Market Update: Second half starts with wary market mood

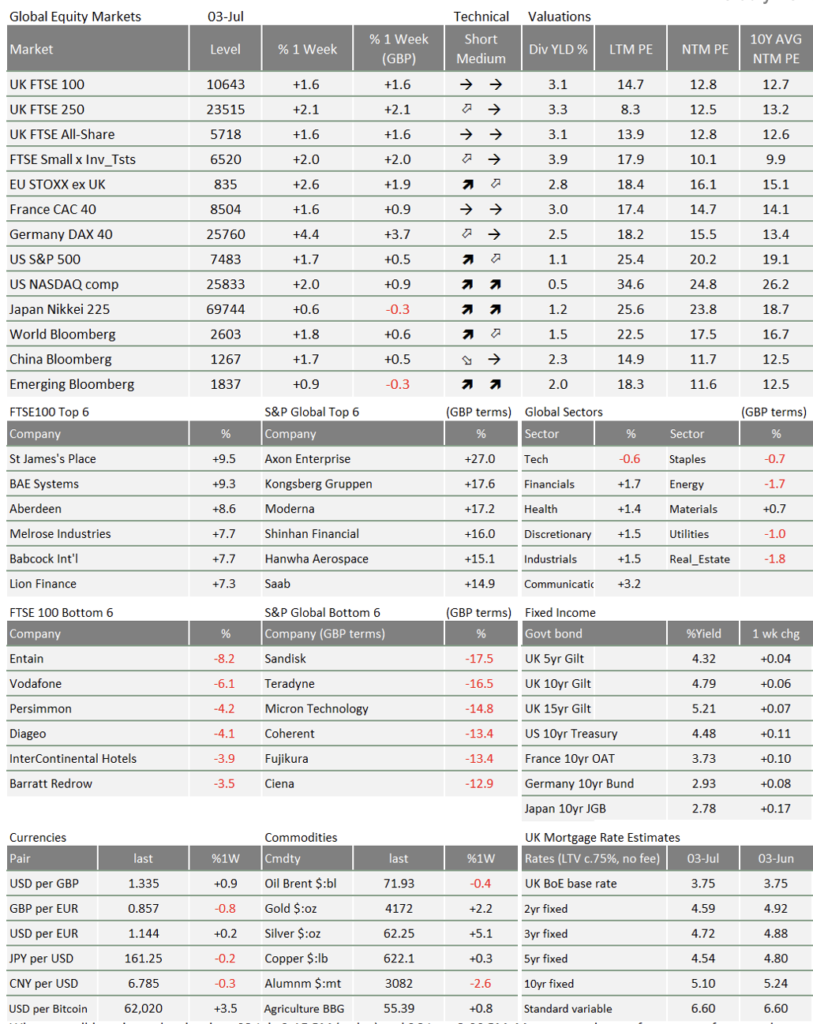

Global stocks recovered from last week’s sell-off, but are still only roughly flat from a month ago. Once again, the previous big winners – like US tech – are the most under pressure. The week before last, we put these moves down to institutional investors rebalancing their assets at the end of a strong quarter. Further pressures last week suggest something else might be going on.

There are a few explanations one could latch onto: possible cracks in the AI spending spree, and a potentially more hawkish Federal Reserve. We should not read too much into these tea leaves, however. The simpler explanation is that investors are cashing in for the summer break after a great market run.

Valuations fall because earnings gain

The stocks stalling right now are the most highly valued, in price-to-earnings terms. Falling valuations are often associated with falls in share prices, but that is not what is happening now. Instead, broad AI shares are trading sideways while AI-related earnings growth powers ahead – particularly for microchip manufacturers. Earnings growing faster than share prices brings valuations down as well, but perhaps a little more constructively for investors than through price falls. As we wrote last week, falling valuations contradict the AI bubble narrative, at least in the classic sense.

Recently, we have seen a drop-off in the momentum factor – the extent to which the previous best-performing stocks keep outperforming. Momentum has been one of the most powerful drivers of equity returns in the last two years (and especially this year), but the factor has considerably tailed off in the last week. In the US, there has been an investor rush to become more diversified, away from big tech stocks into the “lesser” large, mid and small cap companies. Notably, however, we do not see this rotation in Europe.

There is a good chance that these trends are predominantly seasonal. Market trading typically thins out in the summer months – meaning tighter effective liquidity. And the trend for the season can be set by the rebalancing at the half-year point. As we noted last week, there have been an awful lot of investment gains to crystallise in the last six months, so the current flatlining of market price action makes sense.

Nevertheless, some commentators talk of a market peak, pointing to supposed early warning signs: economic growth looks weaker than a month ago – exemplified by yesterday’s disappointing US jobs number – and investors are somewhat sceptical about the durability of AI earnings growth.

Meta has compute to spare

The key question for earnings is whether companies can keep up their AI-related capital expenditures (capex). Notably, Meta announced last week that it will sell its spare cloud computing capacity. Excess computing power is succour for the AI doomsayers; it challenges the idea that there is endless demand for compute.

We should point out that Meta’s share price jumped 9% after the announcement. For the company itself, investors took it as a decent sign that the Facebook owner will make some money out of all the billions it has spent on AI and cloud infrastructure. This continues the recent theme of markets rewarding big tech for smart, disciplined capex.

It is unclear what Meta’s news means for AI capex overall. Coming at the same time as a drop-off in tech stock momentum, it looks like a sign that AI-related earnings growth might be peaking. But we have seen false peaks before – only for tech companies to roar ahead. Computing demand is certainly one to watch, but not one to worry about yet.

The other interesting AI news last week was OpenAI’s reported offer to give the US government a 5% stake in the company, potentially garnering favour with the White House just as OpenAI’s competitors face political and regulatory headwinds. The government-big tech overlap is a fascinating story with potentially significant long-term impacts, but it is unlikely to affect markets in the short term. For now, investors are still laser-focussed on earnings.

If it walks like a hawk and talks like a hawk…

The other key aspect of the earnings-valuation debate is interest rates – with rate hikes being the stereotypical bubble burster. With falling oil prices, low core inflation and weak demand in Europe, the ECB no longer looks like it will raise rates. The Federal Reserve, by contrast, is looking increasingly hawkish (preferring higher rates). Recently appointed Fed chair Kevin Warsh spoke last week at an ECB conference in Sintra, Portugal. It was not what he said there that piqued markets’ interest, but more how he said it.

Warsh insisted on the Fed’s political independence and emphasised that anyone expecting leeway on the central bank’s 2% inflation target would be “disappointed”. If the Fed chair was picked by Donald Trump to cut rates, the statement might signal conflict ahead. At the least, Warsh appears to be looking for a fight with someone. He is reportedly tapping up former Bank of England governor Mervyn King for his new Communications Task Force. Given King’s reputation, we should interpret this as Warsh pushing ahead with his plans for a more assertive (non-)communication style at the Fed. For central banks, assertive typically means hawkish.

The hawkish tone, combined with sharply lower oil prices and (to a lesser extent) the weaker-than-expected US jobs report, has led to a fall in US inflation expectations. That has not dented growth expectations too much though, as shown in the performance of small cap stocks, but it has kept longer-dated US government bond yields below 4.5%.

Lastly, a quick word on UK government bonds (gilts). Gilt yields stayed contained last week despite Ed Miliband becoming betting markets’ clear favourite to be the next Chancellor. Miliband is, we are led to believe, gilt investors’ least favourite for the job. The fact gilts have behaved tells us that markets see the UK government as constrained more by yields themselves than politics – regardless of who is at 11 Downing Street.

From momentum and Meta to Warsh, none of last week’s stories really feel big enough to move the market needle. But in the light summer months, small stories can sometimes feel much bigger.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.