some traders will be badly affected and losses will be hard to assess before IT infrastructure is back online.

Funnily enough, after the ups and downs, many stock indices have ended the historic week not far off where they started.

IT failure could hurt tech.

Thankfully, our own internal systems do not appear to be directly affected by the global IT outage. But the economic, financial and human impacts could be large. Health services, flights and financial transactions have been hit. UK financial regulators are trying to assess the scale of the problem, but it is clear that some people and firms are having difficulty accessing funds or settling trades. This increases the short-term risk in affected investment positions, since traders might be unable to close certain positions, therefore exposing them to downside they did not account for.

If the outage lasts (it is still ongoing at the time of writing), some companies could be badly affected. But one trader’s loss is another’s gain, so immediate volatility at a broad index level may be contained. After sudden shocks like this, risks can feel stark, but they are often recovered once the disruption subsides. It is likely to add some extra pressure to big tech stocks like Microsoft – whose systems are at the centre of the outage. Big tech has already been struggling over the last week, thanks to the market rotation from big to small cap. Investors appear in the mood to look for bad news regarding the mega-caps, and a global IT disaster certainly fits the bill.

As long-term investors, our focus is more on what this episode might mean for the future. While the cause seems to be a malfunction rather than any attack, we suspect more resources will go towards bolstering cybersecurity – both for companies and governments. Interestingly, we had already started looking more closely at the cybersecurity sector, following Google’s announcement of a $23 billion bid for start-up firm Wiz, and this only adds more reason. (Ironically, Wiz is only four years old; its founders sold a very similar business to Microsoft for $320 million in 2015!). One possible long-term effect could be a reduction in the openness of the global internet – analogous to the raising of international trade barriers in recent years. We will have to watch this space.

Trump’s predictions accelerate rotation.

Donald Trump surviving an assassination attempt has pushed the former president from election favoured to presumptive winner – at least according to markets’ reaction. It has done something which previously seemed impossible for the divisive Trump: make him sympathetic to undecided voters – for now at least. The narrative we are seeing is that, unlike a week ago, it now does not matter whether the Democrats stick with their unpopular president or opt for a replacement – most likely Vice President Kamala Harris (although US left-leaning media notes a strong push for Michelle Obama).

Stock prices for small and (particularly) mid cap companies have benefitted massively from the news. There is a perception that a decisive lead for Trump reduces uncertainty about what might happen in November. That might sound odd, considering that Trump is by his very nature a wild card, but markets feel confident that a second term – potentially accompanied by Republican victories in the Senate and House of Representatives – will mean another round of corporate and personal tax cuts. The Russell 2000, America’s main small-cap index, had its strongest week since 2000 in response.

We welcome this shift away from the previously dominant tech mega-caps, but have a few niggling worries about markets’ assessment. While Trump is clearly now favourite for the White House, a lot can happen before November, and it is not clear why his success should mean success for House Republicans. A second Trump term will also bring many uncertainties.

The most important from our perspective is fiscal policy and bond markets. Debt and deficits are already very stretched, and Trump would certainly look to stretch them further. This could have some nasty effects on US markets, as we discussed last week. Falling bond yields suggest that markets are not worried about this, but that could quickly change.

Is momentum the dominant driver of markets?

The large-to-small cap rotation is mostly a momentum story: small caps have gained it and the mega-caps have lost it. In fact, we have noticed over the last few years that price momentum – assets gaining/losing because investors are buoyed by previous gains/losses – has become one of the most important market drivers over the short-to-medium term. We cannot explain precisely why that is, but we suspect it has something to do with the massive growth in algorithmic trading – supported in recent years by generative AI.

AI trading might now have such a presence in stock markets that it can drive a momentum trade worth trillions into a few mega-caps – then just as easily reverse that. It is not the only explanation of course (the prevalence of retail investors, for whom recent price movements are pretty much the only accessible information, could be another). Like all areas where AI’s presence is growing exponentially, the biggest concern is that market behaviour could become increasingly detached from what anyone would reasonably expect.

Nvidia itself – the undisputed winner from the AI boom – could be a prime example. It has become one of the world’s most valuable companies after incredible share price growth, but it is ultimately a risky stock (albeit an extremely profitable one in recent years). With its historical volatility, you would normally expect investors to give Nvidia a reasonably high risk premium (the amount of return demanded for a given level of risk) but its price to the next twelve months’ expected earnings remains around 40 times.

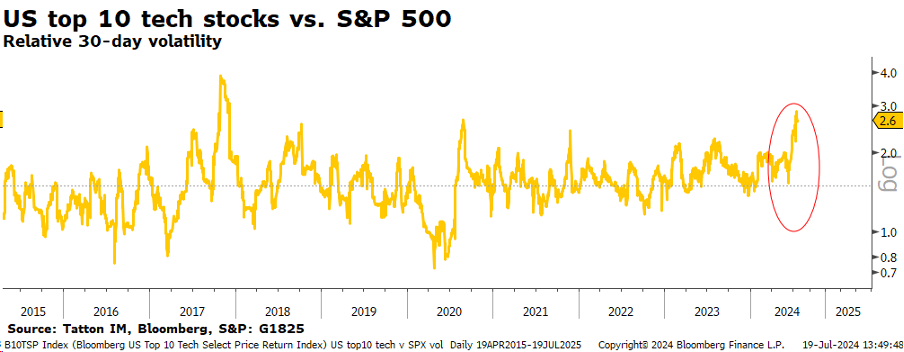

Indeed, the top ten US tech stocks have become the mainstays of the overall US market. These stocks (as calculated by Bloomberg) now form over 30% of the S&P 500, up from 10% in 2015. Yet they have also become more volatile, relative to the overall index, as the next chart shows:

Trends like that might now flip around if the great rotation continues. But one worry we have with this is that, because the mega-caps have become so huge, their losses are now outweighing the gains made by smaller caps – as we see in aggregate losses for the S&P 500. That could have a negative effect on overall market conditions, and therefore consumers (through the so-called ‘balance sheet effect’). There are still many positives, and greater market equality would be good for the long-term but, for now, we should be wary.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.