Market Update: Recession fears creeping back

Source: Ben Jennings, 2 October 2023

Recession fears creeping back

Yields hitting a 15-year highs, despite signs of economic slowing, seems to have wrong footed bond traders, but it is likely to accelerate the slow down.

September 2023 asset returns review

A choppy month for investors brings a lacklustre, yet volatile, quarter to an end, despite overall positive returns for the year.

Brazil – more than meets the eye

The B in the ‘BRICS’ economies has a chance for the political stability it needs to secure long term foreign investment.

Recession fears creeping back

The balmy autumn temperatures have continued into October, but the market chill that has also carried through from September is more troubling.

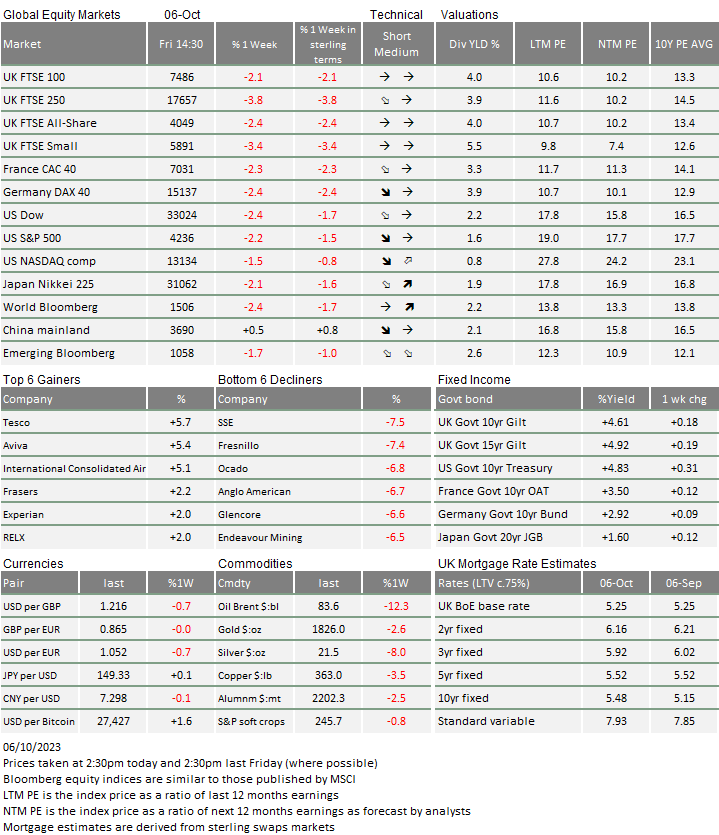

Financial markets are in one of those occasional periods where the world’s economic realities do not quite seem to match what some asset price moves seem to want to tell us. Last week, and continuing the trend from the previous week, we saw a further rise in global long bond yields despite some weakness signals from the global economy. The 10-year US Treasury benchmark hit a yield of 4.88% in early trading on Tuesday – the highest point in 15 years. Other government bond markets duly responded, although rose slightly less. Because of the inverse correlation between yields and bond valuations, this means that fixed-interest government bond prices fell. Subsequently, yields fell back from the highest levels but are now heading back towards their highs after another extremely strong US jobs report. Across the board, they are 0.15%-0.30% higher than last Friday which equates to a fall in in the global bond index price of about 1.5%.

At the time of writing, global equity markets have broadly slipped by about 2.5% in GBP-sterling terms, mostly (we calculate) due to the valuation impact of rising bond yields rather than pessimism over economic growth and any impact on earnings.

However, commodities have also come under pressure which does seem to be related to traders’ fears that growth will be lower than previously anticipated. In particular, oil prices have reversed all of the rise seen in September. Brent spot crude fell 13.5% in just three trading days and is back to $85 per barrel, the same as on 29 August. Industrial metals, which actually fell in September, continued to decline about 4%. Commodity investors seem to be more downbeat about global growth than others.

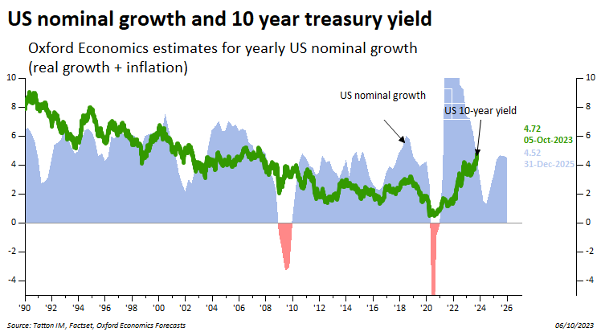

Regular readers may at this point think, hang on …. hasn’t Tatton written in the past that bonds are supposed to be the best barometer of economic health? Don’t yields rise when economies are doing well and fall when the economies are having a tough time? And they would be right. For much of the time, bond yields reflect the broad level of economic activity, both real growth and inflation (we refer to this aggregate as nominal growth). Below, we show a chart of the US 10-year Treasury yield (in green) and US nominal growth since 1990 with data and estimates from Oxford Economics:

Like most forecasters (and ourselves), Oxford Economics foresaw a US slowdown coming during 2023 and has been surprised (as we have) by its resilience. Indeed, there is no denying that the forecasts for a slowdown this year have proved wrong – in the US and even here in the UK. Global intermediate and finished goods trade has clearly slowed but demand for services has been solid. Economies that are more services-heavy have done better than expected (such as the US, UK and to some extent, Japan), those that are goods-based have done poorly (China, Germany, etc.). Services employ more people so the jobs market remains supportive, people remain reasonably confident and prepared to spend.

Nevertheless, a slowdown is still likely as the pace of fiscal stimulus wanes through next year. And the rise in yields makes a slowdown more likely, not less. For many people and for large businesses, their cost of new borrowing is more related to long-term rates than short (for example, US mortgages are 30-year fixed), so the squeeze is getting worse.

So why have bond yields gone up? We think that some (perhaps quite large) investors became overconfident about an ‘imminent’ slowdown earlier this year based on the economic sentiment indicators like the Purchasing Manager Indices (PMIs)a. Rarely do these indicators give false signals but this appears to be one of those times.

Some investors locked in what appeared to be attractive yields. For them, the latest yield increases constitute a missed opportunity but not much else. For investors that borrowed money to bet on falling yields on longer maturity bonds (as hedge funds can do), the price movements have been very painful and for an extended time. These are the most likely to capitulate now. The unwinding of their positions creates a price dynamic which says little about changed market expectations and much about past errors of judgment.

Other investors bought longer maturity bonds and sold equities, expecting a slowing economy leading to general falls in earnings expectations that would hurt stock markets. As it happened, the valuation impact from rising bond yields has hurt stock prices but not the earnings expectations side, as in general, equity analysts have held their 2024 forecasts for larger cap stocks steady. So the damage has been limited so far, generating only a lacklustre quarter for asset returns on the back of just the yield-driven valuations component. The Q3 earnings announcement season begins slowly this week, but will build to a crescendo as we head into November, just as all the central banks make their next rate decisions. Earnings are likely to bear little in terms of negative surprises, but business leaders’ forward guidance may force down analysts’ 2024 earnings expectations.

Market volatility has shifted up across all asset classes which suggests global market liquidity is getting tighter – not surprising, given the continued drain by central banks and the substantial losses across bond markets and, to some extent, commodity markets. Tighter financial conditions make it more likely that growth will slow so we suspect that, in themselves and just like with oil, higher bond yields now probably mean lower bond yields later.

For equity and credit markets, it may be that bond yields plateau and then fall without too much impact. However, the tightening of liquidity is not a helpful signal and the risks of a sharper bout of volatility are clear. Bond yields will probably come down more so if risk assets are under pressure but that may this time be because economic weakness undermines earnings projections and equities would then find it difficult to rally substantially just on declining yields.

Ahead of the next round of rate meetings, central bankers could make things worse if their comments were seen as hawkish. However, inflation data are likely to be helpful rather than a hindrance so we should perhaps expect them to sound slightly dovish in the next few days and weeks. We certainly hope so.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.