Market Update: Equities and bonds go separate ways

Equities and bonds go separate ways

Despite US Thanksgiving downtime, global markets remained dynamic as they anticipate what the changing political framework may mean for the economy and government debt.Terrifying Tariffs

Trump’s social media announcement of 25% tariffs on Canada and Mexico created shockwaves, but is this all a high stakes starting point for a deal?

Despite US Thanksgiving downtime, global markets remained dynamic as they anticipate what the changing political framework may mean for the economy and government debt.Terrifying Tariffs

Trump’s social media announcement of 25% tariffs on Canada and Mexico created shockwaves, but is this all a high stakes starting point for a deal?

New US Treasury’s target of threes

Markets love incoming US Treasury Secretary Scott Bessent’s 3% targets to cut the US deficit, increase electricity production and boost GDP. Too good to be true?Global financial markets appreciate the USA’s Thanksgiving holiday, which tends to be the quietest of its unique holidays. Markets can be frenetic in the lead up though, as it proved last week.

Although developed market equities were calm in sterling terms, stocks were more turbulent in local currencies. France was notably hit by the fragmenting of its ruling parliamentary “alliance”. Emerging markets were even less happy, partly thanks to Trump. Brazil was the weakest, after President Lula announced softer-than-expected spending cuts, threatening future fiscal stability.

Japanese stocks were volatile, opening Wednesday’s trading down 2.5% from Friday’s level in Yen terms. This was directly offset (indeed, probably caused) by currency strength. The Yen notably strengthened against the US dollar, going from Y154.5 to Y150 (meaning it takes fewer Yen to buy $1). Since Wednesday’s weak opening, however, both the Nikkei 225 index and our more favoured TOPIX index are up by 1% in yen terms and 1.5% in Sterling terms.

It seems to us that bonds and equities are being driven by differing narratives at the moment, particularly in the US. Commentary around economic growth is resolutely upbeat, helping equities. Meanwhile, the narrative around government debt has turned more positive but driven by the idea that the deficit may fall.

Lower US bond yields, which made the Yen more attractive, were caused by Donald Trump’s nomination for Treasury Secretary, Scott Bessent. For bond markets, this is the most credible nomination Trump could have made. The erstwhile hedge fund manager has many fans. Some liken him to Reagan’s Treasury Secretary, the legendary James Baker, others think he’s more like Santa, expecting his nomination to gift further gains for US equities through December.

(Bessent worked for George Soros in the 1990s and as his CIO between 2011 and 2015, is well regarded on Wall Street for his level headedness during periods of global market upheaval with a profound knowledge of the inner working of the global economic framework)

His “3-3-3” plan is to raise growth to 3%, cut the government deficit to 3% and increase energy production by an equivalent of 3 million oil barrels per day, all by 2028. This is probably not achievable but the investors see the aspiration as good for policy in each area. “3-4-1” is more achievable and less likely to risk a recession.

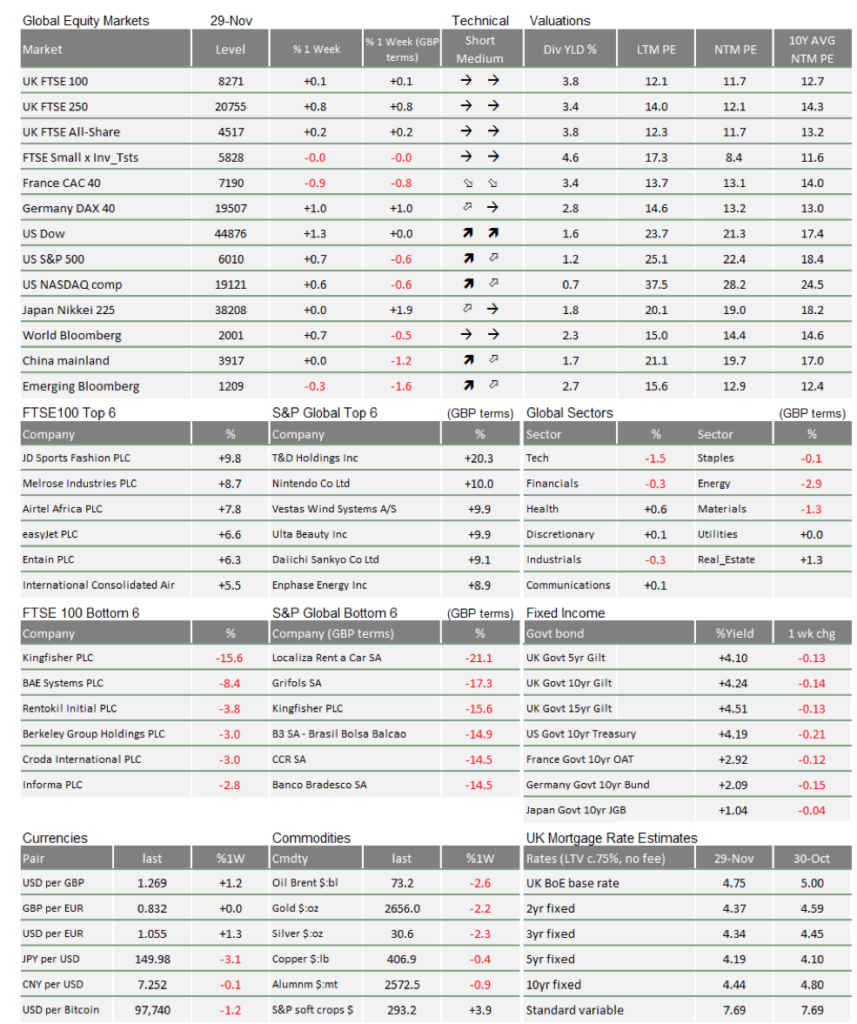

Regardless, the US 10-year treasury yield which had risen significantly from 3.8% since Trump’s election, dipped sharply to below 4.25%, with commentators linking the move to Bessent’s deficit reduction target. The spread to swaps, which we use as a measure of Treasury market credit risk, fell back to +0.52% from the previous week’s 0.57%.

Still, risk-free 10-year real yields (inflation hedged) also fell noticeably from 1.52% to 1.41%. That signals investors are less afraid of fiscal laxity, but less convinced about longer-term growth too.

Bessent wants growth through deregulation, and the last “3” on his plan – energy disinflation through increased supply – is a significant part. Bessent’s framework sees energy (electricity generation) as the supply constraint holding back US growth in a technological world, and Trump calls the solution “energy dominance”.

If inflation falls consistently below 2%, Fed interest rates should be relatively accommodative, keeping interest costs and bond yields well below nominal growth. That in turn should allow companies to borrow at attractive rates, making businesses more viable. The government could also reduce its debt load (at least relative to GDP) and lower its debt servicing expenses. The consequence would be rising corporate debt but higher levels of private business investment.

All of this paints a rosy picture and, perhaps counterintuitively, one that could benefit Europe and the UK. However much the US is struggling for energy supply, we are struggling more – Europe-wide wholesale electricity prices are about four times those of the US. If US prices fall, ours should fall by a similar proportion. The fall in Europe’s energy costs could therefore be four times greater than the US. The wider question, though, is the damage this does to emission reduction targets, and how much environmental disruption undermines the growth targets.

Even if the US puts up tariffs, the biggest barriers for European growth are internal supply constraints and productivity. If those go down, European growth should benefit – so a win for the US should be a win for Europe too, as long as politics doesn’t prevent it.

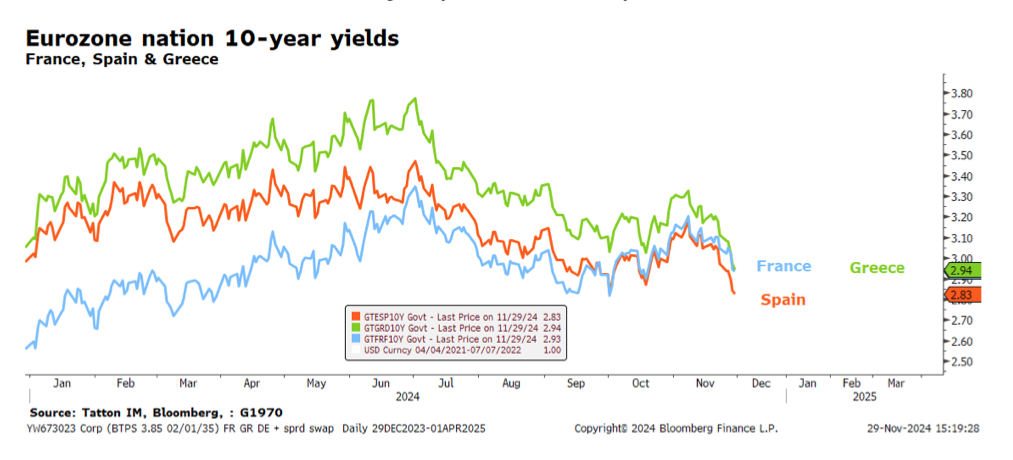

Politics, unfortunately, is an issue. France’s continued politic maelstrom looks similar to the US in recent years, the political right battling for cheaper energy while facing what they see as “lawfare”.

Yesterday (Thursday 28th November) after extreme pressure from his coalition partners in Le Pen’s Rassemblement National, Prime Minister Barnier rescinded his proposed electricity tax at a budget cost of €3.8bn. The legal action against Le Pen that is putting her on edge (she is accused of embezzling EU funds) could not come at a worse moment for Barnier’s fragile coalition. That threatens to derail attempts to bring down France’s unsustainably high budget deficit.

Investors see France as struggling more than the rest of Europe. Government bond yields fell across the Eurozone, thanks to falling US yields, but French yields did not shift as much.

The big political conundrum – in the UK, Europe and US – is now how to tighten budgets back to pre-pandemic levels without hurting jobs or smaller businesses. France’s electricity tax was unpopular, as is the UK’s decision to tax jobs – although Chancellor Rachel Reeves can more credibly say there will be no more.

The fact that the UK government will almost certainly be stable and internally cohesive for more than four years also helps. The US is nominally in the same position, but many doubt Trump’s administration will be internally cohesive, as we discussed the week before last.

Europe’s political instability is a problem. At the moment, it seems that the old mainstream political forces of the centre and left cannot form cohesive alliances, so new populist forces could gain more influence next year. Germany’s early elections takes place on 23rd February and it is unclear how a reconstituted “rainbow” coalition could work with CDU’s Merz as leader. Meanwhile, France is surely set for another election.

Investors do not see much upside in Europe, but there are seeds of positivity, which could grow into bullishness in the spring.

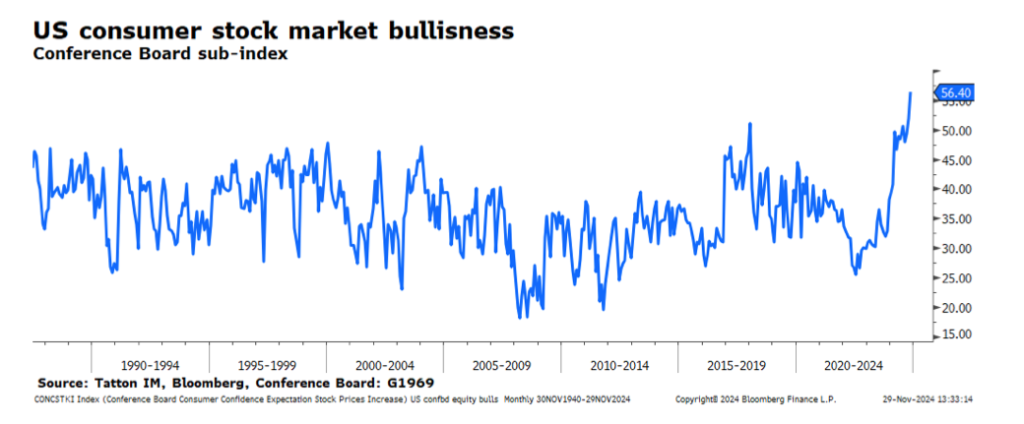

Lastly, we note that some (but not all) measures of bullish market sentiment are reaching extremes. Last week, the US Conference Board published its Consumer Confidence indices, which includes a measure of consumers’ expectations for stock market price rises. The chart below shows the current historically unprecedented bullishness:

Signals of potential exuberance are not great timing indicators, yet one shouldn’t expect that such bullishness will mean imminent disappointment. The same was true in March and July but selling US equities would have not been a good decision. Nevertheless, it could lead to higher volatility if we do see disappointments. We remain cautiously optimistic, as we have been since the start of the year.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.