Market Update: Known winner, unknown outcomes

Known winner, unknown outcomes

Compared to last time, Trump’s election win immediately spurred stock markets, however, the bond market reaction tells a more nuanced story.What does Beijing do now?

China’s struggling economy will not welcome Trump’s win as that will bring export damaging tariffs, just as signals of recovery appear.

Compared to last time, Trump’s election win immediately spurred stock markets, however, the bond market reaction tells a more nuanced story.What does Beijing do now?

China’s struggling economy will not welcome Trump’s win as that will bring export damaging tariffs, just as signals of recovery appear.

US debt risk

We dig deeper into why US government bonds, the lowest risk government bonds in the market, are showing signs of stress.

For the sake of investors, we hoped for a quickly resolved US election, and we got one. Capital markets responded well to Donald Trump’s surprisingly decisive win, with US stocks rallying from Wednesday on. Investors deemed it good news for the US, but less so for Europe and the UK, whose stocks had a tougher week. This side of the Atlantic, equities and currencies sold off and underperformed rampant US markets by a remarkable 5%.

Investors expect more tax cuts and a generally easier environment for American businesses – particularly for top Trump surrogate Elon Musk, whose Tesla shares soared nearly 20% last week. But there are still uncertainties ahead in a second Trump presidency. We expect some risks but potentially also higher rewards for US risk assets in the medium-term.

Tax cuts before tariffs?

Avid stock market watcher Donald Trump will feel vindicated by the record highs of the S&P 500 last week. It is fair to say that markets are excited, but the post-election rally was amplified by investors’ recent de-risking ahead of what looked like an uncertain vote. There will be no fight to overturn this election, and Trump’s Republican party are favourites for a ‘clean sweep’ (control of the White House, Senate and House of Representatives), increasing the probability of promised tax changes. That clarity and lack of instability helped unlock pent up demand for risk assets.

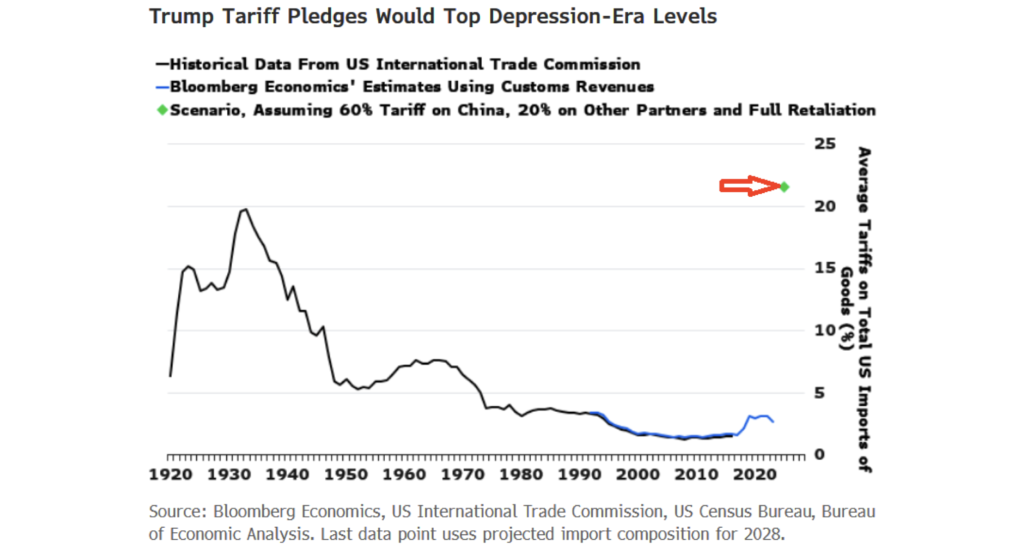

Policy details are still uncertain, though. Trump was elected on an anti-immigration platform, but the influx of 5 million migrants since the pandemic has been a driving force for its economic outperformance – as well as the recent fall in wage inflation pressures. The president-elect also promised high tariffs during the campaign, which economists argued would push up inflation. The tariff numbers he suggested far exceed those introduced in his first term. As the graph below shows, it would raise average mark-up for American imports to its highest ever level.

Of course, the sheer size of that potential impact should lead us to doubt whether Trump would actually raise tariffs so high – at least in the short-term, considering his big campaign promise to lower inflation. The timeline of Trump’s policy changes matter just as much for the American economy as the changes themselves. If tariffs and mass deportations happened before his promised supply-side improvements took effect, the result would be higher inflation and lower growth. This suggests that stimulatory measures like tax cuts will come before the restrictive measures. That would be a rational approach to fulfilling his campaign promises in the face of economic reality – but we know that predicting what a Trump administration will do is difficult.

Less tax revenue will mean more government debt in the short term – the impacts of which we discuss in a separate article. Over the long-term, Trump is likely to cut government spending, particularly if Republicans achieve a clean sweep. Trump adviser Elon Musk talked about cutting trillions from the federal budget. The idea is to improve the productivity of government spending rather than simply gut it, but even so, the magnitude of such cuts would inevitably dampen growth. Whatever happens depends on who else gets appointed to the cabinet.

Germany’s political collapse could mark its economic nadir.

Speaking of political uncertainty, Germany’s governmental collapse this week over a budget disagreement could have a major impact on the European economy. An election is likely in the next few months, and after a painful hit to living standards for the worst off we expect the mainstream parties to promise protectionist policies, to prevent the right-wing populist movement gaining ground.

The political problem is strongly linked to Germany’s underlying economic problem: it suffered a cost shock and a revenue drought at the same time. Europe’s largest economy benefitted substantially over decades from cheap Russian energy, but the post-Ukraine adjustment has been extremely tough. To make matters worse, the prolonged recession in global manufacturing – caused by Chinese overproduction and ‘dumping’ – is weighing on German manufacturers. Profits are being squeezed from both sides, resulting in job losses while living costs are still rising.

There are signs that both sides of that problem could improve, however. Trump’s victory makes it more likely that Ukraine will be forced to cede territory to Russia (if only by default, as with Crimea before) in return for an end of a nearly three-year war. We might not like that outcome, but it would mean a reduction in immediate conflict, and hence less pressure on European energy prices. Meanwhile, the Chinese government has recognised the need to support domestic demand with a $1.4 trillion stimulus package this week (to which we dedicate a separate article) which could signal an end to overproduction. Germany’s cost and revenue pressures might ease simultaneously. We just hope there will be a rational, functioning government to guide toward that light at the end of the tunnel.

UK bonds will keep following the US – for now.

It shows how important the political news has been that we are near the end of this article without mentioning this week’s interest rate cuts. The US Federal Reserve and the Bank of England both lowered rates by 0.25 percentage points on Thursday, as markets fully anticipated. Fed chair Powell refused to speculate on the potential policy impacts from a second Trump term, but he did note that material changes to US debt dynamics would have to be taken into account. Bond yields came down after the Fed’s cut, having risen on the election news.

Although last week’s autumn budget increased Britain’s medium-term inflation outlook, UK bonds continue to be dominated by those US yield moves. The budget pushed UK bond yields above their US counterparts, but the two central banks remain in lockstep and the two markets are unlikely to diverge much, as the US and UK are thought to have similar inflation pressures. It also helped that BoE governor Bailey continues to sound relatively dovish (preferring lower rates) in press conferences.

The US-UK bond relationship could shift long-term, however. Britain’s growth and inflation outlook is tied much more closely to struggling Europe, while the UK government’s fiscal stance will probably remain more prudent, despite last week’s budget being clearly expansionary.

Meanwhile, we have spoken about the long-term bond market risks that could come from a second Trump presidency, which could keep US yields relatively more elevated. For the time being, however, any move up in US yields is likely to do the same to UK yields, which could cause some headwinds.

Trump was the 45th president and will be the 47th president of the United States.

Trump will not be inaugurated until January 20th, but his transition team (headed by Cantor Fitzgerald’s Howard Lutnick) will appoint a cabinet before then that will probably be very different to his first term. His victory address characterised the next four years as “promises made, promises kept”, perhaps out of a sense of disappointment with his first term. His early tax cuts had significant economic impacts, but many felt that the constant sense of turbulence and drama were significant barriers to achieving more. Now he has another chance, perhaps a better idea of what he wants to do and, almost certainly, a unified legislature with which to do it.

If he is to bring anything to fruition, he needs his cabinet to be adept and stable for the whole term. Thus, investors will look for the team to be credible and for the incoming President to allow them to set policy detail. In particular, policy implementation of policy has to be coordinated, to avoid destabilising the economy. Markets are betting that he is likely to succeed. We hope so.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.