Market Update: The Lagarde Pivot Hits Insecure Markets

We made the case last month that we disagree with the market maxim that “How January goes, so goes the year”, at least for 2022. After a disappointing January for investors, February made a promising start, only to revert to last month’s wild down and up trading pattern towards the end of the week. This was despite the week not having been dominated by the US Federal Reserve (Fed) or Russian manoeuvres (admittedly Boris Johnson was still big news – but only in the UK).

We made the case last month that we disagree with the market maxim that “How January goes, so goes the year”, at least for 2022. After a disappointing January for investors, February made a promising start, only to revert to last month’s wild down and up trading pattern towards the end of the week. This was despite the week not having been dominated by the US Federal Reserve (Fed) or Russian manoeuvres (admittedly Boris Johnson was still big news – but only in the UK).

Nevertheless, what unnerved markets on Thursday and Friday followed the same playbook as the market turbulence in January: central banks announcing their determination to no longer ignore inflation pressures and markets reckoning with the idea that the growth slowdown is slowly morphing into a growth slump. The main protagonists this week were the European Central Bank (ECB) and Meta (aka Facebook). The ECB’s president Lagarde (finally) declared that inflationary pressures had to be countered with a change in monetary policy towards a gradual tightening – not immediately, but in due course.

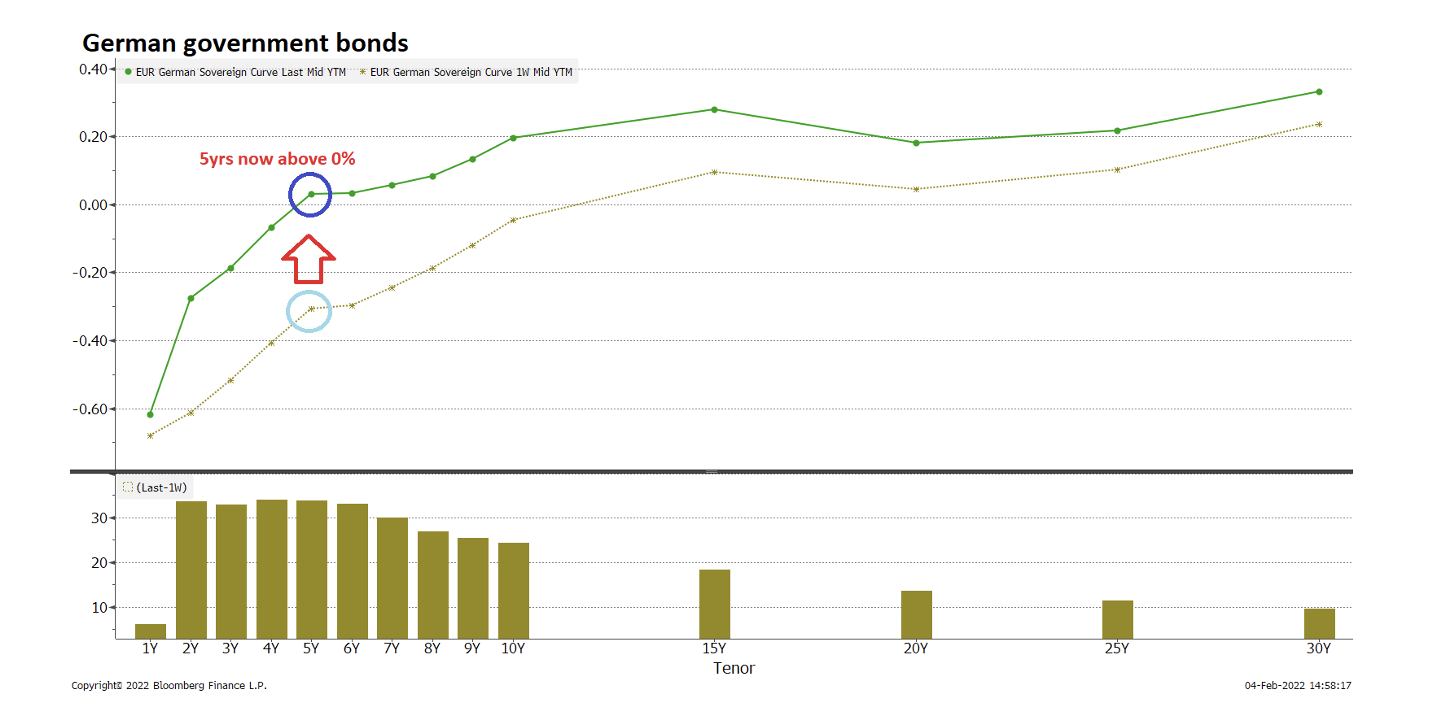

This followed the course prescribed by both the Fed and the Bank of England (BoE), and means that all major central banks, bar the People’s Bank of China have now pivoted from an easing to a tightening stance – although only the BoE has raised rates so far. Even without any actual tightening action, bond markets were quick to respond, as the chart below vividly illustrates. It shows the upward yield movement over the course of a week in bonds with maturities between one and 30 years.

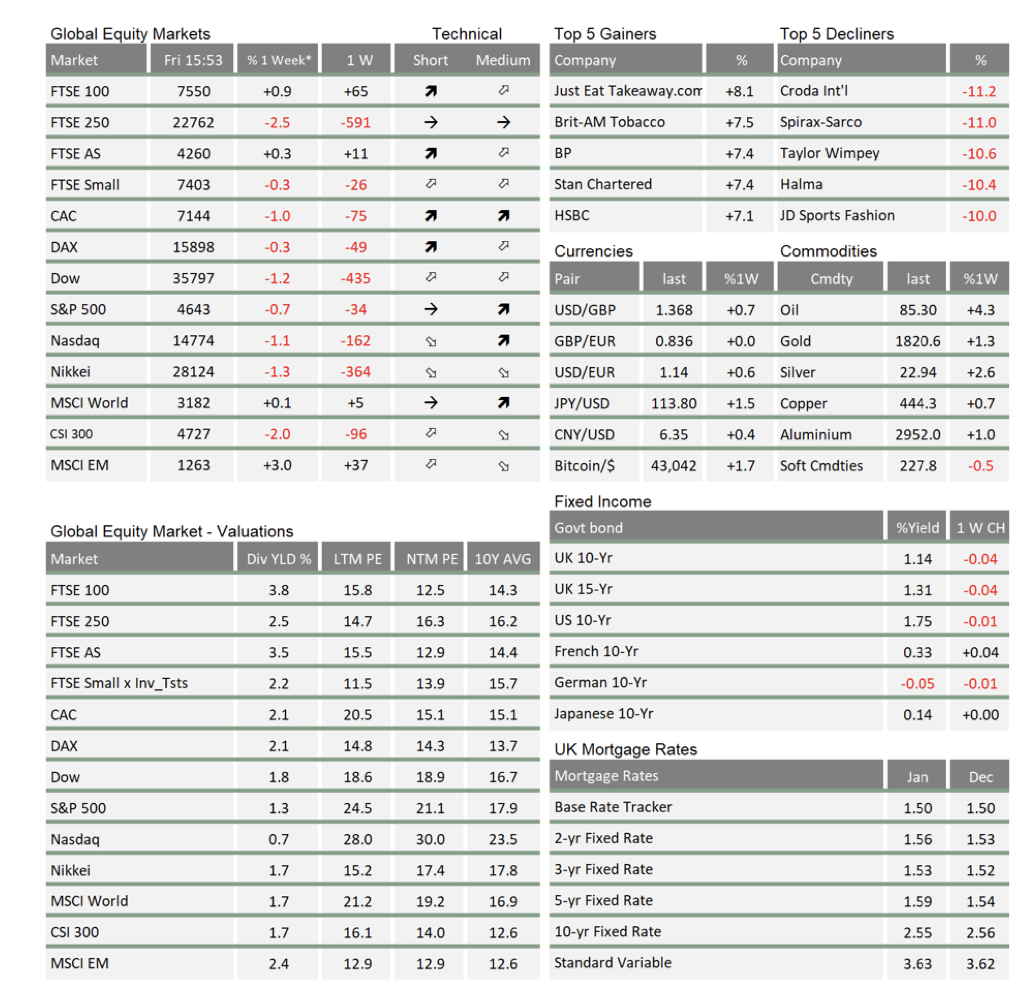

As regular readers will know, rising bond yields put downward pressure on stock market valuations, unless corporate profits (equities’ earnings yield) can grow faster than the rising yield effect has on their share price valuation metrics. This would explain why US mega-tech companies are currently getting so extraordinarily penalised when they report disappointing earnings growth. Meta – formerly known as Facebook – lost about 25% on Thursday after reporting it expected next quarter’s revenues to only increase somewhere between 3% and 11% (after last year’s first quarter near 50% increase that was clearly seen as ‘disaster territory’). The US S&P500 index fell 2.4% on the day, and commentators were quick to point out markets were pulled down by Meta’s falling advertising revenues pointing towards a distinct economic slowdown.

We would note that of the 2.4% fall, 1.1 percentage points (or 45% of the decline) was attributable just to Meta’s 25% slump – perhaps not surprising given we are talking about one the biggest of the US mega caps. Furthermore, Alphabet (Google) reported a 36% rise in advertising revenue for the same quarter – making Meta’s revenue growth slump look far more stock-specific than a more general economic indicator (See our separate article this week).

What do we make of the turbulent markets? Clearly investors are concerned central banks are pivoting towards monetary tightening exactly at the point when the economy is at risk of slowing further, sliding from a slowdown in growth that started after last year’s activity bounce-back into a more serious growth shock. Should the central banks stick to their guns as growth turns negative this would clearly be seen as constituting a central bank error – historically the most common reason for economic recession.

Market nervousness is therefore understandable, given the economic outlook has become far hazier than it was a year ago as the cycle has gone from its ‘early’ to ‘mid-cycle’ phase. Moreover, investors have no experience with post-global-pandemic recoveries to ground them, which only increases the level of uncertainty and insecurity.

We remain optimistic for portfolio investors for 2022 overall, although we admit that the outlook for the first quarter of the year is no longer looking positive. The shock to disposable consumer incomes from energy price rises is going to have a knock-on effect on corporate earnings, which may slow companies’ willingness to invest and spend. Interestingly, this dynamic makes aggressive central bank tightening action much less likely, as the job of curtailing demand to dampen demand-driven inflation pressure is taken out of their hands before they are forced to act. This is provided consumers are not able to compensate through higher wages – which would explain the BoE Governor’s explicit warning to UK citizens this week to resist the urge to ask for wage increases (See our separate article this week).

Cleary, central bankers, just like us, have very vivid memories/knowledge of the wage-price-inflation spiral dynamics of the 1970s, and are therefore doubly alert to the potential dangers we are now facing. However, this vividness of memories does not apply to the average consumer, and neither do we still have widespread collective wage bargaining structures that encourage blanket wage hikes. Here at Tatton, we discussed these matters intensively over the week and conclude, that while we cannot be entirely certain, we expect that the loud noises from central banks – together with the cacophony of the coming price shock or price-of-living-crisis – will see consumers tread more carefully with their spending plans, rather than all at once resigning from their jobs in pursuit of higher pay.

Spring still feels a long way away, and the next few weeks may continue to be both unnerving and somewhat unstable in capital markets. For now, all signs from the global economy point towards a blip, rather than a cycle-ending downturn. We have been in these situations before, and capital markets have tended to ‘look-through’ such periods when there were enough signs that the slowdown would ultimately prove temporary.

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.