Market Update: Central bank Elves boost 2023 Santa rally

Everyone likes a Santa Rally, Hedgeye, 15 December 2023

Central bank Elves boost 2023 Santa rally

The scrooges of last year’s Christmas, US central bankers, put markets in a warm festive mood this week by surprisingly declaring ‘peak rates’ – is the US getting ahead of Europe and the UK once again?

Tatton’s 2024 Outlook

After an unexpectedly overall positive 2023 for investors, we take stock of what 2024 may hold, now that the inflation genie appears to be back in its proverbial bottle.

Central bank Elves boost 2023 Santa rally

Looking back to a year ago, the introduction article to our 2023 outlook was titled: ‘Central bank scrooges cancel Santa rally’. One year can be a long time, and this year provided a very welcome Santa rally to end it. This means that globally invested, diversified investment portfolios like the ones we manage for clients, should have once again, by and large, outperformed prevailing cash rates and consumer price inflation. Higher risk, equity focused portfolios in some instances should have returned even twice that.

The gifts Santa brought markets were crafted by the central bank elves. Well, maybe Andrew Bailey and Christine Lagarde were less involved than Jerome Powell but at least they didn’t try to break bits off the gifts. On Wednesday, the US Federal Reserve (Fed) did not move rates, but the market reacted almost as if it had announced a cut. Expectations of where rates will be across next year dropped sharply, with the first 0.25% rate cut now seen as underway by May and then rates being cut by 0.25% five or six times in total in 2024. Last Friday, the first cut was predicted for June and three/four cuts for the year.

The shift in tone of Jerome Powell’s press conference comments after each of the last three Federal Open Market Committee (FOMC) rate decision meetings has been the spur for changing market perceptions, given there have been no actual interest rate changes. We note that his authority with markets has increased, with investors lately hanging on his words almost as much as they did with the legendary Alan Greenspan in the 1990s.

Powell spoke of declining inflation pressures and, notably, an employment market moving into balance, which was completely unexpected. Given the unemployment rate had shown a fall from October’s 3.9% to 3.7% in November, this was an important assertion. Only at the beginning of the year, Powell had talked of the non-inflationary level of unemployment rate being 4.5%, so clearly, the FOMC’s view of what level constitutes ‘balance’ must have changed.

It is also interesting to note how the trading interlinkages of money markets mean that (for the time being) the European Central Bank (ECB) and the Bank of England (BoE) currently have less impact on domestic interest rate expectations than does the Fed. Both held meetings on Thursday and, despite no rate move and only marginal differences to the October/November meeting narratives, rate expectations dropped before the meetings and stayed there as well.

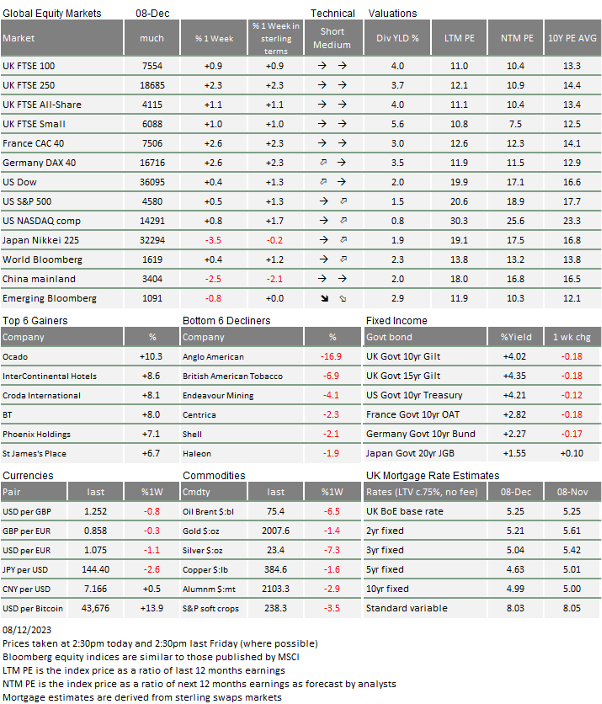

Andrew Bailey did allude to “making progress” on the inflation front. Not surprising, since growth is anaemic for the UK as a whole, and November’s monthly growth was -0.3% which may well mean this year’s last quarter will show a small contraction. However, we continue to see a disparity between sectors; services remain supported, but manufacturing is worsening again, according to the CIPS/S&P Global purchasing manager index (PMI) reports. These showed the services PMI rising sharply to 52.7, a level which indicates services are back to a reasonable growth path; but it was not so good for the manufacturing PMI, back down to a nasty 46.4 and therefore definite contraction.

This dynamic was also the case in Europe until recently, but things seem to have changed and for the worse. The hope was for weak manufacturing to bounce but, unfortunately, service PMIs have shifted downwards to join manufacturing in the doldrums. Perhaps it is little wonder that despite the newly dovish mood music from the Fed, investors continue to see the ECB as the major central bank most likely to cut rates first, with the BoE not far behind.

Beyond the positivity from the service sector, we should also note that the UK is going through a bit of bounce in the housing market, now that 5-year fixed rate mortgages on offer have dropped back to around 4.5%. The housebuilders are up since the start of this last quarter by over 17%, currently beating every other sub-sector. And this is not confined to the UK, it’s interesting to see how house prices are also bouncing in other global regions.

Next year will probably be full of political drama. Hopefully, it will be the agreeable kind, borne out of a smooth democratic process. Major elections will happen here, in the US and many other major nations. Returning to the theme of central banks, it will not just be politicians having their records and behaviours judged. Having endured the almightiest inflation episode, central bankers may have decided to tread more carefully over this coming year, so as not to inflame sensitivities during a period of heightened political debate. This is not to say that they will develop biases, nor that central bankers will be self-serving. Rather, we should expect that their messaging will be less confrontational. Perhaps, if there is to be an impact on policy, it will be that they will prefer to act a little more quickly if inflation (especially wage inflation) allows.

On the back of the Fed’s sentiment change announcement, equity markets have in general had another good week. The exception was once again China. The western world’s elections are part of a system which spreads power and responsibility across many people and institutions, and thereafter holds them accountable for their actions in a transparent way. China has no such system and appears to be going through a crisis of confidence wherein its autocracy is a large part of it. Just over a week ago, Politico reported that Xi Jinping appeared to be purging his erstwhile lieutenants in a Stalin-like manner, confirming rumours we had picked up on the City grapevine. We cannot know the truth, but should hope that China is able to break this current spiral soon, so that confidence and economic sentiment can return to what is after all the second largest single economy.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.