Market Update: A blooming May for the UK

Natalie Elphicke’s defection from the Conservatives to Laboure, Patrick Blower, 8 May 2024

A blooming May for the UK

Global equity markets are rising and the UK is now doing well, the Bank of England is dovish and Sterling is holding up – is political change less worrisome here than elsewhere?

What to take from a strong earnings season

The first quarter has been good for equities and analysts see profitability as positive.

Share trading catches up with technology

Instant share trading is not a reality, but new US rules will halve the time it takes to trade, but the change will cost and time some time to settle.

A blooming May for the UK

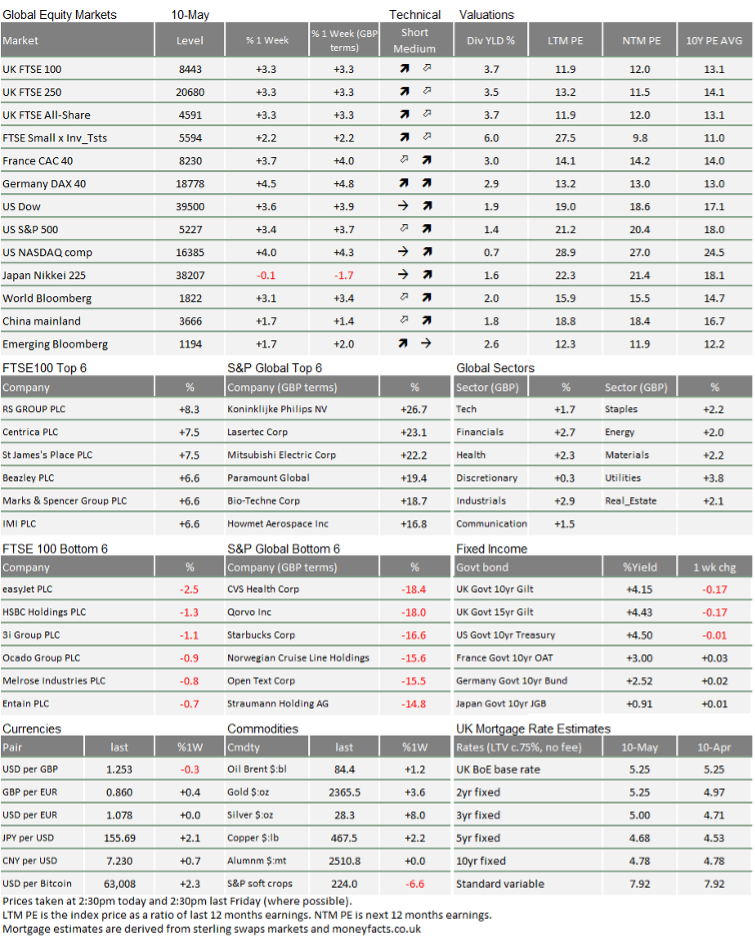

Stocks and bonds had a good week again, revelling in the after-effects of the week before lasts’s US Federal Reserve meeting and signals of a tepid US jobs market in the April employment report. Hong Kong stocks did particularly well, after the Chinese authorities were said to be considering tax waivers on Chinese stocks bought through the island’s Stocks Connect system. Here in the UK, the FTSE 100 stormed above 8,400, helped by the Bank of England’s Andrew Bailey outdoing Jerome Powell, of the US Federal Reserve, in dovishness. So far, at least, there are few takers for the old adage, “sell in May and go away”.

For US stocks, there was mixed news in the final datapoint of the week. The University of Michigan published its consumer sentiment index which fell sharply to 67.4 from 77.2. While this might indicate slower growth expectations, it seems perhaps more to do with rising inflation expectations. Year-ahead inflation expectations rose to 3.5% and longer-term expectations rose to 3.1% from 3%. The initial market reaction was mixed, with bond yields rising slightly and shares unchanged. Starbucks and McDonalds also signalled that US consumers may be feeling less flush in first quarter results.

The UK’s economy experienced some growth in the first part of this year, rebounding somewhat from the contractions of the previous two quarters. January to March showed a stronger-than-expected rise in “real” GDP (real means adjusted for inflation), rising by 0.6% over the quarter. The economy’s bright spots appear to be some surprising strength in manufacturing and services, with construction being a laggard. Even better news is that investment spending has been a positive, even though consumption undershot expectations.

Fortunately, expectations of UK inflation are falling back, according to the Decision Maker’s Panel, an input for the Bank of England’s (BoE) Monetary Policy Committee (MPC). Inflation is now expected to be +2.9% year-on-year in April 2025, versus the Panel’s +3.2% expectation previously. After the Bank of England MPC’s May meeting (concluded on Thursday), Governor Andrew Bailey felt able to indicate that short-term interest rates are likely to be cut. Most now think this will be at the next meeting on Thursday June 20th. Huw Pill, the BoE’s chief economist, pointed to declining pressures in persistent inflationary components in a speech today (Friday 10th).

There is some concern that growth may be accelerating a little too early for a June rate cut. Recent UK Purchasing Manager Indices, an indicator of business confidence, have been strong, and stronger than most other nations. Meanwhile, the weakness of construction could be short-lived if mortgage rates fall back quickly, given the strong underlying housing demand as exhibited in Royal Institute of Chartered Surveyors’ (RICS) residential survey last week. Although near-term house price rises are not showing up, estate agents expect price rises over the rest of this year and in 2025. The RICS “balance” measure will probably mean rises of about 4-5% in the next year, according to Pantheon Macroeconomics. The BoE forecast has GDP being relatively weak in the second quarter (at +0.2% quarter-on-quarter, equivalent to +0.8% annualised) so we could find the external member hawks in the ascendancy in three weeks’ time.

Still, like the Federal Reserve and the European Central Bank, the BoE members appear to be convinced that better real growth is not feeding through into longer-term inflation pressures. More importantly, investors seem happy to believe that they are not mistaken, and have pushed interest rate expectations lower accordingly.

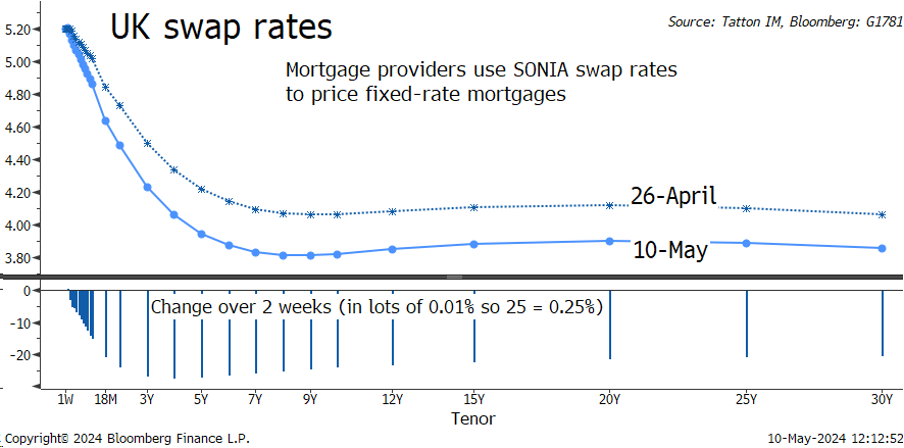

In turn, as the chart below shows, UK yields have fallen quite sharply in the past twoweeks, with the bulk of the shift lower happening last week. Gilt prices have risen, and so too have UK equities.

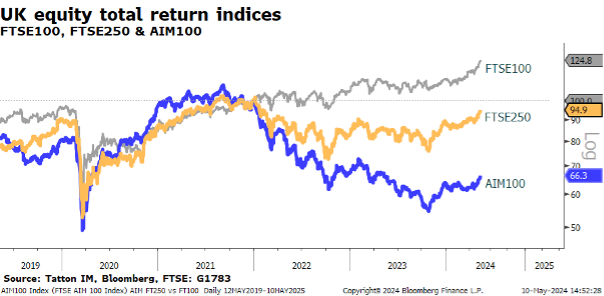

Relative to other country indices, the FTSE 100 underperformed from January into March. Since April it has outperformed and now, year-to-date, is on a par with most other markets in total return Sterling terms. However, this stock market outperformance is probably down to factors outside the real domestic economy. For example, HSBC’s rise has some links to Hong Kong’s rebound, while Anglo American – a global mining company being bought by other global companies – has rallied thanks to takeover talk.

The UK smaller company indices have many globally focused companies as well, but they are predominantly affected by UK (and European) factors. Financial conditions have been much tighter for smaller companies in the UK and beyond for a long time. Companies that generate strong levels of free cash flow have benefitted, but any enterprise that needs capital has been compressed.

The MPC’s easier tone is a welcome boost for UK companies’ prospects and that has been reflected in the performance of both the FTSE250 and the AIM market. While they are yet to outperform the FTSE100, at least they are now performing in line – a good thing when the FTSE100 is doing well.

It is also interesting to note that, while US yields have declined, UK yields have fallen more. Sterling has remained stable against the US Dollar at just above $1.25/£. Likewise, the Yen has weakened slightly against the US dollar, now back above Y155/$, despite Japanese yields rising (rather than falling) last week. It is often assumed that currencies move because of changes in interest-rate differences between countries and, recently, the correlation between yield differentials and currency pairs has been quite strong. Perhaps we are entering a period where this is less so.

Politics may be one reason to think this might be the case. Last week, the Financial Times wrote about the similarity in economic policy between the policies of the current Chancellor of the Exchequer, Jermey Hunt, and the Labour shadow, Rachel Reeves. The FT terms the policy mix as “Heevesian” and we made a similar point after the Spring budget!

While the estimable Paul Johnson of the Institute for Fiscal Studies thinks that their shared goal of reducing the ratio of government debt-to-GDP over the next five years is “daft”, the Office of Budget Responsibility thinks it credible that it will happen. According to Oxford Economics Forecasting, the current level debt-to-GDP is at 100% but will fall to 97% by 2030. Meanwhile, in the US, publicly held government debt will probably rise from 99% now to 109% in 2030, and that assumes that former president Trump’s ‘temporary’ tax allowances will cease.

In the past, investors have generally seen the prospect of a new Labour government as potentially problematic, but this does not seem to be the case this time around. Yet investors seem to have some disquiet about a prospective Republican presidency. It is possible that currencies may be ruled less by yield differentials and more by political differentials in the next few months.

UK stocks are enjoying a bit of time in the sun, after what feels like a long period in the cold. Maybe it has something to do with the improving weather.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.