Market Update: Markets take good news in their stride

In previous weeks, we’ve noted how the absence of specifically good news meant markets reacted more negatively than expected to the relatively low probability of a US debt default. We pointed out that the more notable event of the weeks have been bond yields once again surging.

Last week, not only did we get a resolution to the US debt ceiling brinkmanship, but also the welcome news that inflation pressures across Europe were declining faster than expected, while the US jobs market remains paradoxically both vibrant and at the same time showing signs of slowing down (with unemployment going back up). Unsurprisingly stock markets staged a brief relief rally on the debt ceiling resolution, but began wobbling again when Chinese, US and European manufacturing sentiment data showed sure signs of contraction.

On the back of this, bond yields stopped their ascent and declined over the course of the week on the expectation that the economic headwinds in goods manufacturing should persuade central bankers to stop hiking rates. The extraordinarily robust US job market figures last Friday did not appear to change this narrative for bonds, while equities took the strong economic news as outright positive for a change. This came despite expectations for the first rate cut being yet again pushed out further into the future – now only expected for January 2024 (Back in January this year it was implied for the middle of the year).

It is heartening to observe how much more, compared to last year, equity markets are taking the return to higher yield levels in their stride. Particularly notable is that the growth companies of the tech sector, whose valuations suffered substantially last year under rising yields, seem to no longer be seen as growth companies this year, but safe haven investments, almost regardless of how sky-high their valuations (versus actual earnings) are – perhaps as a longer term structural play. Markets appear to accept that rates and yields are unlikely to come down in the very near future as inflation proves stickier than anticipated. Yet in combination with a still booming services sector compensating against the activity slowdown wave in manufacturing, the notion that the global economy will avoid a painful inflation-busting recession became once again the narrative of the week.

There is little doubt in our mind (and analysis) that higher rates and higher yields for longer will leave more collateral damage in their wake. However, the unique post-pandemic set of economic variables has created ample monetary liquidity constantly searching for a better return, paired with plentiful jobs – and a higher-than-usual debt resilience of the proverbial weak links of the economy – pushing out recession expectations ever further. Perhaps to the point where manufacturing’s overstocking in reaction to the post-pandemic demand surge has worked its way through and the service sector catches up to the same demand saturation level that manufacturing has painfully experienced since last year.

Concerns over China’s lacklustre reopening recovery have been weighing heavily on China’s stock market and have been one of the major recent risks in the hope for a global economic soft landing. This week’s news that Beijing is working on a sizeable property sector support package seems to be precisely what investors were looking for, given the jump with which Chinese stock markets reacted to the news.

In all, it was a good week for the optimists, and to justify their equity buying they would point towards the wider market expectation that yields will fall in the medium term, making equities more attractive versus bonds again (and therefore not worrying too much over the profits squeeze hiatus in the interim). As to the already seriously expensive US stock market, those optimists would argue this is mainly driven by those companies that will shape our society’s future, and therefore justify the hefty premium.

Pessimists will point to the higher-for-longer risks emanating from high interest rates and lending costs eventually driving down demand (and profits), causing a recession-triggering debt default cycle. They might also point out that US tech firms will have to generate almighty profits in the future to justify the current valuation hype.

The ‘jury’ of high ranking forecasters remain split but this past week held more for optimists than pessimists. Whether it will stay this way over the coming weeks remains uncertain and will from week to week be driven by the interaction between falling goods and resource prices and the stickiness in core inflation driven by the ongoing labour shortage. Stay tuned.

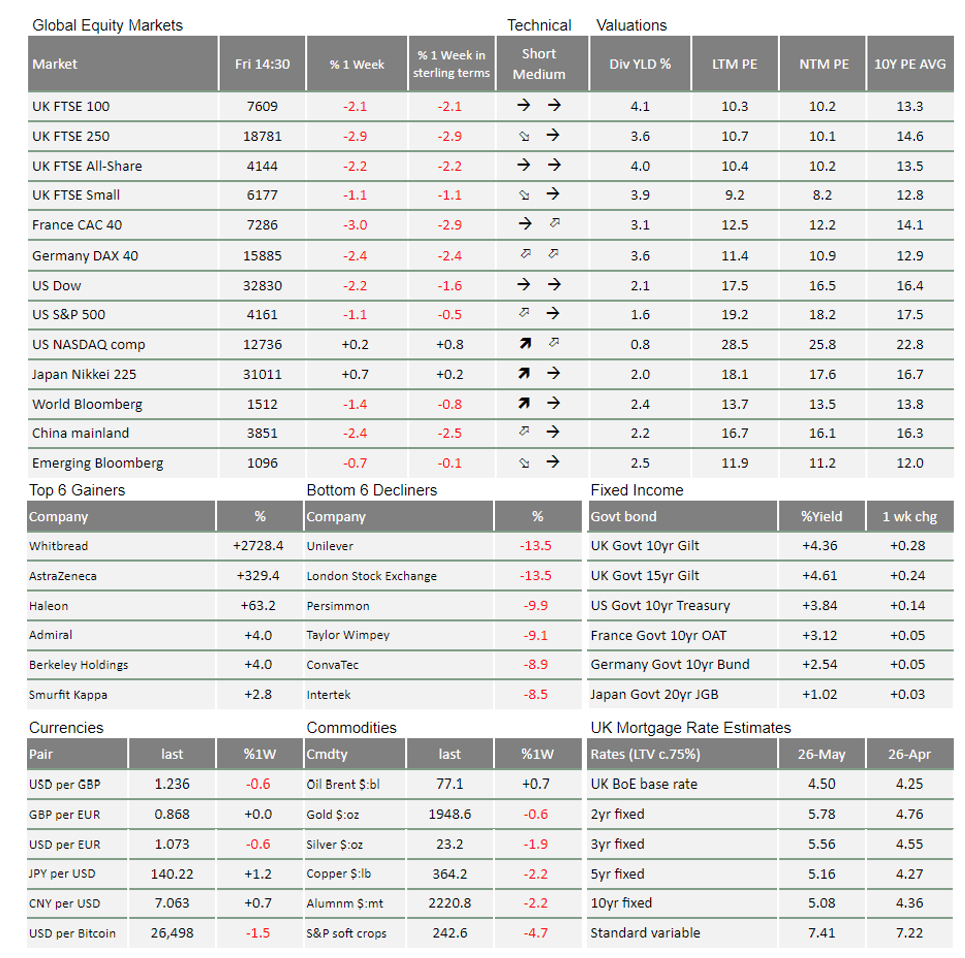

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.

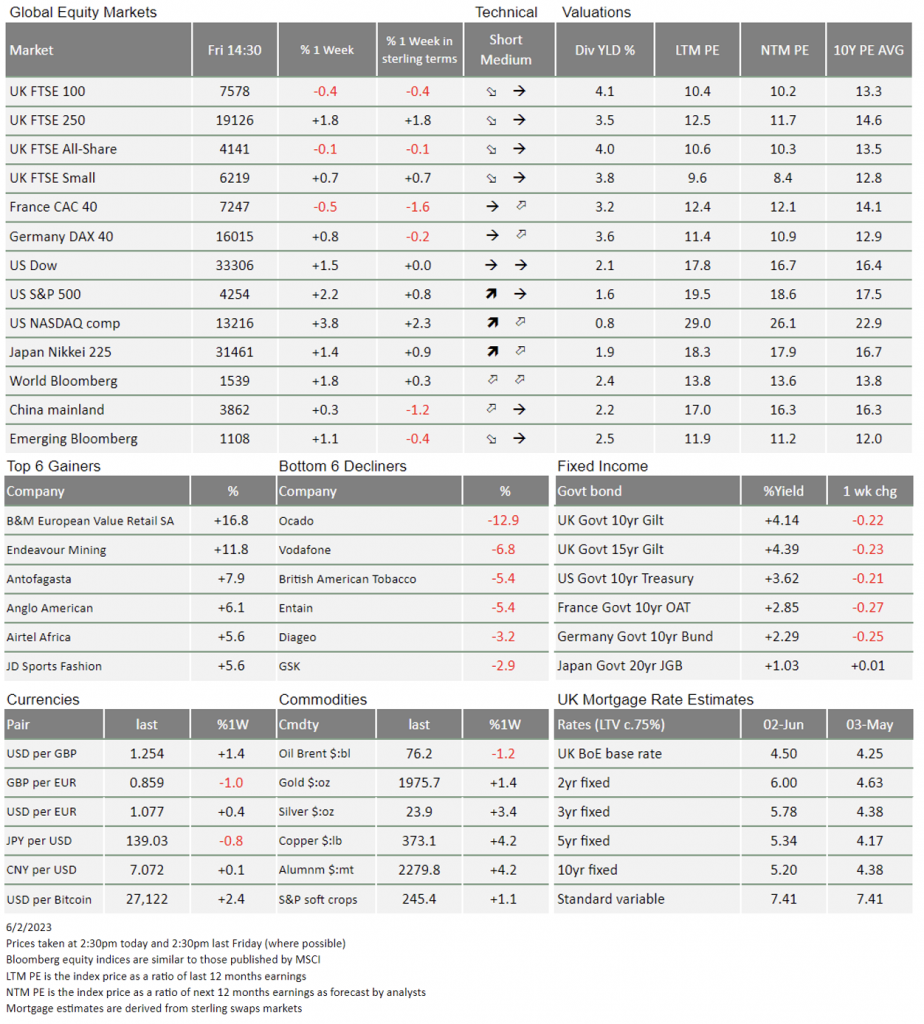

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.