Market Update: Energy Price Shock Turns Into Central Bank Focal Point

![]() More than two years since the COVID virus hit Europe, it is clear that most peoples’ livelihoods have been affected more by the policy ‘medicine’ than the virus itself. Of course, without those interventions which were needed until vaccinations become prevalent, it most likely would have been the other way around. As we start the second half of 2022, the excess monetary liquidity now draining from markets – the unavoidable consequence of those pandemic-fighting measures – is hitting the global real economy and thus lowered market valuations.

More than two years since the COVID virus hit Europe, it is clear that most peoples’ livelihoods have been affected more by the policy ‘medicine’ than the virus itself. Of course, without those interventions which were needed until vaccinations become prevalent, it most likely would have been the other way around. As we start the second half of 2022, the excess monetary liquidity now draining from markets – the unavoidable consequence of those pandemic-fighting measures – is hitting the global real economy and thus lowered market valuations.

It also must be acknowledged that more than one threat has presented itself this year. If the world was merely facing the consequences of natural disaster such as the virus, we would probably be heading towards normality by now. As we enter the second half of 2022, the energy price crisis caused by Russia’s geopolitical provocations has likely turned into the biggest problem now. Russia’s invasion of Ukraine is the most obvious aspect. For Europe, the impact is felt most clearly through the disruption to our energy markets.

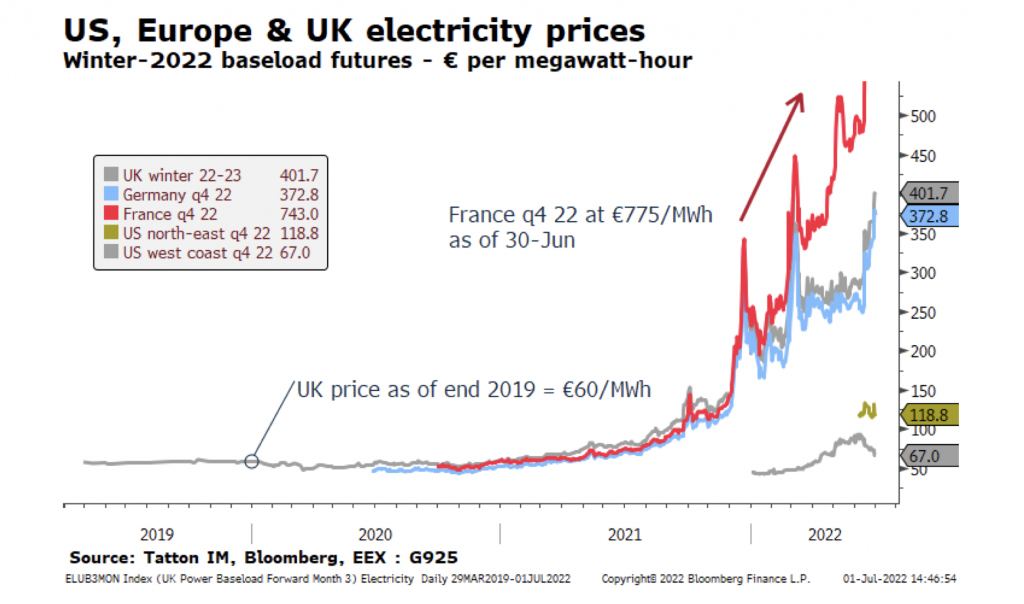

The chart below shows how this coming winter’s anticipated electricity prices for the US, Europe and UK compare. In 2019, across the western nations, energy (electricity, heating and petrol) was around 6% of household expenditure, similar for service businesses, and about 12% for manufacturing (US Bureau of Labor Statistics Consumer Expenditure Survey, ONS, Eurostat).

The past 12-month average for Germany has been about €180/MWh. Looking beyond the winter, Germany’s electricity contract price for the whole of 2023 is at €290/MWh, and 2024 is at €190/MWh. Europe’s dilemma is clear. Russia’s hold on the price of energy appears significant and while those effects can be mitigated in the long-term, they are difficult to avoid in the near or even medium-term.

This places considerable pressure on businesses and their profit margins. It also means that sales revenues are likely to suffer as consumers fret over their household budgets as the extra expenses diminish their savings.

Although admittedly less than in Europe, US businesses and households are also under price pressures, as demonstrated by the latest personal consumption expenditure data. Consumers increased dollar spending in May versus April by just 0.2% and bought less goods. Inflation adjusted (real) expenditure dropped by about 0.4%.

If businesses are not selling as much they will be forced to hold back costs. Capital investment will be put on hold and only essential hiring will take place.

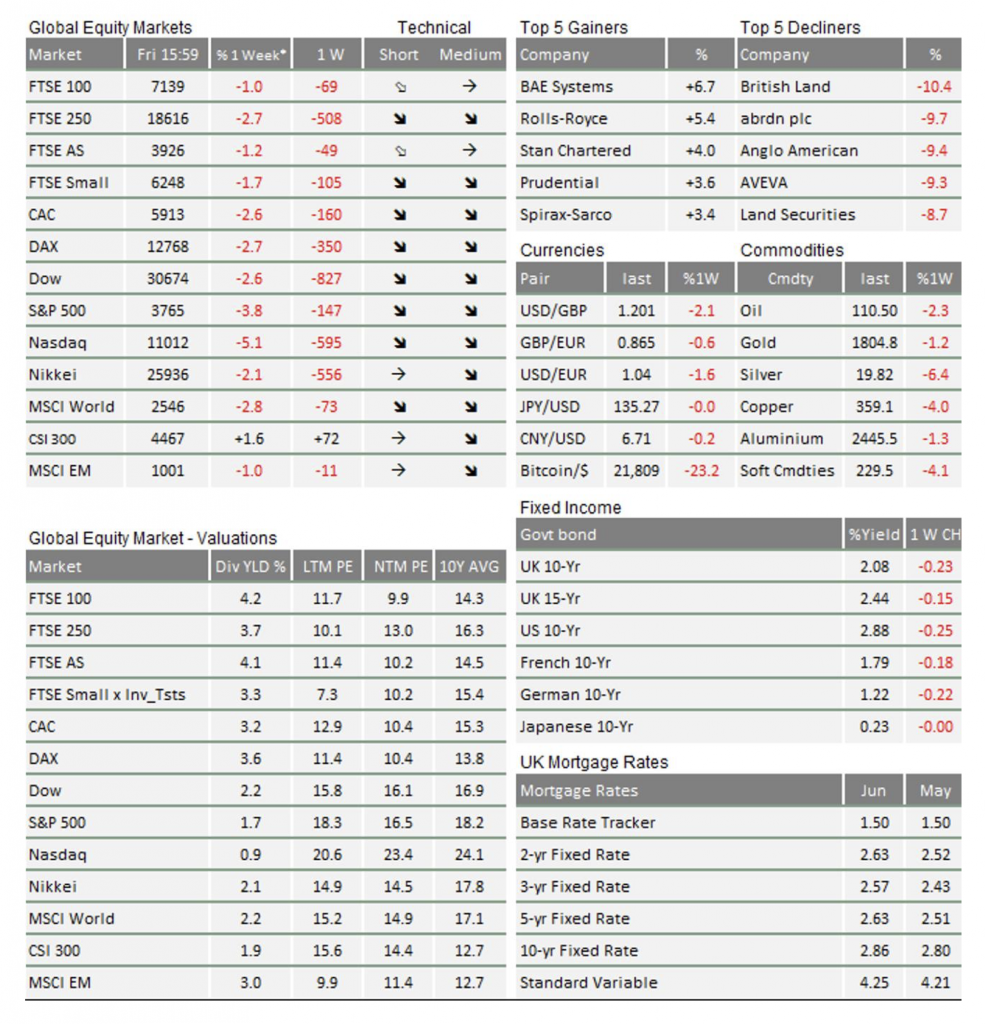

Markets already sense the slowing of growth is upon us, and it is being reflected in government bond yields. The ten-year US Treasury yield has moved back down to 2.90%, having traded briefly at 3.50% about two weeks ago.

This move has been matched by the fall in the German ten-year Bund from 1.90% to below 1.30%, and the UK ten-year Gilt from 2.73% to 2.13%. Although 0.6% may not sound a big number, in the context of today’s bond markets it constitutes a substantial move.

Markets have shifted inflation expectations lower by about 0.3- 0.4%. Rising energy costs would usually be associated with rises in inflation expectations. However, we are now observing a big shift – energy cost rises are having the same impact on markets as rising taxes.

Nevertheless, the rhetoric coming from this week’s big central bank get-together in Portugal remained resolutely hawkish. But markets are already sensing that inflation-boosting growth is in the process of slowing quickly enough now to warrant a softening in central bank guidance towards the autumn. As for the other crucial inflation variable – tight labour markets – there are early signs of subsiding employment demand across western nations. When those are reasonably clear, central bankers may tell us they have succeeded in preventing supply chain disruptions and the energy price shock from mutating into a vicious cycle of 1970’s style structural inflation.

We expect that the European Central Bank (ECB) will still want to raise rates this month – there were several speakers at the Portugal meeting suggesting a 0.5% repo rate rise – and they may well keep going from there. Interestingly, however, these rate increases will happen while the ECB continues to purchase assets. What it takes with one hand, it gives with the other, and that rather incongruous policy is helping to hold back rising credit spreads in the weaker peripheral nations.

Still, the negative effects of the energy war Russia is waging on Europe may be softened somewhat for the weakest nations by such monetary policy moves. However, while European governments may want to turn on the fiscal taps to help households and businesses, the policy effectively channels money into Russia’s war-chest, unless there is also an increase in energy supply from elsewhere.

This places the onus on fast expansion of tanker capacity to the US and others, and on building better political relationships the Middle East and North Africa. Across the globe, there are major initiatives to secure new partnerships, coalitions, alliances, call them what you will. Maybe, for the UK and the EU, it will also provide an incentive to bury the hatchet and return to a more pragmatic relationship model.

As always, we know that challenges usually drive change as well. Indeed, we write below about how China seems to be heading out of its recent trough. We know as well that risk also tends to mean greater potential returns. As we enter the second half of 2022, market participants are certainly downbeat, reflected in lower price-to-earnings multiples and higher credit spreads. A resolution of the conflict with Russia is very unlikely anytime soon, but securing other energy supplies is possible. If and when that happens, the headwinds blowing against the global economy should slacken considerably.

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.