Market Update: Mood Swings

For some time, bond and equity markets have been experiencing teenager-like mood swings. As February ended and March began, government bond yields continued their march higher to levels last seen last autumn, when stock markets tumbled as a result. Yet this time, stock markets have ricocheted between optimism, namely the surprising resilience of consumer demand and resulting relative company earnings stability, and pessimism that the same economic resilience will keep inflation pressures high, forcing central banks to keep raising rates higher for longer, which undermines valuations and said resilience.

For equity and bond markets, the last week of February was not so good, as the inflation focus dominated, whereas this week focus shifted back to more positive growth indicators, resulting in an improvement at least for equity markets. China’s equity market – which was a drag last week – was in a happier place this week. Meanwhile, the bad mood in the pan-European bond market worsened last week. While Europe’s economy has avoided an outright energy crisis, and delivered some positive economic updates, the unfortunate of this is a creeping back up of inflation. Closer to home, the UK saw the prospect of recovering trade relations with its largest trading partner on the back of the positively perceived ‘Windsor Framework’ proposals for solving the Northern Ireland trade and sovereignty conflict.

We observe that, of late markets, are behaving in a less predictable fashion than in the ten years or so between the Great Financial Crisis and the Covid outbreak . During that period, investors became used to the idea that “rates can rise, but equities remain robust” because periods of rising rates were few and the rise in rates was small. It took only a small amount of tightening and economic slowdown to remind households that their jobs may be at risk and that a new job (at comparable pay) could be tough to find. Analysts would say that although there might be mini-economic cycles, the global economy was broadly operating below potential output – or in their jargon ‘with deflationary slack’ – as spare capacity could always easily be called up.

It may be that the monetary policies of the 2010s did a good job in stoking demand but did little to stoke productive investment to increase capacity, that the spare capacity was labour and, just before the pandemic struck, it had finally become scarce. It may also be that the virus had a significant impact in reducing the global economy’s spare productive capacity, as businesses have become keen to diversify their supply chain dependencies.

In the 2010s, growth could pick up without signs of inflation, but the 2020s are proving different. The latest purchasing manager index (PMI) reports of business expectations showed that global growth had returned in February but that it (quite literally) came at a cost. Despite falling energy prices, input cost pressures rose, a sign that even the smallest amount of growth takes us back to a position where there is little or no spare capacity. That view was backed up by German, French and Spanish inflation data which showed a surprising rebound, especially given that companies’ energy bills should have fallen somewhat.

For the central banks, therefore, this information has been enough to warrant another round of warnings that rates will probably have to go higher and stay there for longer. In the US, there is growing talk of a return of a jumbo 0.5% rate rise step on 22 March. The European Central Bank (ECB), had already told us rates would rise by 0.5% on 16 March, but could be tempted to go to a deposit rate of 3.25%, a rise of 0.75%.

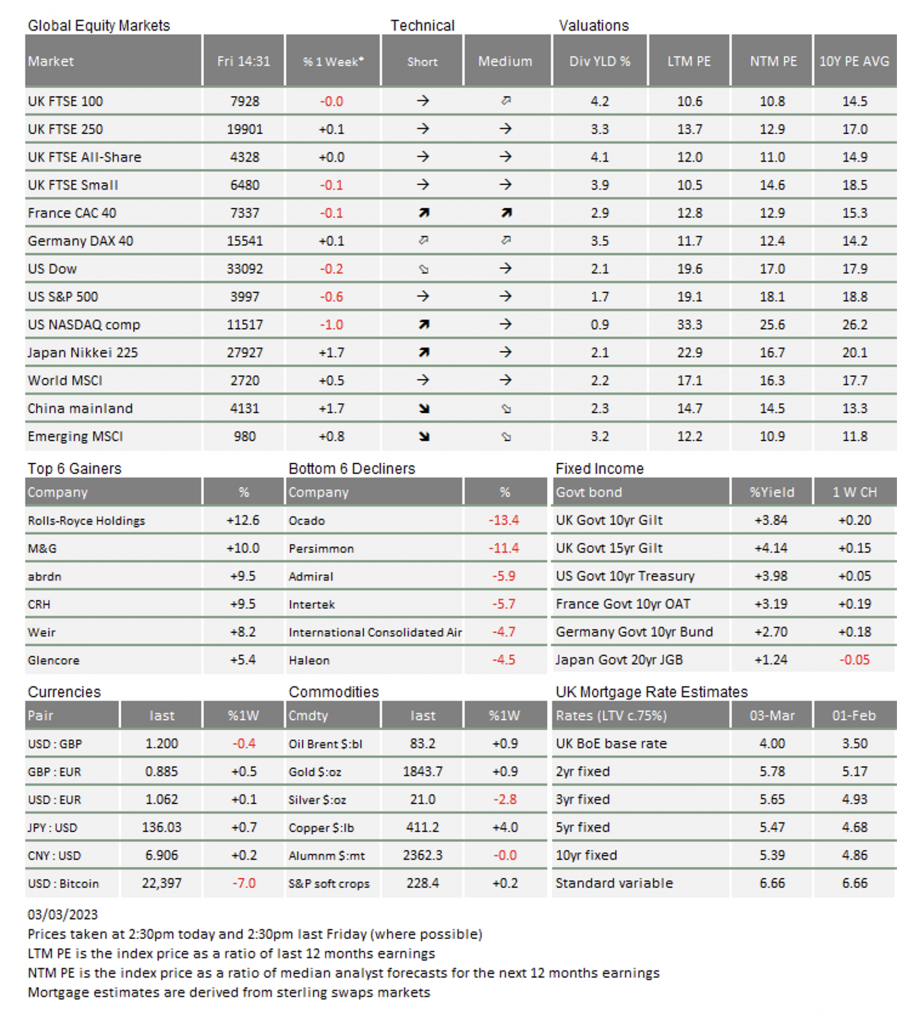

On the back of this, bond yields rose again, with ten-year US Treasuries decisively breaching 4% for the first time since last November and German ten-year Bunds for the first time up to 2.7%. It is worth remembering that it was only a year ago that German yields stopped being negative.

Higher government bond yields are problematic for other asset classes since they form an important part of market valuations. However, on the stock-specific side, analysts form a view on each stock’s price by looking at the expected profit flow. Should that expected profit flow start to improve because growth is improving, it might be that the higher degree of confidence offsets the effect of higher yields marking down the value of longer profit streams.

Indeed, last week, investors seem to have become less worried about demand falling off a cliff. Even with the impact of higher yields, confidence in the resilience of economies and household spending has improved – in terms of that looming recession, we are not even close to a downwards spiral.

We have sympathy with this view. When one looks back at equity valuations of 20 years ago, the breadth of corporate profitability was strong amid the higher yields of the time. That confidence in the resilience of an economy which had a broad balance between supply and demand allowed investors to expect more certainty in profit growth. We think that the stronger confidence was key in allowing equity valuations to be higher (more expensive) than now.

In recent weeks, we have talked about how equities are expensively valued which makes them riskier. But, as you can tell, we are mindful they might only be expensive in terms of the last 20 years, a short period in the general history of investment.

Equally, we know that saying “it’s different this time” is a dangerous thing. Equity markets are still in a risky position, particularly if consumer demand was to eventually buckle and corporates were no longer able to maintain profits. However, if profit growth confidence is starting to improve – as we had some reason to believe last week – then we could see reasonable upside from current levels.

In the coming weeks, we will be watching for rhetoric about Taiwan and Ukraine. There is no doubt both will be discussed, but the key issue is whether the west is put in a more difficult position in the near term. We think Beijing will be careful to avoid inflaming a damaging rise in tensions now, just as growth seems to be re-establishing. However, we know that they have often surprised us as well…

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.