Market Update: Talking recession to fight inflation

It has been another rocky ride week for capital markets, with inflation talk increasingly turning into chatter of an ‘inevitable’ recession, prompting the most recent cohort of DIY retail investors to throw in the towel. However, the thin trading volumes, plus the fact there’s no clear directional trend within stock markets, tells us institutional investors are staying put.

It has been another rocky ride week for capital markets, with inflation talk increasingly turning into chatter of an ‘inevitable’ recession, prompting the most recent cohort of DIY retail investors to throw in the towel. However, the thin trading volumes, plus the fact there’s no clear directional trend within stock markets, tells us institutional investors are staying put.

According to the most recent Bloomberg surveys, most of the leading economists in the US do not think a recession is imminent recession, and further evidence suggests inflation readings and high yield credit spreads have stabilised. So why is that the media is full of recession talk but long-term investors remain unconvinced?

Well, the recession talk has ramped up because central bankers have done such a good job in convincing us they are unafraid to choose inflation-fighting over growth support. US Federal Reserve (Fed) Chair Jay Powell confirmed it will keep raising rates until inflation is back under control. But this tough talk is not just confined to the Fed. Here in the UK, the Bank of England (BoE) Governor Andrew Bailey has been describing “apocalyptic” conditions, while Chief Economist Huw Pill’s belief that inflation won’t be brought under control before the end of the year tells us of similar determination.

Such verbal machismo by central bankers, threatening worse to come (unless we cut back spending and/or refrain from asking for pay rises), may be considered by central banks as a more effective short-term strategy to fight inflation by curbing consumer demand than the more blunt and time lagging instrument of a raft of rate hikes.

This is where economists and institutional investors may be taking their relative positivity from – the falling prospect of persistent rate rises and thereby the risk of recession which would pull the rug from under corporate earnings growth. The headline inflation figures may have been a shock for the general public, but were widely expected by markets, and therefore priced in. The fact that inflation numbers did not overshoot expectations, and were very clearly driven by quite explicit components (rather than being structural) was enough to lower recession expectations. These expectations are often best taken from the yield premium that the lowest-quality corporate borrowers must pay for their finance. After rising sharply over the past four weeks, there has been little indication of this yield premium going up further last week.

So, is Huw Pill mistaken in his belief that inflation will continue to rise (and thereby force the BoE into more painful rate rises)? It bears repeating that this inflation episode is driven by supply disruptions and Russia’s war on Ukraine leading to demand exceeding supply. Meanwhile, the labour market is very tight and consumers are willing to accept higher prices for non-essential goods while they still have excess savings from the pandemic. This has created the real risk of inflation once again turning structural, which explains the fervour from central banker.

While no one can know where Russia’s war will lead, we note that energy capacity and food supplies from other global regions are being redirected. For example, this week led to the UK having more liquified natural gas coming in than can be stored, used or passed on to the continent. High prices create powerful incentives in a market economy, and this is no exception. Another is the incentive for the Chinese leadership to regain the economic initiative, after their ‘Zero-COVID’ strategy blunders left China seriously behind its growth targets. President Xi’s government just announced a significant stimulus programme aimed at creating jobs by increasing manufacturing capacity. In the past this increase in supply has had a deflationary impact on global markets in finished goods.

It seems that the aggressive messaging from central bankers has been successful in driving down demand while global supply issues can be expected to continue to resolve. The European gas price issue may not be solvable before winter, but recent redirection efforts indicate that the longer- term fallout may be less than feared, while also stoking economic activity to prove to Vladimir Putin that Russia’s energy exports are not indispensable.

The continuation of last week’s story – of falling market implied inflation expectations that have taken bond yields down with them – has offered some evidence that the stagflation scare we read about in the media is mostly that. The price pressures we are all experiencing are unpleasant, but the economic and financial backdrop has much stronger parallels with the price pressures the US experienced just before the onset of the ‘Golden Fifties’, than the dire stagflation of the 1970s.

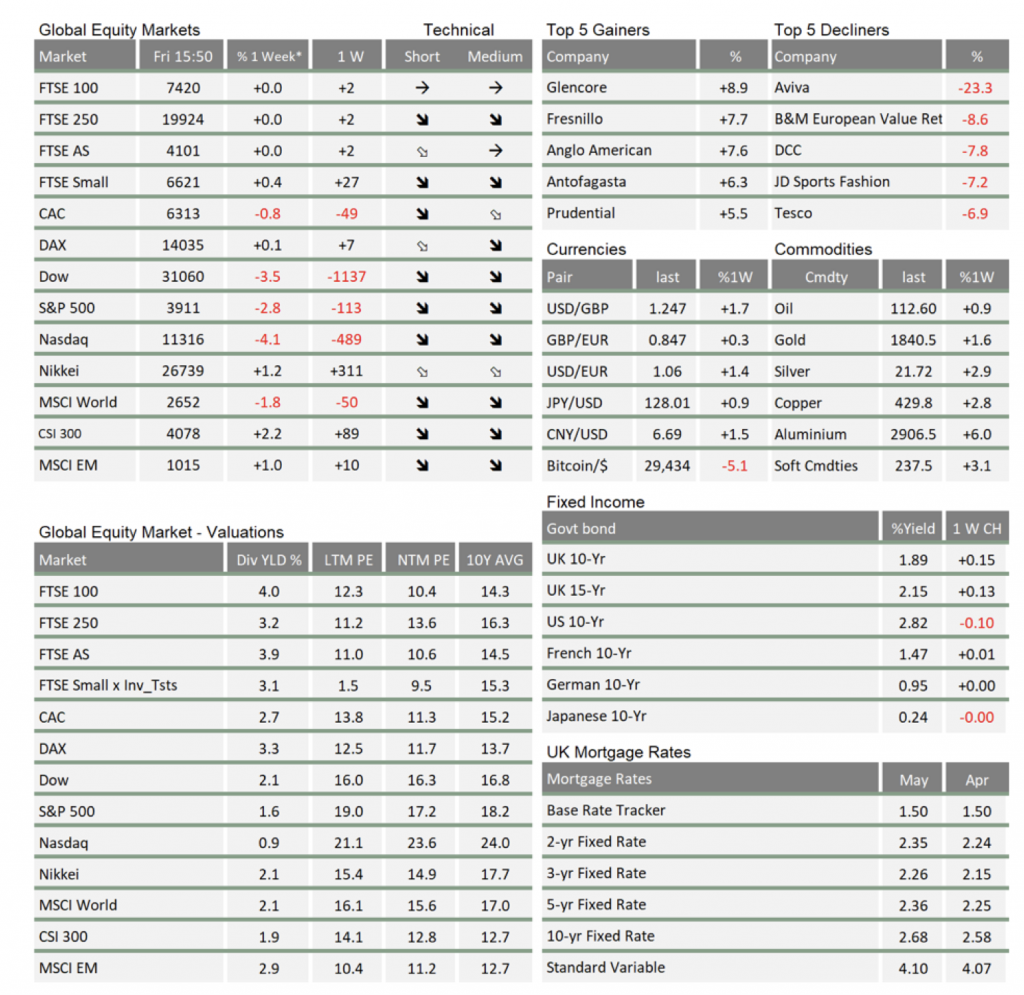

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.