Market Update: A Bumpy Road to Somewhere

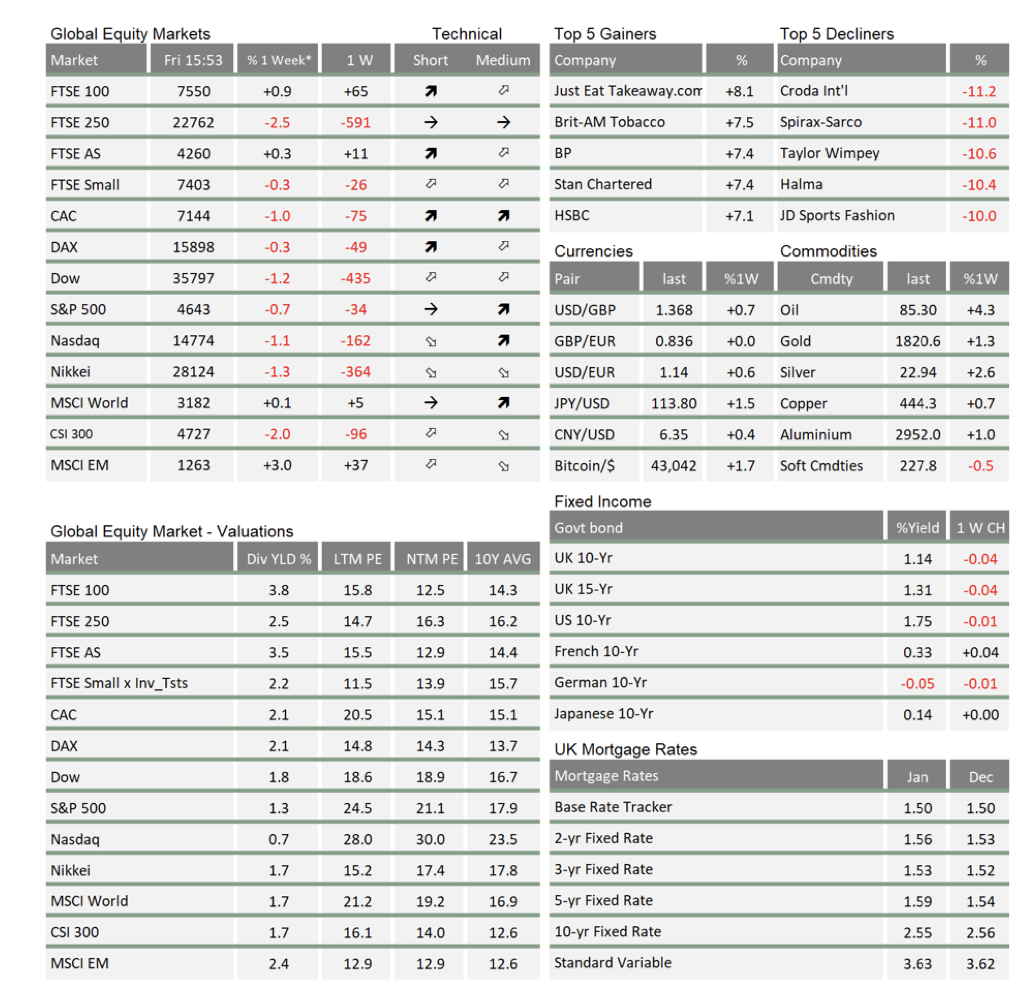

It has been an all-action year so far. Global equity markets have been in a downward trend since the end of 2021, led by US stocks. America’s mega-cap tech companies that were so loved throughout the pandemic have taken the biggest hit – with the tech-heavy Nasdaq falling nearly 10% in January. The change of fortunes was made abundantly clear on Friday morning after stock market darling Netflix plummeted 20% in pre-market trading after a warning on subscriber growth. UK equities seemed immune to the downturn in the first two weeks of the year, but that changed this week as the FTSE 100 joined the broader fall.

The global economy has been similarly tumultuous. There are early indications that the intense supply-side pressures we saw last year are easing – with input costs no longer spiking and supply chains freeing up. But that shows little sign yet of feeding through into inflation data. Prices are still spiking across most major economies, and consumers face a daunting shock to their real disposable incomes in the next few months. Meanwhile, growth is slowing, and central banks are removing their emergency support (more on this in a separate article).

All of this is without mentioning politics. The inescapable rollercoaster ride that is Boris Johnson’s premiership rattles on – but for how much longer is impossible to say. The pressure on the Prime Minister continues to build as MPs defect or denounce him and fresh allegations emerge. What we can be confident about is the fact that investors are unphased either way. Judging by market moves, the UK economy is not expected to be much affected by change in Downing Street – even if the government’s COVID policies are a source of market optimism.

That may seem an odd expectation, given the position the government is in. ‘Partygate’ is the highest profile problem for the Tories, but just as worrying for them is the cost-of-living crisis around the corner. The squeeze on real incomes will almost certainly see them lose some support from the ‘red wall’ voters gained from Labour in 2019. Meanwhile, plans to raise taxes to their highest level in decades does not play well to their traditional base. Any new leader is likely to face calls for a snap General Election, and with the explosive combination mentioned, there is no telling how that could end.

At the same time, though, markets’ indifference to Westminster drama is understandable. There is still a fair (though diminishing) chance that the Prime Minister will weather the storm. Or, if he doesn’t, that a continuity candidate replaces him, and no snap election is called. The status quo would then be restored and current events would be forgotten.

On a bigger geopolitical scale, all eyes are on Russian-Ukrainian tensions with its repercussions on the relationship with NATO members. The threat of destabilising conflict is significant, and Russian financial markets have reacted negatively. Government bond spreads have widened, and the stock market underperformed its Western peers. Global markets seem more pre-occupied with their own troubles though, as the big pandemic winners adjust their earnings outlook to a world without stay-at-home policies, and most importantly, the tightening stance from the US Federal Reserve (Fed). All in all, it seems global markets expect the significant political volatility will not affect the status quo.

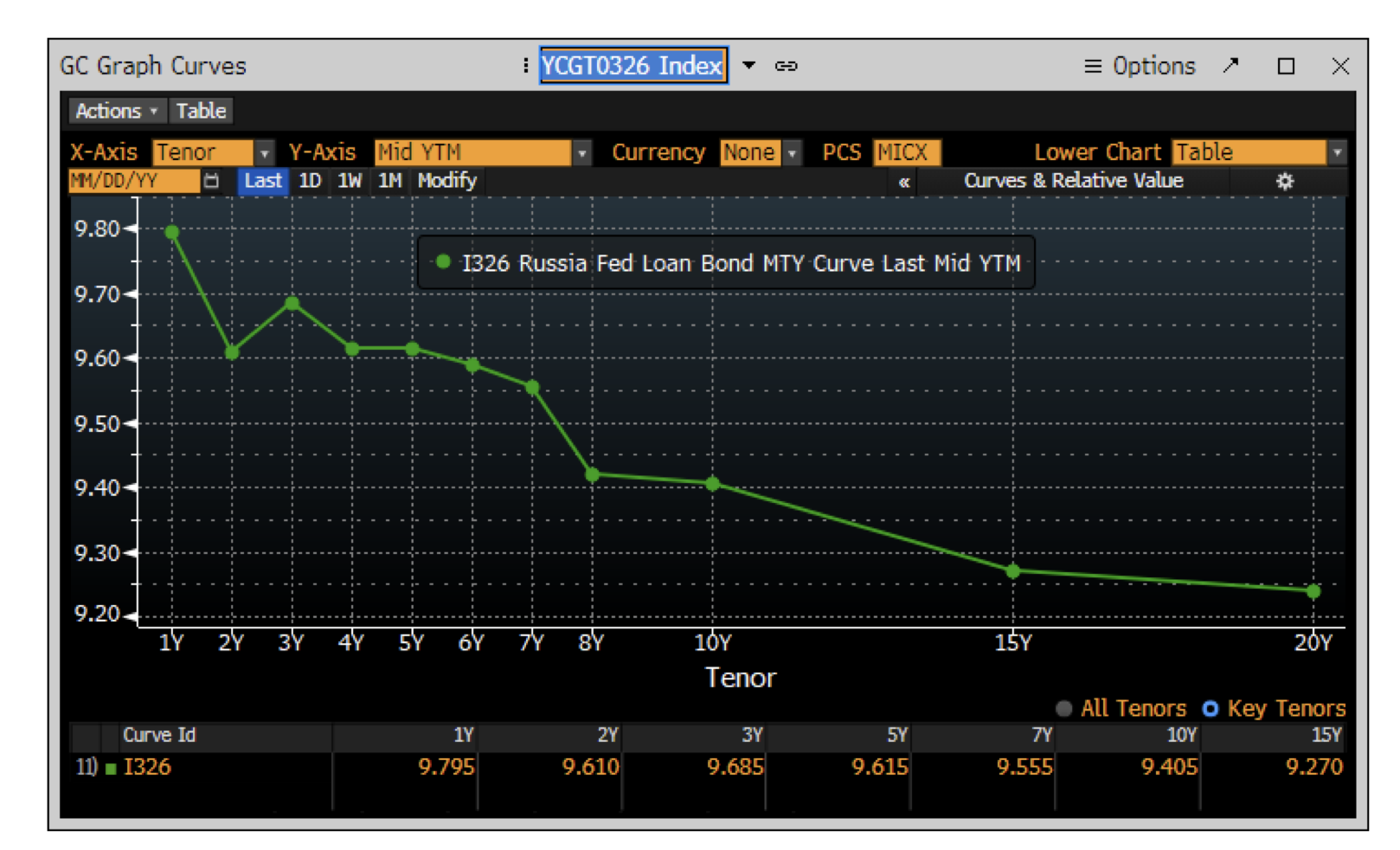

Russia was one of the many emerging markets (EM) that tightened monetary policy last year in response to soaring inflation. But as inflation stabilises or drops back, EM central banks will be able to stop or even reverse interest rate rises. Barring a global risk-off move toward a stronger US dollar, this would be an attractive backdrop for EM debt. Russia is a case in point here: its yield curve (the difference between short and long-term debt) has inverted, which suggests markets think the tightening cycle is close to its peak.

The global economy can often still thrive with emerging markets lagging, but there is one notable exception: China. Though classed as an EM, it has such weight in the global economy that its economic development sifts into the rest of the world. In response to a continued slowdown in growth and a weak housing market, China continued easing policy this week by cutting interest rates. Onshore and offshore Chinese equities welcomed this move, and promptly outperformed their Western market peers. Indeed, on a price-to-earnings basis, Chinese equities are trading at a steep discount compared to developed markets.

We suspect Western economies are living through the last bout of COVID-induced distortions. If so, the coming quarters will reveal the genuine underlying pace of growth, and hence companies’ long-term earnings potential. The transition phase will bring both pros and cons for markets. On the plus side, fewer virus restrictions will be a boon for those industries that have struggled in the last two years, particularly services, while input cost pressures should subside. On the other hand, real disposable incomes will be hit with higher prices, while monetary and fiscal tightening will add to the squeeze on businesses and consumers.

As the growth cycle matures, markets will adjust toward higher real interest rates, not just in the US but across most major economies. This is all part of the road back to normal, but after so long on emergency support, there will inevitably be bumps along the way.

We can see as much in the cyclical rotation of assets. Sectors that are highly sensitive to real interest rates did very well through the pandemic, but now those same sectors are under pressure. Long duration investments like technology and consumer discretionary companies have underperformed this year, as stretched valuations limit their growth potential. As economies open up, sectors will converge towards their new position within the ecosystem.

We have every reason to think this new ecosystem will be a healthy one – with many opportunities for growth. Changing conditions are likely to bring more volatility, as we have plainly seen so far this year. But volatility along the way does not mean we will end up in a worse place. It could be a bumpy road, but the destination should still be a good one.

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.