Market Update: Big tech stocks increase is ‘artificial’

Last week we wrote that markets were facing growing risks. Since then, and at the time of writing, equity markets have generally headed higher. Japan has been enjoying a particularly good run with the Nikkei 225 making gains every day since last Wednesday. This has occurred despite some disappointing economic data and a weakening currency (we’ll return to the currency moves in a moment). However, the most notable moves have been in US stocks, with the large-cap tech names doing very well in aggregate.

The earnings reports for Q1 have almost all been published, and have surpassed the usual ‘better-than-expected’ level. We all know companies manage to ‘beat’ the near-term expectations of bottom-up analysts, sometimes at the expense of the next quarter’s forecasts. However, on a market-cap-weighted basis, developed world stocks have seen a return to earnings growth in the forecasts for the next 12 months. That’s after six months of analysts seeing falls in earnings.

In Europe, HSBC analysts note that cyclical sectors have been the winner while real estate has been the laggard. They see a swing in momentum and their forecasts have improved through the late part of the earning season to about an 8% annualised growth rate. Still, the 2023 forecast as a whole is muted at just 1% compared to 2022. Companies continue to be hit by higher interest rates and HSBC is concerned that the European Central Bank (ECB) may keep tightening financial conditions through the summer.

In the US, retailers have been discussing the continued softening of spending trends for big-ticket and other discretionary items. The pandemic reversal is till releasing pent-up demand for services, though, particularly when it comes to travel and entertainment.

But for both regions, what stands out as surprising is that ‘top-line’ revenues are better than expected. In Europe margins are still under pressure, but sales are substantially improved. In the US, both sales and margins have started to improve. That tallies with a more stable economic environment, especially for Europe where energy price declines have helped greatly. The improvement in global service sector purchasing manager indices (PMIs) also helps explain the corporate positivity. Meanwhile, Goldman Sachs notes that three themes have dominated earnings calls: banking stress, returning cash to shareholders, and artificial intelligence.

Exposure to regional banks and potential impacts on credit availability remains a focus for mid-caps and smaller companies. Most continue to want to pay back cash through share buybacks and dividends, although financials appear less keen.

Artificial intelligence (AI) is the hottest of topics. Although potentially encompassing many different aspects, most companies are talking about the use and development of chatbot (large language model engine) applications. Management teams talk about the potential business impact, current uses and plans for investments. Here there’s a split. For some service companies, AI is a threat because, for the customer companies, it offers a great opportunity to cut costs. But, as Goldman Sachs noted in a discussion yesterday, there are few companies for whom AI represents a direct profit opportunity. Goldmans suggests the main winners are hardware manufacturers at the cutting edge of fast computing, followed by the software techs that have investment capital – at least $1 billion in to put into research and development. And then you still need access to huge proprietary data.

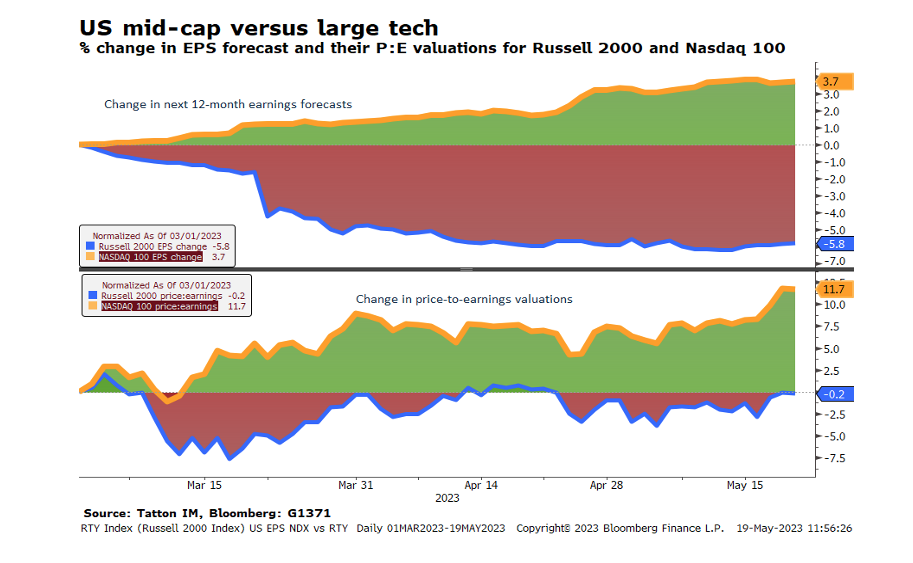

It’s no surprise then the stocks that have done best recently are hardware companies like NVIDIA and the behemoths: Microsoft, Amazon and Alphabet. The NASDAQ 100 contains many of these winners. The first panel of the chart below compares this index to the US Russell 2000 mid-cap index, showing earnings forecast changes since the start of this earnings season. The panel below shows the price-to-earnings multiples. For the NASDAQ 100, both earnings forecasts and the multiples have improved. For the more interest rate-sensitive mid-caps, both have declined.

The outperformance of large tech comes at a point when yields are not low, and have risen in recent days. As such, the move feels a bit like the start of the dotcom bubble, as Bank of America points out. However, for many investors, it is still a defensive move. The rise in US large cap techs is redolent of past times where risks to economic growth were substantial. And this week has seen other indications that investors are feeling a little downbeat.

The outperformance of large tech comes at a point when yields are not low, and have risen in recent days. As such, the move feels a bit like the start of the dotcom bubble, as Bank of America points out. However, for many investors, it is still a defensive move. The rise in US large cap techs is redolent of past times where risks to economic growth were substantial. And this week has seen other indications that investors are feeling a little downbeat.

The US dollar has moved quite sharply stronger after some weeks of weakening against most currencies. We write about this below. While there are several idiosyncratic reasons for emerging market currencies to soften, all except the Brazilian real have been on a downward path. The worst is the South African rand, 2022’s equity market darling. China’s renminbi has also taken a fall today (Friday 19th) after the authorities signalled an acceptance of move through RMB 7/$. The scramble for offshore dollars seems to us to be a signal of tightening liquidity.

The good earnings results in the US – and especially Europe – are hopeful. Still, the underlying tightness of financial conditions for many companies remains, while the AI theme seems to be equivalent to a narrowing of profitability breadth, at least for the moment. The rise in equity markets is welcome and, if caused by a general improvement in profitability, all the better. We would feel a whole lot more optimistic if central banks were less hawkish.

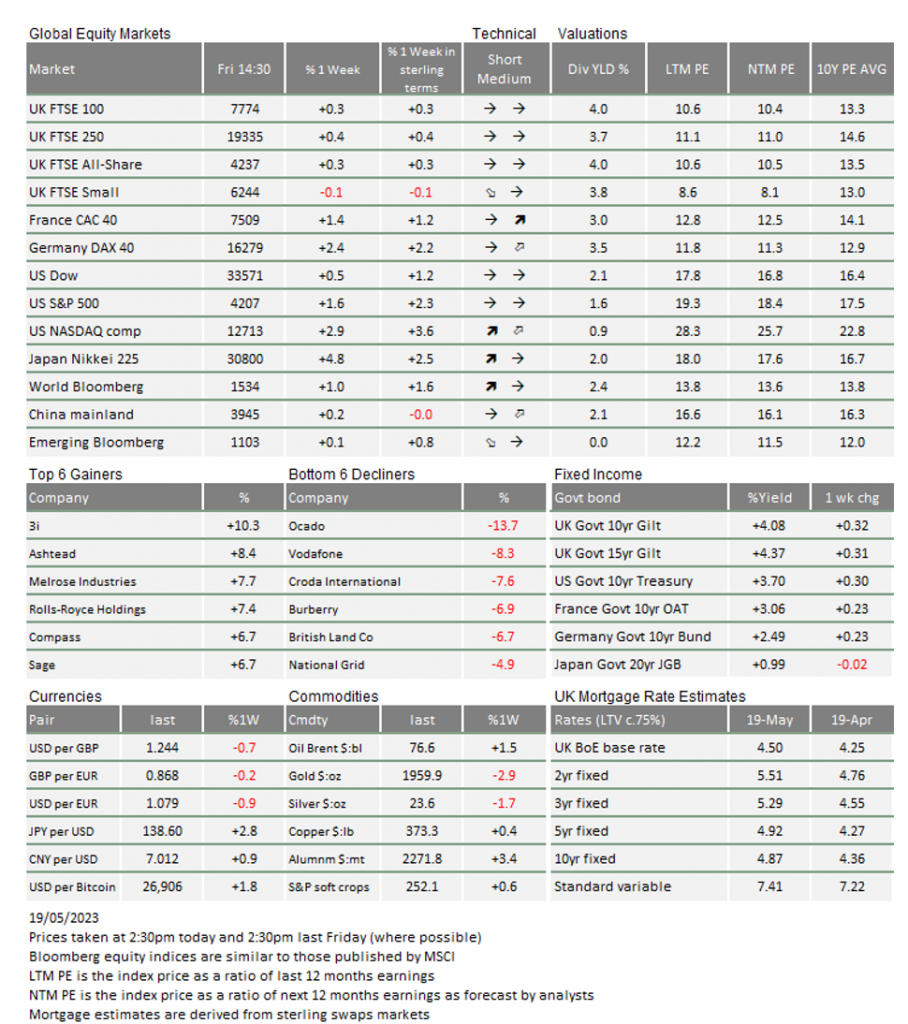

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.