Market Update: Return of calm bodes well for Spring

Easter lies behind us and the second quarter of the year ahead. Considering how unnerving the first three months of the year were, UK investors in globally-diversified multi-asset portfolios have not fared too badly. Mildly positive returns across the risk spectrum tell the story of another risk storm having passed without sinking global capital markets. If readers feel like they have heard and read it before, then that’s clearly the case. It’s not hard to recall recent risk storms and market corrections, such as last autumn’s government bond market upset, the summer’s growth scare, the market reaction to Russia’s invasion of Ukraine, to name only three of the most fresh ones.

With the latest market recovery having stock and bond markets retesting previous highs, the observed regularity of this wave-like market behaviour already has some market commentators jumping ahead to the old investor adage of ‘sell in May and go away’. While there may be a startling regularity in recent market dynamics, suggesting short-term market timing as a viable investment strategy overlooks that there is a second wave pattern behind markets, namely the global economy and its prospects in the post-pandemic world. That world has been characterised by the back-and-forth of excessive supply and demand mismatches as consumer demand patterns and producer capacity was driven by what was or rather was not possible during the various stages of the pandemic. Paired with overzealous policy support the resulting over- and undershooting of economic parameters, especially inflation, this has created economic and monetary volatility which continues to be harder than usual to predict.

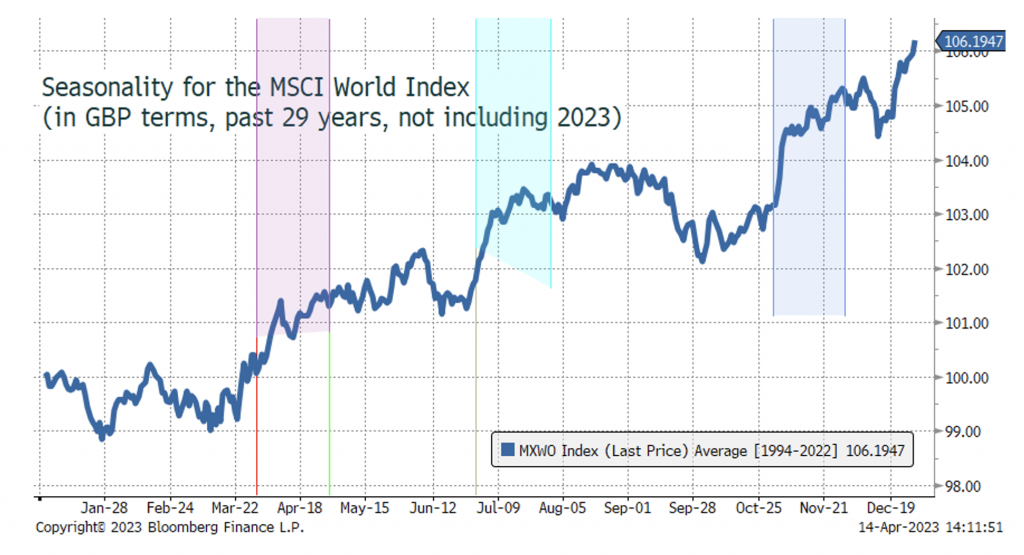

Focusing on the hard facts and figures of current economic activity and direction while markets go through another period of relative calm therefore feels advisable. Likewise, it is worth taking some hints from seasons past, which we start with here. Statisticians that consider the way the world’s equity markets move across the year note that the month of April has the best chance of delivering a positive return and the second-best chance of having the best performance (on average, November has been slightly better). If one includes the last week of March, then historically at least this is the best and least volatile period of the year.

Seasonality is an interesting dynamic and because most of the developed world lies in the temperate northern climes, Spring really does have an influence. Human beings become less stressed as the days lengthen, the temperature rises and the claustrophobia of winter departs.

If markets have calmed down after March’s mini global banking crisis, it seems that the global political environment has also become more serene. If asked, few people would say they feel that risks are demonstrably lower but, while the news flow may have attention-grabbing headlines, the individual news stories are more mundane. Here in the UK, our politicians are working hard to be as boring as possible. China feels it has to react to Taiwan’s President going to the US by conducting exercises off the island, but its response is less provocative than when Nancy Pelosi went to visit last year. France’s President Macron ruffles feathers by talking to President Xi about a ‘relation amicale’. Meanwhile, US President Biden visits Northern and Southern Ireland and delivers an inevitable gaffe while talking about the benefits of peace. Additionally, Russia and Ukraine appear to have reached a stalemate in the terrible conflict.

Meanwhile, anecdotal evidence about the state of the economy are not cataclysmic. The western world’s central banks are still telling us interest rates will remain high because of inflation, but Tesco cut the price of milk. Compared to last year, the western world’s retail prices are 5-7% higher but, in Germany, prices between producers and wholesalers are now only about 2% higher than last year. In Asia, prices are not rising discernibly. Indeed, China’s producer prices are 2.5% below last year’s level.

Through 2021, the massive liquidity injections to stave off the pandemic had the effect of calming economies and markets. Since the start of 2022, the inflation after-effect waves this entailed brought the aforementioned scare storms upon the world’s economies and therefore also upon its bond and equity markets. But even here, the sheer scale of the movement waves in prices is now less worrisome.

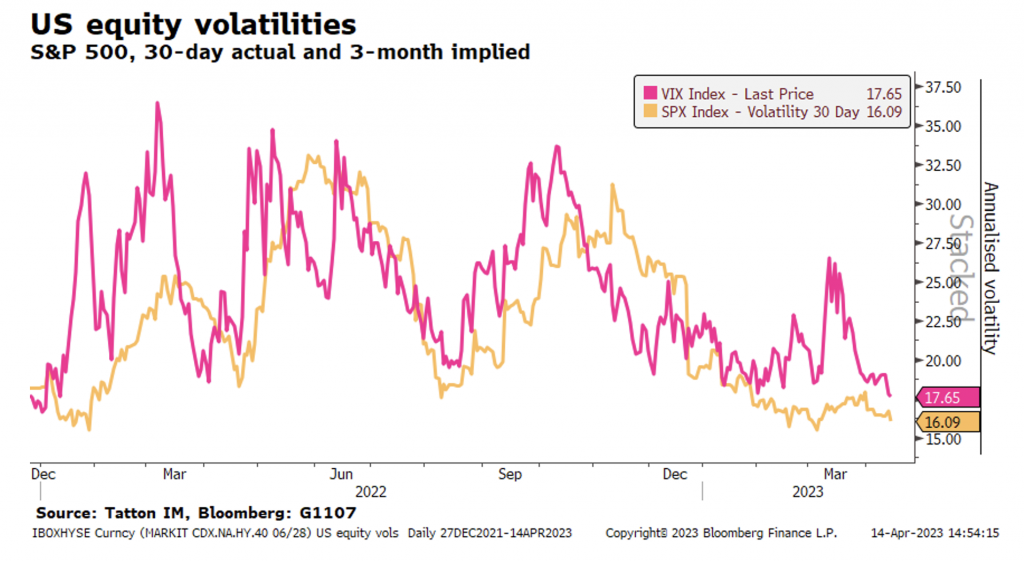

The chart above shows in yellow the actual one-month volatility of the S&P 500. The pink line shows the market’s expected volatility for the index, which is the volatility used to price options. Both are now at their 12-month lows.

Historically, we are not suggesting that the volatilities shown here are low in comparison to the lows of the 2010s. In 2017 for example, the S&P actual one-month volatility remained below 10% for the whole year and got down to below 4% in that October. However, the process of moving from a higher volatility regime to a lower one tends to be associated with positive returns. Just mechanically, investors become less worried about putting cash to work in the markets. Equally, more sophisticated investors that use option hedging spend less of their returns on expensive options which, in turn, boosts returns.

Of course, as mentioned earlier, April is often not very volatile so predicting things will not be turbulent into the summer may be foolish. We point out in the articles below that the world’s regions appear to be on a gentle economic upswing and that China’s upswing is more than gentle, which is obviously a good thing. However, US weekly employment data has been weakening noticeably and, by our measure, is close to becoming a signal of recession. Meanwhile, UK employment has also weakened.

Across the Western world, small companies continue to be stressed by high short-term lending costs, if they can get loans. Some have no longer access to loans at all. In the US, the profitless tech companies are still finding access to equity cash difficult to come by.

This suggests that until central banks are comfortable headline inflation no longer poses a threat, destabilising bankruptcies remain a strong possibility. This week, we have had mixed messages from US Federal Reserve (Fed) members, European Central Bankers and Bank of England Monetary Policy Committee (MPC) members. The mix has been either warnings about rate rises or statements about “wait-and-see”. We are still yet to hear anyone proposing that cuts should be made. The all-too-predictable danger is that rate cuts are only discussed after economies have started falling. But to give central bankers their due, they have yet to induce recession despite the talk for the past year. Perhaps they can engineer a soft landing for the economy after all, by way of a return to lower, less damaging interest rates while inducing a less risk-averse attitude from banks and other sources of corporate credit towards borrowers.

In this regard it is notable that larger banks are doing well, if this week’s results from the likes of JP Morgan and Citi are anything to go by. While they tell us they are wary of lending, non-performing loans remain lowish rather than high (they have gone up but are actually not in recessionary territory). Meanwhile, depositors scarred from their recent small bank experience are content to receive less interest than the (large) banks make in the money markets in return. With credit spreads for lending even higher, the banks have capacity and a strong incentive to lend, despite the negative yield curve suggesting otherwise. It may well be that despite the demise of Silicon Valley Bank and others, the larger banks will ease credit standards ahead of the smaller ones, in order to cement market share gains. Thus, smaller companies may get a bit of help in coming months, even if the lop-sidedness of the banking sector is bound to result in less competitive credit markets over the longer term. The next loan officer survey will make interesting reading.

The renewed calm in markets is a positive for the prospects of a soft landing, while the stability and profitability shown by larger banks suggests that the narrow path towards a stable non-recessionary slowing is still being followed. As we have said before, the outlook feels delicately balanced at the moment and we therefore cannot say with conviction that there will not be slips. But we have lower volatility, and progress to towards smaller ‘waves’ in markets and the economy. At the same time, the inflation genie is slowly being squeezed back into the proverbial bottle. This all bodes well – for now.

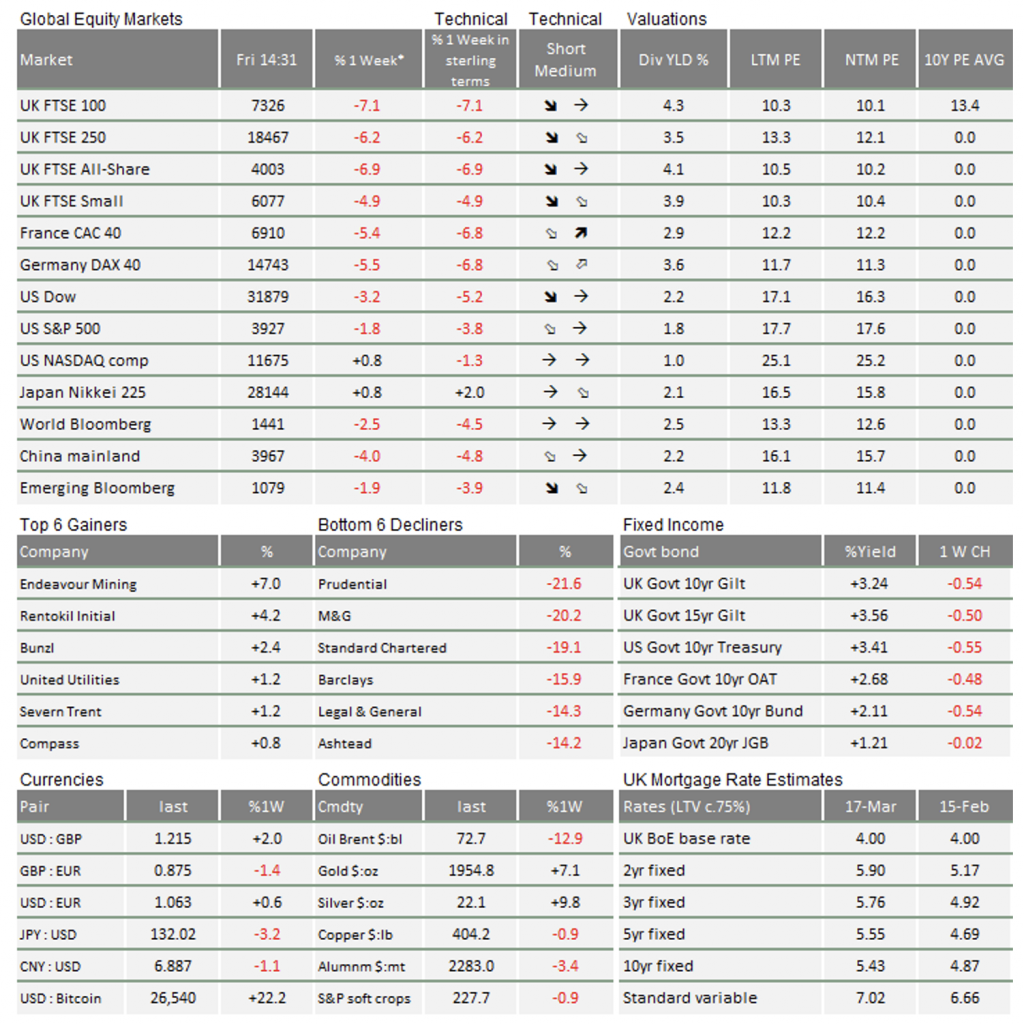

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.