Market Update September: End of the Re-Opening Honeymoon

We are halfway through September and investors have not experienced a continuation of the positive returns picture of the summer months. This is despite COVID restrictions gradually lifting (not only in the UK) and an on-track economic recovery resulting in record numbers of jobs and demand outstripping supply in many places. To be sure, investment portfolios are only marginally down for the month and still sitting on very healthy return cushions for the year so far. However, as noted in recent weeks, economic growth momentum has hit a bit of an air pocket and talk has died down about the imminent arrival of the ‘Roaring Twenties’.

We are halfway through September and investors have not experienced a continuation of the positive returns picture of the summer months. This is despite COVID restrictions gradually lifting (not only in the UK) and an on-track economic recovery resulting in record numbers of jobs and demand outstripping supply in many places. To be sure, investment portfolios are only marginally down for the month and still sitting on very healthy return cushions for the year so far. However, as noted in recent weeks, economic growth momentum has hit a bit of an air pocket and talk has died down about the imminent arrival of the ‘Roaring Twenties’.

Is it that the spreading of the vaccine-busting Delta variant and the persistent supply bottlenecks have reversed expectations of a better and stronger economic outlook? Well, not so fast. The disappointing geopolitical newflow (Afghanistan; this week’s exclusively anglo-saxon nuclear submarine pact against China), does not apply to the global economic data flow.

A global shortage of labour, rising wages and healthy corporate investment plans may ring alarm bells with inflation hawks, but more level-headed economists attribute this to a confluence of indicators of persistent growth, not stagflation. As always, there are various threats to the positive scenario – this week the most keenly-debated threat was the rapidly rising cost of energy, which conjured up the spectre of a 1970’s-type price shock. This week’s Tatton Weekly therefore features a special insight article dedicated to why energy prices matter, but also notes how positive market forces have the ability to correct the cyclical overshooting of prices that is so characteristic for commodity markets.

The fact is that the recent phase of extraordinarily steep economic growth has now most likely come to an end. What follows now is a transition phase during which both households and businesses have to get used to once again standing on their own feet, as the fiscal and monetary support issued by governments and central banks is gradually withdrawn. Just as people have been feeling uneasy about getting back on crowded public transport and returning to their workplaces, this transition is just as likely to spread the sense of uncertainty.

In this environment, every dark cloud on the economic horizon can be viewed as a potential perfect storm that will surely see our fragile economic equilibrium collapse like a house of cards. It is undeniable that political and central bank leaders bear a larger than normal amount of responsibility for the future path of economic development, but the current state of the global economy is most likely less fragile than it might appear. With strong demand for labour strengthening consumers’ purchasing power over and beyond the savings surpluses they have been able to build during the lockdown periods, and the climate challenge mobilising pubic and private investment , there is hardly anybody suggesting this cycle is already nearing the end.

That does not mean that the summer’s ‘Goldilocks’ environment is about to return to capital markets. Corporate earnings expectation have recently moderated, while bond yields are likely to see further upwards pressures as price-driving supply bottlenecks persist, and with central banks inclined to reduce their yield-constraining support measures. This limits further upside for risk assets in 2021 over and beyond what has already been achieved so far, in anticipation of exactly the economic conditions we have arrived at.

On the other hand, just as markets had projected the recovery with their relentless buoyedness during the dark lockdown months of the year, they have also rotated towards sectors that thrive even when economic growth is not so rampant. On that front, various indicators suggest the negative sentiment turn may have already bottomed.

In the months ahead, much will hinge on the dynamics that define the interaction between bond yields and equity valuations. We continue to believe that at current depressed yield levels, equity valuations are not excessive even if they seem so in purely historical comparison terms. If, however, yields begin to rise more strongly than corporate earnings can outpace them, market conditions could become more unnerving again. At the moment we see not much indication that central banks are inclined to deviate from their view that current price inflation is transitory, but as we said earlier, every dark cloud at the moment…

We therefore expect that for the rest of the year investors may experience more of what we have seen so far in September – bumpy sidewards movement until the true likely upward trajectory of the economic recovery path becomes clearer and more acceptable again.

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

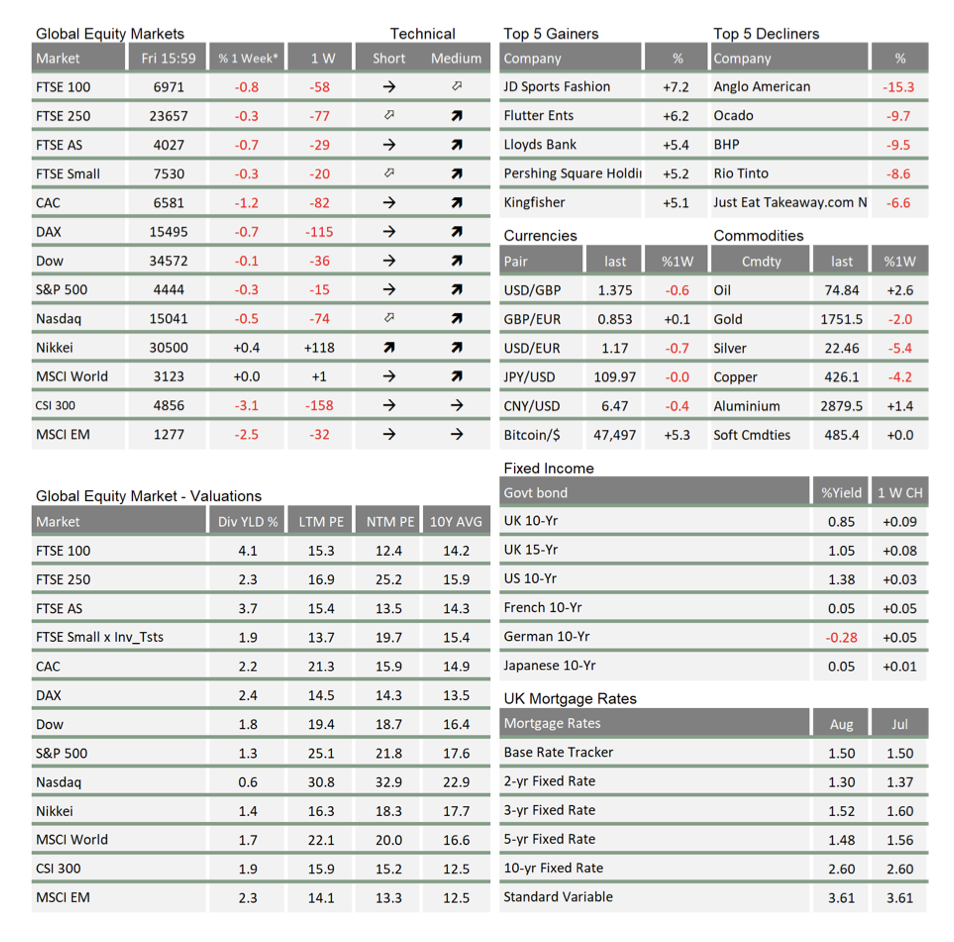

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.