Market Update: Geopolitics refuses to leave the stage

Just as markets had downgraded the risks emanating from the Middle East, they flared up again. Yet again, however, it is telling how measured the market’s reaction has been to ships being set ablaze in the Strait and the consequent military responses.

Spot oil prices spiked up 12% after Iran’s targeting of ships and President Trump’s very marked expressions at the Ankara NATO summit. Having said the deal was over, US forces hit Iranian targets over two days. Iran responded, targeting both US bases and Gulf country targets with up to 15 missiles and dozens of drones which reportedly were all intercepted before impact. Iran may have talked up the level of response – claiming to have destroyed 85 US military installations – for its domestic audience. This stands against the backdrop of technical discussions between the two sides continuing. As a consequence, oil has settled back down, falling 5% from the $80.50 Brent crude oil peak on Tuesday morning.

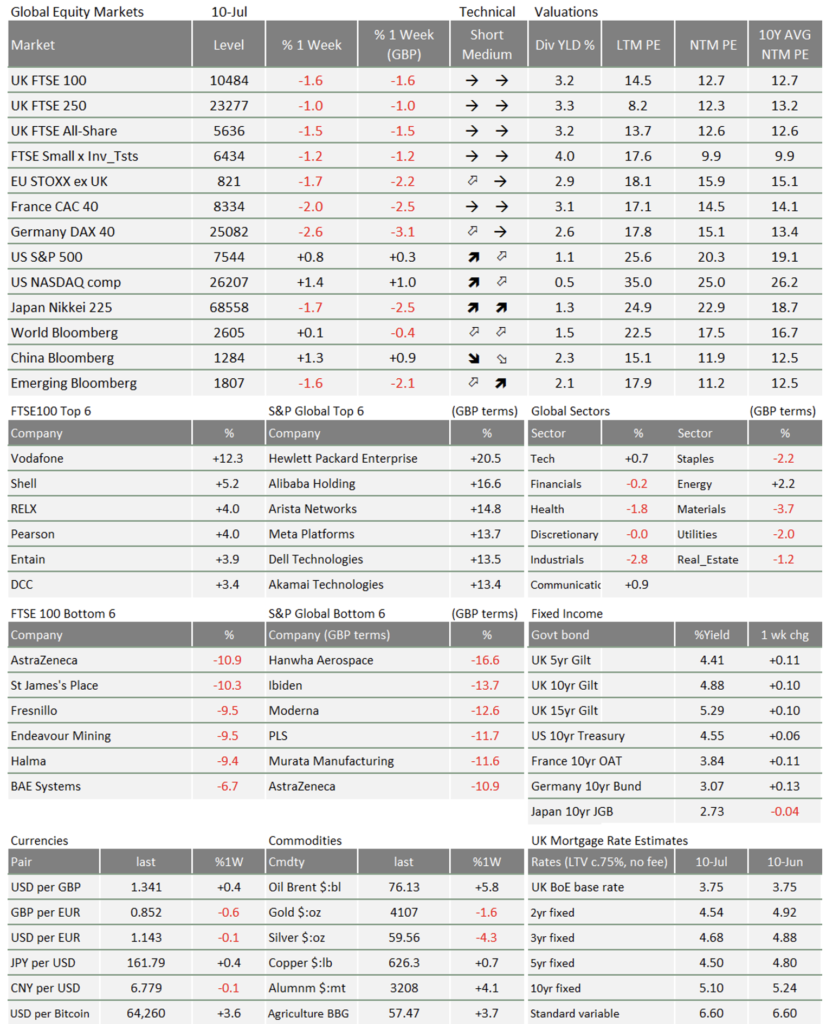

These moves have been mirrored in other assets. Globally, 10-year bond yields rose, with both real yields and inflation expectations up. Of course, both have fallen back a bit after oil’s slight retreat. So too, equities fell only to regain.

And, as we saw in the earlier stages of the conflict, the negative impacts on cyclicals can make the less affected sectors more attractive. The chip sell-off that started last week seemed to have run its near-term course before the news, a stabilisation that helped tech to outperform. South Korea’s SK Hynix share sale (via American Depositary Receipts or ADR, which made it the third largest listing in global history) went well, despite shares not being offered at a discount compared to the domestic share price. Perhaps that’s why its now-diluted Korean share base fell by another 10% last week. The large weighting it gained in the emerging market indices may mean that EM index performance last week was not very representative of the wider universe of emerging market stocks.

Indeed, the markets are becoming more focussed on company stories rather than global geopolitical risk. Initially, this has been around the tech IPO stories such as SpaceX and the share add-ons for Alphabet and now SK Hynix as well as the continued debt issuance to fund the AI buildout. However, merger and acquisition activity is coming up on the rails to challenge for investor focus.

The battle to take easyJet private, with bids from Castlegate and Apollo, is gathering attention from global investors. AI capability-infrastructure and pharmaceutical patent-driven bids dominate the M&A scene; foreign bids for discounted UK companies are a distinct theme. Property company Segro, airline easyJet, financial house Schroders, and utility UK Power Networks have all been picked up, mostly by private equity groups in some form.

Private equity and private credit groups, in terms of their listed equity performance, have had a poor time during 2025 and then again in the first half of 2026. For this year, the story has been one of over-exposure to companies vulnerable to being displaced by AI competition (“SAASpocalypse” as it has been known). While they have been working hard to become beneficiaries rather than victims of AI, the other area of focus seems to be “value” and some UK companies appear to be particularly attractive.

The step-up in M&A may also be signalling an improvement in global private equity access to funds – in other words, liquidity. That would be welcome for investors generally, and would be associated with stable-to-rising valuations amid a broadening of performance across the wider equity market.

However, there was another piece of news involving UK companies and private equity which was interesting if not exactly good news. Hovis had been owned by private equity company Endless LLP and had become loss making again after a turnaround had improved things up until 2023. While a slide in demand for packaged bread and a rise in operating inputs (such as the cost of wheat) have hurt, a major problem has been high interest costs; the weight of debt is too much.

The Competition and Markets Authority approved the merger after realising that Associated British Foods’ Allied Bakeries was also significantly loss making and would have been shut if the merger had not happened. The businesses will be merged and costs will be cut, as scale benefits are being put to use. Hovis has a very good distribution operation, while the combined business dominates the low-cost supermarket own-brand bread supply. To us this reads that cheap bread is likely to be less cheap in the near future.

While inflation won’t be helped by this, the other read-through is that interest costs remain high for consumer-facing businesses. Those costs are driven not just by the interest rate but by the amount of debt. Ultimately, debt holders in these areas may find they have to write down some of their assets.

Meanwhile, a finance minister announced that there would be a new multi-year budgeting framework which would be used to fund measures including investments in economic security, crisis preparedness and other strategic growth areas. At the same time pension funds, including the Government Pension Investment Fund, would be “encouraged” to increase investment in domestic financial assets. Government bond traders assumed that this meant more buying of government bonds so bond prices rose and, consequently, yield fell.

This was Satsuki Katayama, Japan’s Finance Minister. At the end of June, Japanese yields rose after the announcement of a supplementary budget which raised fiscal expenditure. Obviously, the situation is potentially instructive for an incoming Chancellor of the Exchequer here in the UK.

The Secretary of State for Business and Trade Peter Kyle told the Guardian that he was “fed up” with UK investment managers having tweaks to regulation to incentivise buying UK assets, only for nothing to happen.

“I don’t think mandation [forcing funds to invest] is ideal in any circumstances. But I’ll use it if I have to, because I’m in a rush,” he said.

The truth is that it would be incredibly difficult to force UK investment directly. However, it is worth noting that some UK assets are cheap according to (global) private equity investors and that incentives are likely to be put in place.

This week, the US second quarter earnings season kicks off with the major banks giving us a steer on the current state of the US economy. Thus, the focus will continue to shift to corporate news and away from geopolitics. Things may feel more normal, at least for a while.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.