Market Update: Changing Tides

Last time we reminded portfolio investors of the importance of making sure that long-term investment decision-making is not overly influenced by short-term market fluctuations. At Vizion Wealth, we aim to ensure portfolios remain positioned appropriately, and are fine-tuned when medium-term changes in the economic and market outlook either necessitate adjustments or indeed present new opportunities. The strong rebound in stock markets around the world over the week has been a case in point.

Last time we reminded portfolio investors of the importance of making sure that long-term investment decision-making is not overly influenced by short-term market fluctuations. At Vizion Wealth, we aim to ensure portfolios remain positioned appropriately, and are fine-tuned when medium-term changes in the economic and market outlook either necessitate adjustments or indeed present new opportunities. The strong rebound in stock markets around the world over the week has been a case in point.

With oil prices having rapidly fallen from over $130 per barrel (pb) back to around $100pb, it seems clear that the prospect and negative potential of an energy price shock discussed last week has dissipated, returning more optimistic sentiment to markets. While this is broadly true, there were other dynamics at play over the week worth mentioning.

First, it was not just the price of oil that declined steeply, but also heating gas and many of the other hard commodities that had previously driven the fear of a price shock derailing the recovery. So, was it simply the faltering of Russia’s invasion of Ukraine and the rising probabilities of a near term peace settlement that reversed commodity prices? Well, it certainly was a major influence, but market observers suspect another reason for the strength of the reversal was that the sheer magnitude of recent volatility left so many of the more speculative commodity market participants seriously out of pocket (margin), and that appetite and liquidity available for further ‘bets’ just simply dried up. We also know that the direction of commodity market price movements has over the past decade increasingly been boosted and exacerbated by momentum-detecting trading algorithms. This means, once the ‘price-tide’ turns, the boosting dynamics go the other way, leading to the extremes of 2020’s negative oil prices as well as this year’s sky-high levels.

The question last week was therefore whether the inflation scare has now peaked and are more realistic expectations finding their way into capital market valuations? It certainly seemed so, after the lowering of market-implied inflation expectations decreased the historically extreme gap between equity and bond market real yields. However, there was also fear that the US or UK central banks could upset these decreasing market tensions with this week’s interest rate announcements.

In the end, rate-setting committees on both sides of the Atlantic raised interest rates by just 0.25% as had been expected, while the US announcement hinted at an expectation of a strong economy which was taken positively by markets. However, reading between the lines, monetary policy tightening could still come to bite in 2022. This is because the longer the price shock of the past nine months carries on, the more this risks leading to an embedding of inflationary expectations, turning the transitory price shock into structural inflation. Therefore, while central banks are tightening monetary policy gently enough to not cause serious upset, they have also signalled that they are prepared to step up their actions should labour markets become too buoyant – even when price rise pressures dissipate later in the year, as currently widely expected.

They may not need to worry too much. We can already detect a certain labour market slackening in the US, and perhaps in the UK, as last week’s mass sackings callously announced by P&O Ferries demonstrated. Price rises are also increasingly driven just by car fuel and gas prices and, from past experience, we know consumers have shown a tendency to look through those.

The wider price pressures from supply chain stresses have also recently reduced, but this is where the positive news flow of the past week ends, after China reacted to fast rising cases of the Omicron variant with widespread lockdowns. We dedicate a separate article this week to China’s ever- changing economic and market outlook, but note here that over the shorter term, China’s leadership appears keen to strongly support its domestic economy through this rough patch, especially so as President Xi will be seeking approval of a third term in office later in the year.

Beyond these observations about the drivers of this week’s market actions, the most important aspect for the medium to long-term picture may not be Russia’s war on Ukraine, but how the relationship between the US and China continues to develop against this backdrop. Presidents Biden and Xi held a two-hour call on Friday, ostensibly to discuss Russia’s aggression, but beneath the surface both sides will be considering Taiwan, and how recent developments may have influenced China’s own ambitions to increase their territorial reach.

We hope quiet and measured diplomacy will win the day, although Biden’s camp is making somewhat provocative statements as we write, which suggests the US may be taking a hard-line stance amid a sense of uncertainty about China’s position.

Behind all this is a very uneasy conclusion. If peace in Ukraine is to be achieved soon, it may only happen with some form of international acknowledgement that allows Russia to gain control of Donetsk, Luhansk and ultimately Crimea. China’s claim on Taiwan is stronger than any that Russia has over these areas. Peace in Ukraine would therefore make Taiwan very nervous.

To end our top-level comments, we clearly welcome this week’s market dynamics, but also acknowledge that market valuations for the forthcoming months will continue to be subject to many moving parts, with an almost equal probability for improvement or deterioration. Much will depend on continued easing of supply bottlenecks and consumers increasing their demand for services rather than goods as we leave another winter of COVID-restricted lives behind. For the positive post-pandemic economic impulses from this to feed through to risk asset returns, labour markets need to remain balanced enough to not force central banks to step up their still very measured monetary tightening in an attempt to put the inflation genie back into its proverbial bottle. We are monitoring this fragile balance intently, while being ready to react with portfolio adjustments should they prove required or opportune.

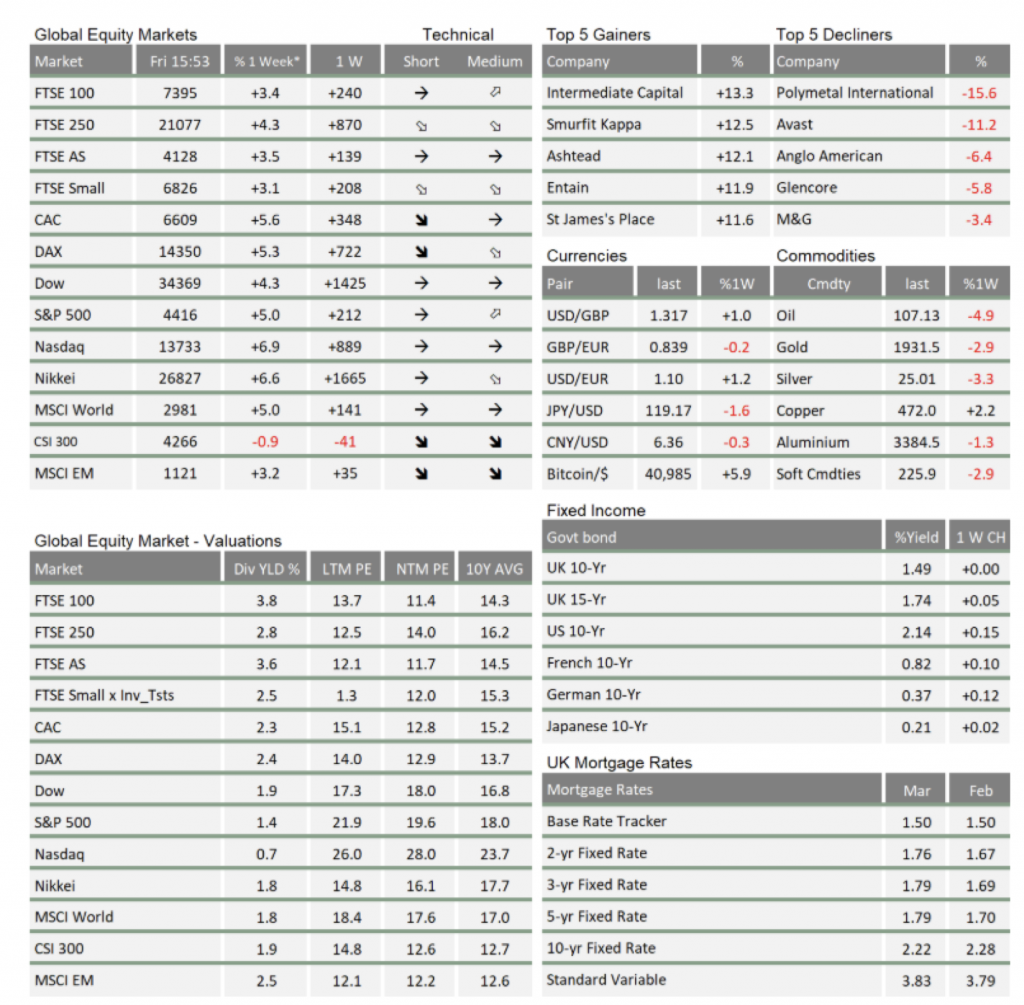

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.