Market Update: Market & Investment Activity Update

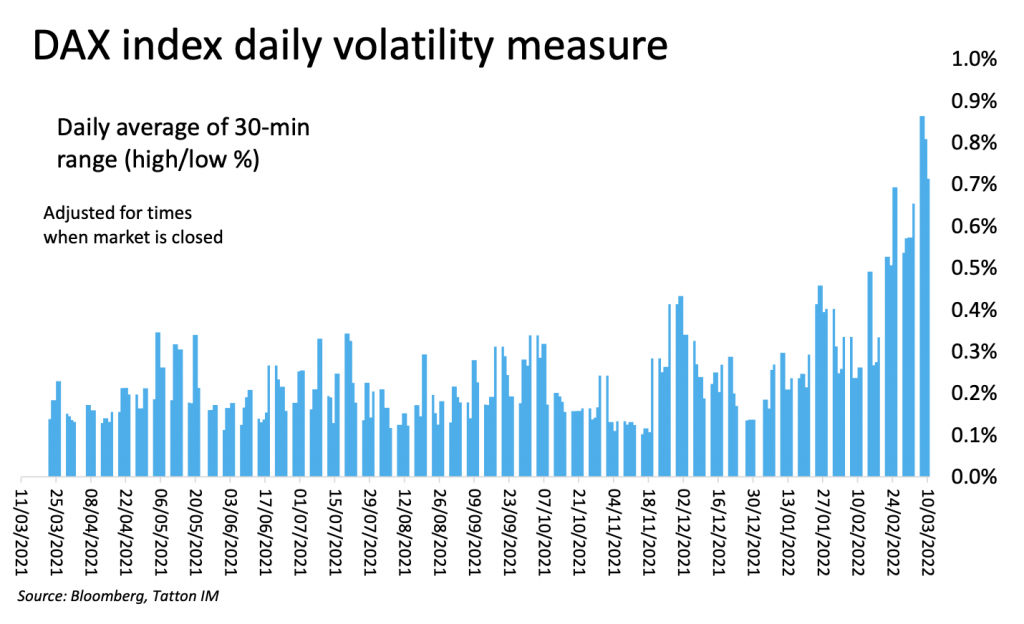

For the last few weeks, we have regularly had to caveat our commentary with the phrase “as we write”. The chart below shows how much the German DAX benchmark equity index (which tracks the top 40 German companies) has on average moved every 30 minutes over the past year:

Markets go up and down, but in the past week the DAX has moved up and down every 30 minutes on average about 0.75%. Last week, for example, President Putin has said that the Ukraine-Russia talks taking place in Turkey have “positive movement”. Within five minutes, the DAX rose 3%.

On Monday morning, the German and French equity indices had underperformed the US market by 10% on a year-to-date basis. By Thursday afternoon, the markets were back to near-equal performance. For any long-term investor, changing portfolios in this environment is a difficult and potentially costly process.

Events which are negative for markets may not always mean that markets end up being negative. That is because those events cause reactions. During the first months of the pandemic, central banks eased policy, cutting interest rates and flooding the financial system with liquidity, while governments borrowed huge sums in order to provide emergency income to households and businesses. The speed of the reaction in the early months of 2020 was remarkable; the US recession was the shortest on record at just two months.

Although the Great Financial Crisis of 2008/2009 was ended by similar policy reactions, they were slower in coming. The recession took 18 months and was the longest of the post-war period. The US Federal Reserve (Fed) initially saw the crisis as a specific issue in the financial sector, and that there was not enough ‘moral hazard’ for individual firms found to have behaved badly. It was unwilling to use the ‘Fed Put’, the idea that Fed policy would protect risk takers by supporting risk asset prices.

The Federal Open Markets Committee meets this week, and will almost certainly raise rates by at least 0.25%. Its bond buying quantitative easing operations ceased this week. Although the war in Ukraine have ensured markets expect a more cautious approach at this meeting, US inflation as measured by the consumer prices index (CPI) has been rising at an unchecked 6% annualised rate for the past three months.

For the Fed and all other developed world central banks, the conundrum is this: is real demand going to be so adversely affected by the upswing in non-labour (energy) costs that they should wait for the cost shock to play out on dampening further general price rise, or should they fear that the non-labour costs will feed back into wage demands amid a tight jobs market?

The Fed will want to be perceived as fighting inflation, if this week’s European Central Bank (ECB) council meeting is any guide. Given the much greater proximity and impact of the war, most economists expected a rather dovish outcome, but the ECB turned more hawkish. Its bond purchases are now set to finish before October and a rate rise could happen at the same time.

Judging by ECB President Christine Lagarde’s demeanour in the press conference, the meeting might well have been rather fractious. She tried to “sell” the idea that the ECB retains more flexibility and is more data-dependent now. However, the bond markets didn’t think that was the outcome. 2-year bond yields rose 0.125% during the announcement.

So, there is some risk that the aftermath of commodity and energy price rises drives a medium- term fall in buying power (demand) for businesses and consumers, which reduces inflation from becoming structural but might be ignored for some time by the central banks. In a sense, we think of it as ‘policy exhaustion risk’, or the risk of an outright central bank policy error.

In the US, and possibly also in the UK, fiscal policy latitude also seems to be limited. However, there is much hope for Europe that the fiscal policies are not exhausted but positively enlivened by the current events. France’s President Macron (now extremely likely to win a second presidency) advocated another round of mutual bond issuance to cover more European defence and green investment. It was not immediately welcomed by all, so it will take more effort, but it seems likely Europe’s fiscal policies will remain accommodative for some time.

This leads to a scenario of a slowing economy for the short-term but with Europe at the least rebounding strongly in the medium-term. Much of the short term depends on what happens in Ukraine and in the commodity and energy markets. Thereafter, it may be about government largesse. Unfortunately, central banks seem – at least for now – to be less responsive than usual, or have more conviction that this war – and the sanctions that come with it – will end much sooner than almost anyone else.

Meanwhile… COVID. Is it still a problem? The US is set to end its mask mandate (for public transport and other public areas) this month. Here in the UK, case numbers are rising again although case severity is still muted and has been reported to be below seasonal flu (even if infection numbers are significantly higher still).

At the same time, China mainland’s cases have topped 1,000 per day. According to Bloomberg, the current epicentre of the outbreak is in north China’s Jilin Province. Its state capital Changchun (about the same population as London) has locked down. Of more importance for global trade is Shanghai. This week it had (only) two ‘community’ cases – those not explainable by contact with carriers from elsewhere. Shanghai has yet to make any restrictive move.

Currently, the disease’s severity is much reduced compared to the initial outbreak in Wuhan. Of the current cases, 70% show no symptoms, possibly because China embarked on a more widespread and effective vaccination programme. There were rumours that the central authority’s zero tolerance policy approach was softening.

Bloomberg also reported that PremierLi Keqiang, the second-ranking leader of China’s Communist Party, has called on the world to work more closely to create the conditions for a return to post-pandemic ‘normal’ living conditions. With today’s press conference marking the end of the annual National People’s Congress in Beijing, Li said officials will work to make China’s response more scientific and targeted, to maintain the normal functioning of everyday life and supply chains.

That’s a positive sentiment, but if Shanghai comes under pressure before it is ready, this will be a real test. As a result, it is still too soon to assess whether China will continue on its reopening course or prescribe another painful lockdown period to its economy.

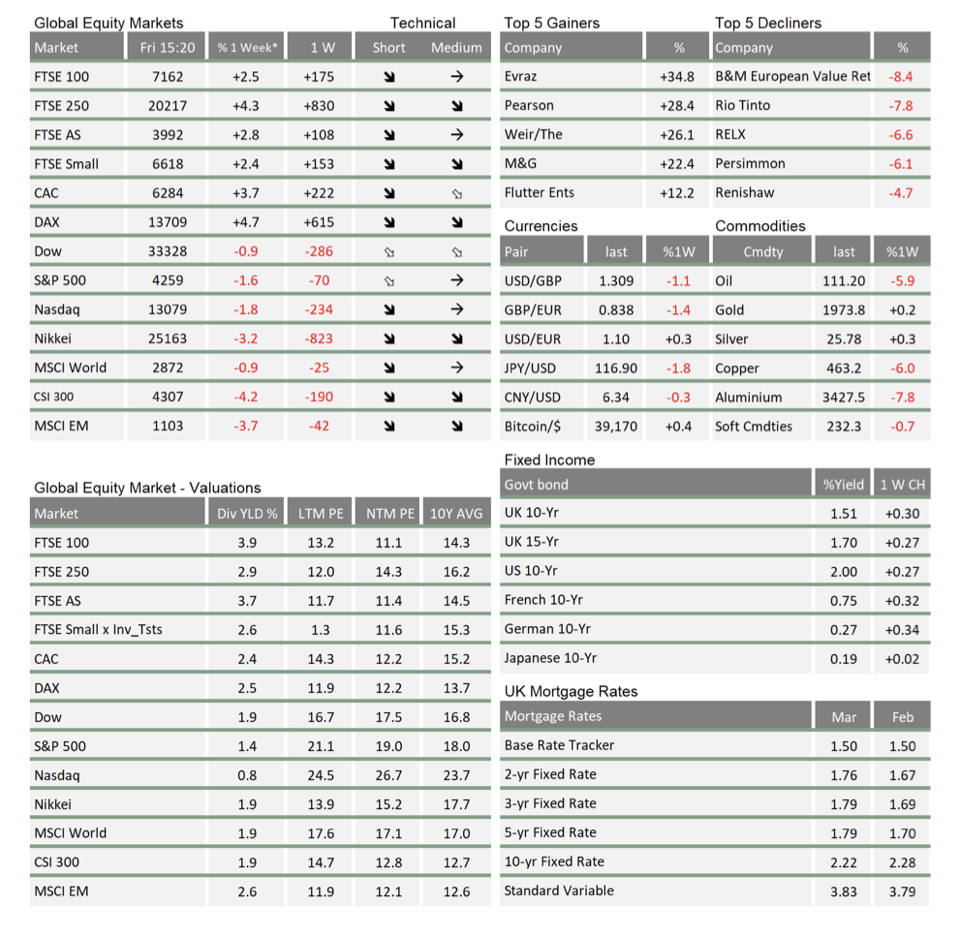

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.