Market Update: Back pedalling central bankers

Contrasts of our times, Source: MATT, 7 November 2023

Back pedalling central bankers

The turn around rally petered out last week, but the sentiment shift persists because the tail risk of a policy error has diminished.

Bank of England giving and receiving mixed messages

The confusion over keeping interest rates higher for longer is more likely caused by confusing data than disagreeing central bankers.

Europe’s natural gas on a bumpy road down

Gas and electricity prices in Europe remain far higher than the US, but a repeat of last year’s stresses on businesses and consumers is much less likely.

Back pedalling central bankers

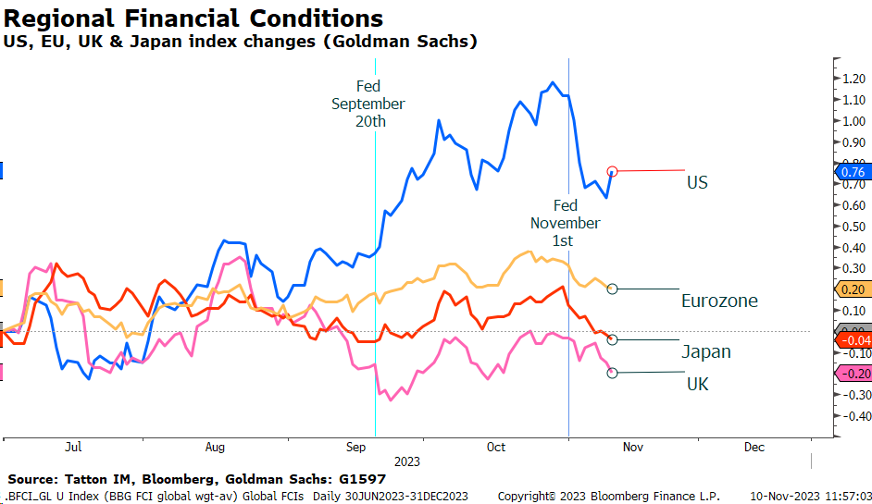

The turnaround rally in stock and bond markets – started by the previous week’s dovish central bank comments – petered out towards the end of last week, with central bankers seemingly at pains to reverse their messaging or at least reaffirm their continued commitment to keeping interest rates high however long it takes to get inflation back to their 2% target. Perhaps this was not entirely surprising, given the eight-day streak of US stock market gains and easing bond yields undid much of the financial condition tightening that US Federal Reserve (Fed) Chair Jerome Powell referred to in the previous week as doing the central bankers’ job (see chart below – the higher the reading the tighter the financial conditions). But then – not really – or at least the fundamental shift in market sentiment has occurred and is unlikely to flip again so soon.

Indeed, while most of the leading central bank policymakers have sought to say rates will remain restrictive, investors now think the tail risks of higher rates have diminished. Underlying this is the sense that the greatest inflation risk is coming under control, as labour markets appear to be softening.

As has been the case on more than a few occasions in recent years, the UK is doing a good job of exemplifying the global economy’s issues.

As a matter of fact, sometimes the UK appears to be a caricature of what happens in the rest of the developed world. The pandemic seemed worse, inflation more embedded, growth seemed weaker and employment has been tighter. Our politicians swing repeatedly between populism, political ideology and pragmatism. The economic data has been more suspect and the economists have been especially wrong. Now our central bankers are sending more mixed messages than their counterparts.

The current situation may well be because the economy has passed through a turning point. The UK economy has moved into a less inflationary environment. Unfortunately, that goes hand-in-hand with a quickening growth slowdown. We are picking up from our grapevine that small company stress levels appear to have increased, as have job lay-offs.

So, we seem to have passed through the peak in nominal growth (real growth + inflation) and are now heading back down to more normal levels. In most cycles we would expect to see real growth become negative for a time while inflation starts to undershoot central bank targets. That normally means contraction of economic activity (aka a recession).

What matters for capital markets is the depth and pace of the downswing. Will there be a collapse of both ‘bad’ and ‘good’ borrowers? In this phase, the danger is that contagion problems spread much faster. The increased uncertainty heightens the likelihood that banks, investors and other intermediaries in the financial system respond to rising risks and uncertainty by pulling their liquidity prematurely. This in itself creates the downswing in both markets and economies (of course, if it happens, no bank or investor would say they were premature).

Central banks actively seek this moment but, for them and us, this is also the point of greatest danger. Information is more than usually uncertain while the past problems of inflation remain at the forefront of worries. Indeed, because we start from such elevated inflation levels, there is a lot of uncertainty about where we are in this trajectory.

We ask our central banks to constrain inflation and to enable our financial systems to function as optimally as possible. Which of these requirements is most important depends on the situation, but the flip from the first to the second can happen in what feels like the blink of an eye.

Bank of Japan Governor Kazuo Ueda said last week that he has an “asymmetric” problem. He can easily raise rates but cutting them is difficult because in Japan short rates are still around 0%. This is true – as long as growth is on a positive path, the question about raising rates is less catastrophic although, as we know from our experience, perceptions that you have time can lead to complacency.

But we also know the most common central banking mistake is one of delaying rate cuts. Central bankers may be expert enough to see different signals, but they are individuals that are in the public eye and they feel the weight of their responsibilities – currently this is to ease the cost-of-living-crisis pressures inflation has brought upon the public. This can make them cautious, reliant on data that is “authoritative” but is actually too slow-moving to catch the sharp swing from an inflation regime to a recession regime.

Thus the recent days have been one of hope for investors. Whether it’s the Fed, the European Central Bank (ECB) or the Bank of England (BoE), the discussions are acknowledging that rate rises are almost certainly over for now and that cuts are on the cards.

Despite BoE Governor Andrew Bailey saying repeatedly that “it’s too early to talk about rate cuts”, his Chief Economist, Huw Pill, spoke openly to the Chartered Accountant conference about the possibility of rate cuts next year. He must have thought the Governor was asking for conversation to be kept breezy before breakfast. Meanwhile, Jerome Powell undid a bit of his post-meeting dovishness but markets have sensed a welcome responsiveness.

Financial conditions had tightened after the early autumn meetings, somewhat in Europe, UK and Japan, substantially in the US. As the chart at the top shows, a lot of that tightening has unwound in the past week and, although there has been a small retightening after Powell’s speech, investors are comforted that the risks that policy is stuck have lessened given they gave back little of the previous eight days’ gains even though they had to – at the same time – grapple with the largest drop in forward earnings expectations for the coming quarter in years.

A fall in energy prices has also helped. For Europe and the UK, a decline in absolute prices is particularly helpful. It is nigh impossible to remove the effective energy surcharge that Russia’s actions have imposed on us but it is alleviated if energy is reduced in the proportion of overall production costs by making more effective use of it.

Declining commodity and energy costs are usually part of an economic slowdown. This time around, they add monetary policymakers’ ability to be responsive by reducing input inflation pressures.

This week brings the release of provisional inflation data, always an important piece of information, which feels even more important in the current environment. UK consumer prices rises are expected to have fallen back to 4.7% year-on-year, which should allow Prime Minister Rishi Sunak to claim a victory in his inflation pledge (to halve inflation from December 2022’s level of +10.5%). That will be less important than the signal it might send about the chances of rate cuts in the second half of 2024.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.