Market Update July: Transition Uncertainties

The great British summer may have struggled to materialise so far, but the end of the first half of the year always brings an element of sunny optimism. We will comment on market and investment returns in more detail next week, when the data has settled, but after what proved a quite decent 2020 for investors, the first half of 2021 has again left investors with plenty to be positive about. However, investors with a higher allocation to equities than bonds will have done much better than last year. Regular readers will know bond markets have been a decisive factor for stock markets this year and while compared to the first quarter of 2021 they have calmed down in the second quarter they remain a risk to lofty equity valuation levels.

The great British summer may have struggled to materialise so far, but the end of the first half of the year always brings an element of sunny optimism. We will comment on market and investment returns in more detail next week, when the data has settled, but after what proved a quite decent 2020 for investors, the first half of 2021 has again left investors with plenty to be positive about. However, investors with a higher allocation to equities than bonds will have done much better than last year. Regular readers will know bond markets have been a decisive factor for stock markets this year and while compared to the first quarter of 2021 they have calmed down in the second quarter they remain a risk to lofty equity valuation levels.

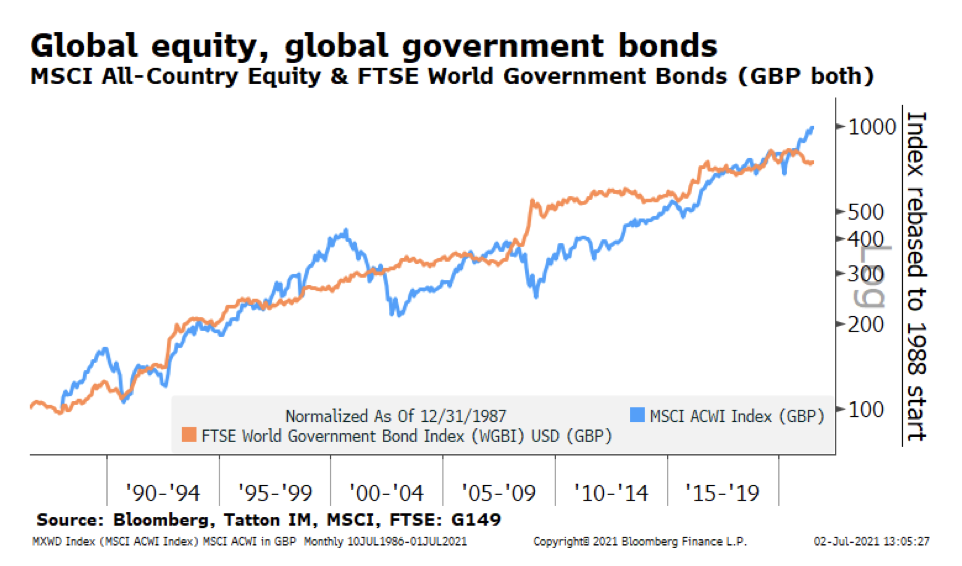

On the back of calmer bond markets – and a significant rebound of the global economy – the second quarter saw many equity markets close at all-time highs. Meanwhile, despite a notable recovery rally in the second quarter, bond investors have not had it quite so good. This poses an important question against historical observations. Can equities continue their rise despite a lack of upside for bonds?

The timescale of the chart below may distort things, however, the return boost that the relentless decline in bond yields provided bond holders over the past 40 years has meant that over this period stock market returns did not come at the expense of bond markets. The 1950s and 60s looked very different. Then, yields continually rose and drove down bond valuations while equities grew strongly. So perhaps we should pose the question differently: can the 2020s be like the 1950s and 60s?

It is certainly possible, but some of us may also remember the 1970s when out of hand inflation drove bond yields up at a much higher rate than before and stock markets suffered prolonged falls.

For the rest of this year, returns are more likely to be driven by the more immediate factor of the post-pandemic economic growth levels. On this point, last week’s record highs in economic sentiment survey data from around the western world confirmed that equity analysts have not been mistaken to expect exceptionally high 2021 corporate profit growth rates – which are underpinning stock market valuations (see also this week’s article ‘Global half-time review). At the same time, concerns have subsided for now that runaway levels of inflation are poised to push up bond yields and put equity valuations under pressure through rising discount factors for future earnings.

As we have noted over the past month, this environment of stock market positivity was driven by the expectation that the pandemic and its restrictions is gradually ebbing away, opening the path for an outsized economic catch-up rebound all the while central banks keep bond yields stable. However, the ebbing away of the pandemic also means the inevitable phasing out of the government and central bank support that bridged the past year’s economic void. This introduces a significant – and potentially unnerving – period of transition when the economy will have to stand on its own feet again.

Markets have already priced in much of the good to come from the pandemic really being behind us – at least in the west – and there may not be much patience if things do not improve in a straight upward line.

To be clear, it is our central case that the peak of the pandemic is now well behind us, and economic growth lies ahead, but we also expect to see bumps and humps on the way. For one, it has to be recognised that only the UK’s public health has so far successfully weathered the onslaught of a far more infectious variant against a widely vaccinated population, while the rest of the world is still where the UK was only six weeks ago – reopening as the rate of infection has declined to very low numbers. It is entirely possible that the rest take their insights from the benign impact on the public health this latest COVID wave has had on the UK, but it is just as conceivable that once infections there rise again, those in charge of public health react with renewed stringent restrictions out of fear that their lower vaccination rates make the UK experience inapplicable.

This is just one example of the uncertainties that lie ahead as we transition to the post-pandemic environment, and it will make it very difficult for politicians and central bankers to calibrate the pace of withdrawing support. All the while, capital markets will fret over whether the remaining support level are too much – stoking inflation and yields – or too little, undermining the economic outlook and corporate earnings.

Our relatively positive outlook is anchored on two things. First, even as variant scares temporarily slow progress, vaccines have forced the pandemic to retreat. As a consequence, the strong economic bounce back is set to continue, even if there may be the odd setback in the process. Second, central banks are determined to avoid letting inflation pressures (that come with a strong rebound of demand against a not yet fully operational supply side) deter them on their path back to sustained economic growth. This should mean corporate earnings continue to grow as strongly as currently expected, supporting markets, while yield levels should remain contained – thereby not undermining equity valuation levels either.

But to quote ex-US defence secretary Donald Rumsfeld, who passed away at 88 this week, there are “known unknowns” and “unknown unknowns” to be mindful of. Just as in his assessment of terrorist threats back in 2002, we can only take into account the known unknowns and steer our investment management actions accordingly. The potential blows of the unknown unknowns are the risks investors have to mitigate through their personal investment risk profiles and resultant asset allocations – as the first quarter of 2020 so starkly reminded us.

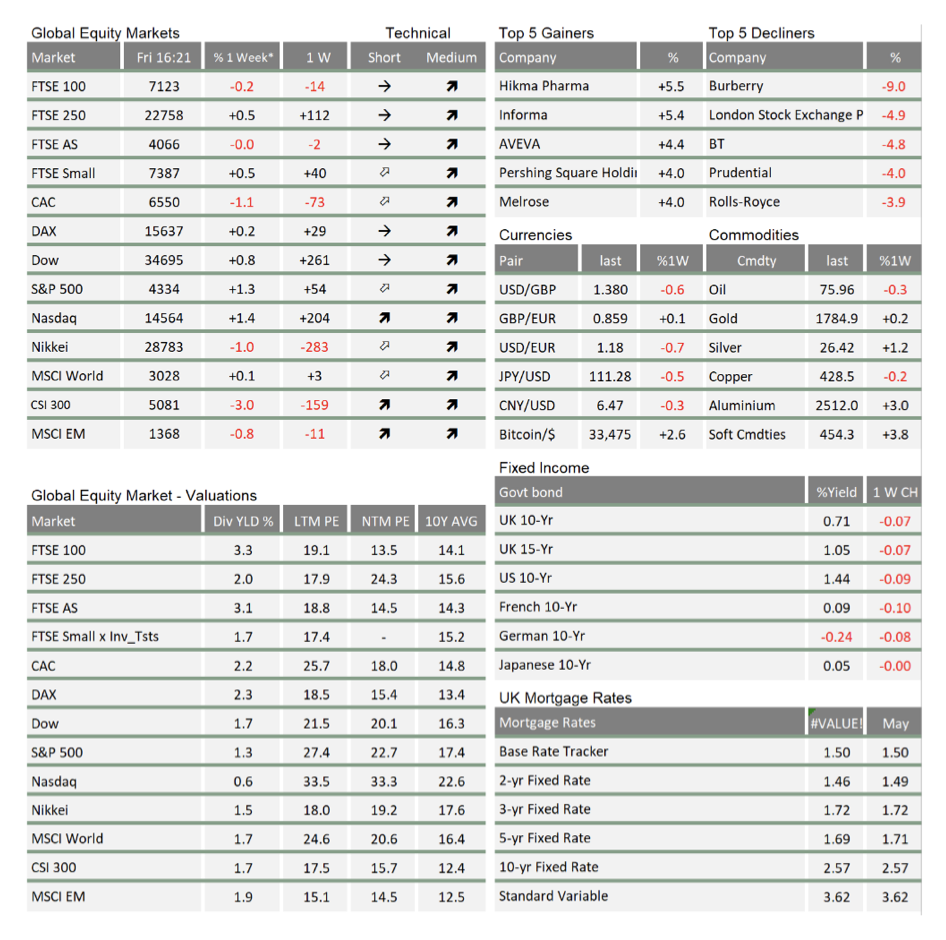

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.