Market Update: Markets firm but fair

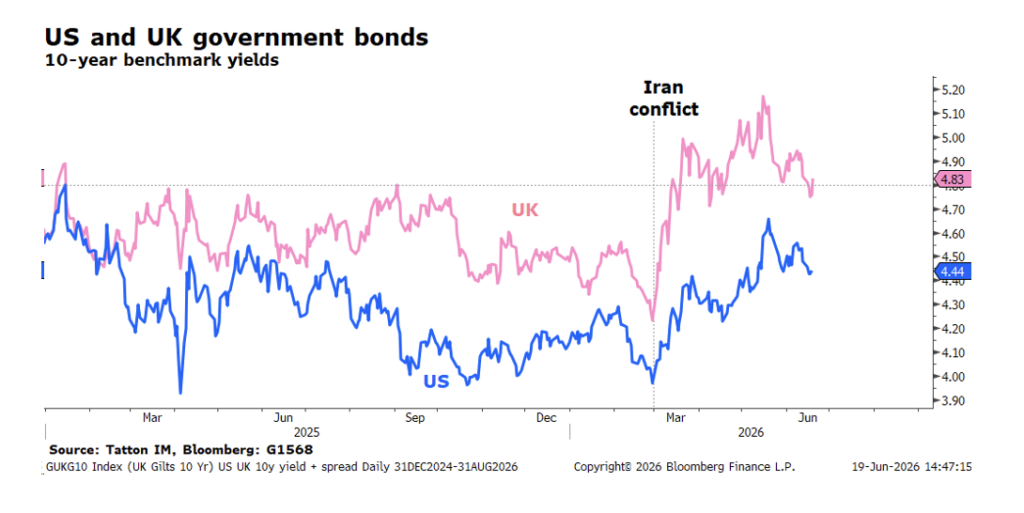

The deal between US and Iran, which extends the ceasefire and opens the Strait of Hormuz, was unequivocally good news for markets. Oil prices are sharply down, global stocks are up and long-term bond yields have calmed.

We can be sceptical about what constitutes peace or when it will really begin. The supposed signing in Switzerland was delayed after Israeli bombing in Lebanon but, as we write, Israel and Hezbollah say they have agreed a ceasefire. The situation appears fragile. However, for markets, the fact is that there has been a lessening of risks, particularly the most economically damaging risks.

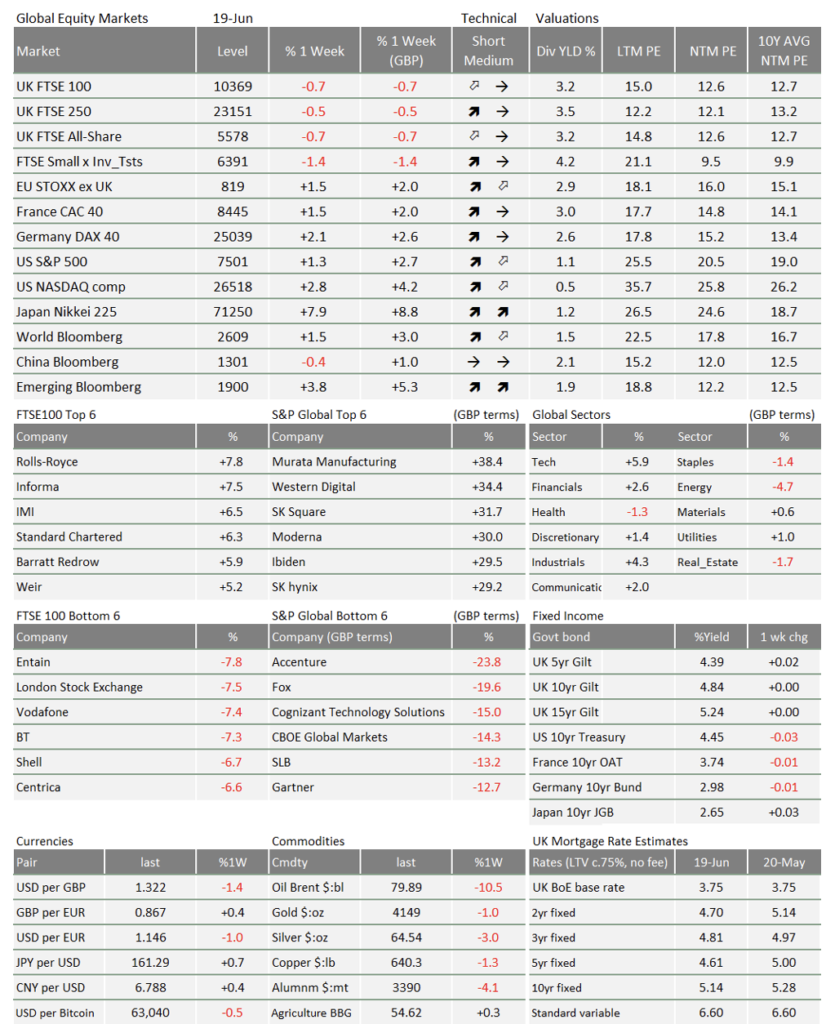

Washington’s dealmaking drove down inflation expectations, helping longer-term bonds. But US stocks were only marginally up through last week – lagging behind Europe and Japan. With Iran (apparently) in the rearview mirror, global investors turned their attention to Kevin Warsh’s debut meeting as Federal Reserve Chair.

Hard money Warsh means a harder dollar

Chairman Warsh has a clear agenda – but maybe not the agenda of the man who picked him. Donald Trump nominated Warsh because of his perceived desire for lower interest rates, and everyone wondered how that would gel with the new Fed chair’s desire to tighten central bank liquidity. It is now clear that the latter will take priority.

What we also saw in Warsh’s first meeting was a plan for reforming the way the Fed researches and communicates its policies – notably, by reducing the central bank’s forward guidance. Reforming the Fed’s research and communication will allow Warsh to control the narrative and overcome institutional blocks on his plan to reduce the Fed’s balance sheet.

We think the eventual aim is to shift the burden of money creation onto private banks, as we had before the 2008 global financial crisis and the ensuing era of Quantitative Easing. Many are sympathetic to the idea that markets should be weaned off the central bank printing press. But it would put risks back into the financial system (the ones removed by post-GFC banking reform). This is already weighing on prices of riskier assets.

The other surprising part of the meeting was the Fed’s signal that rates could go up this year. That hawkishness did not come from Warsh; the chair declined to submit a dot for the ‘dot plot’ of committee members’ rate predictions. Even with falling oil prices, policymakers are concerned about US inflation – which sent short-term bond yields higher. That is not good news for mid and small cap stocks, which rely more on bank loans.

US inflation expectations fell, long-term real (inflation-adjusted) bond yields were stable, and the dollar gained against most global currencies. All of that tells us that markets think Warsh’s ‘hard money’ approach to liquidity is off to a good start. If that is right, the dollar could be on a firmer footing than it has been for a while. That is important for investors: a weaker dollar over the last 18 months has significantly detracted from otherwise strong US equity returns.

Deal eases the BoE’s concerns

The Bank of England held rates steady in its meeting last week. Monetary Policy Committee (MPC) members were grateful for the US-Iran deal, lowering energy inflation and removing the need to hike. The UK’s employment report was not quite as weak as expected, but private sector wage gains were fairly dreary. May’s inflation figures (+2.8% year-on-year, versus +3% expected) vindicate the MPC’s feeling that underlying inflation pressures are not so bad.

UK government bonds (gilts) were one of the best performing bond markets last week, with the gap between UK and US yields shrinking substantially. As we have written before, structural imbalances in the outstanding stock of supply make gilts highly reactive – in both directions. Lower global energy prices therefore have a bigger impact on gilts than others.

We said last week that gilt traders would be watching the Makerfield by-election. Andy Burnham’s win caused a small rise in yields. But, by the time it happened, external pressures on gilts had eased up enough to make the fates of Starmer and Burnham seem relatively unimportant.

Burnham has said that he will not alter Labour’s fiscal rules if he becomes Prime Minister. Unless that drastically changes, we expect international factors will keep being more important for gilt yields than domestic politics. If oil and gas prices ease further, there is even the possibility that Burnham could enter Downing Street with greater fiscal headroom than the government has enjoyed for a while – thanks to falling yields and stable tax revenues.

Can Beijing reverse China’s weakness?

For much of last week, the only major currency stronger than the dollar was China’s renminbi, though it reversed slightly on Friday. Despite currency strength, Chinese stocks were once again among the week’s worst performers. We recently noted a pickup in Chinese economic growth – but the latest activity data suggest the opposite.

We think that is a liquidity problem. For a long time, the authorities have been actively supporting the renminbi’s value, not as an economic tool but as a symbol of international stability. The plan has (arguably) worked but it has also effectively meant less capital in the financial system (buying up renminbi to support its value removes the amount of renminbi around). That exacerbated the damage that higher oil prices did to Chinese growth.

Beijing’s recent communications suggest they might loosen liquidity conditions slightly. If so, we suspect the renminbi may soften – particularly against the dollar, thanks to the Fed’s liquidity tightening. You could argue that China has come through the Middle East crisis politically stronger. As such, Beijing might feel it can afford to let the currency slide. That would reverse one of the key long-term trends in markets – but it would likely benefit Chinese stocks.

This week is the end of a quarter, which usually means fund managers rebalance their investments back to their target asset allocations. That means selling the assets that have done well. Equities beat bonds again this quarter, so many expect markets to take a breather into the second half of the year.

Enjoy the good weather.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.