Market Update: Markets heading for holidays

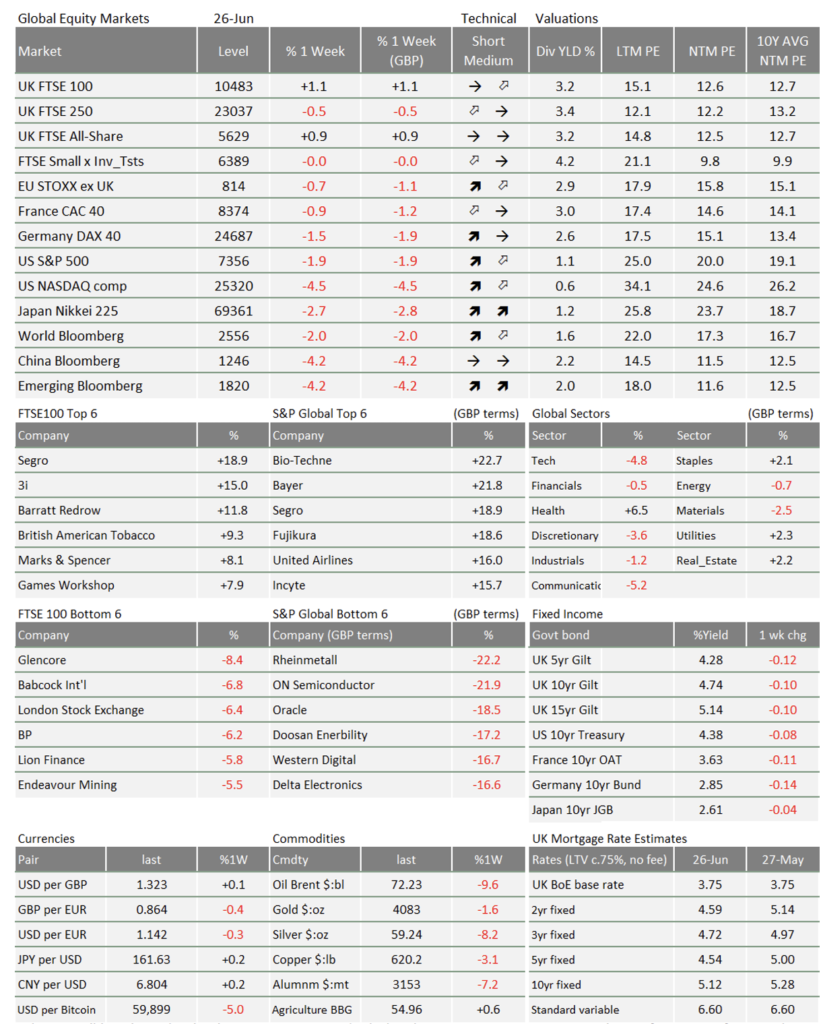

Stock markets, predictably, wobbled this week. Investors have seen great returns this quarter despite intense global risks, so now many institutional investment managers must rebalance their asset weightings back to target – by selling the assets that have done well. Rebalancing selling pressures are temporary, but the extent of this sell-off suggests that markets might be less fun in the second half of the year. Drier liquidity conditions and market jitters could mean stable but slightly less spectacular returns ahead.

UK markets look serene about Andy Burnham’s expected entry to Downing Street. While most regional stock indices fell this week, UK equities rose and government bond (“Gilt”) yields have declined more than others. We cover Burnham’s potential economic policies in a separate article, but the short version is that they are unlikely to affect globally diversified investment portfolios particularly much.

Currently, lower oil means lower liquidity

Despite pessimistic news coverage, ships are traversing the Strait of Hormuz, and oil prices are back to where they were before the war began in late February. Government bond yields have risen in the last few months on heightened energy inflation expectations, but they meaningfully dropped too this week. You would think the good news would push equities up further. That does not appear to be the case.

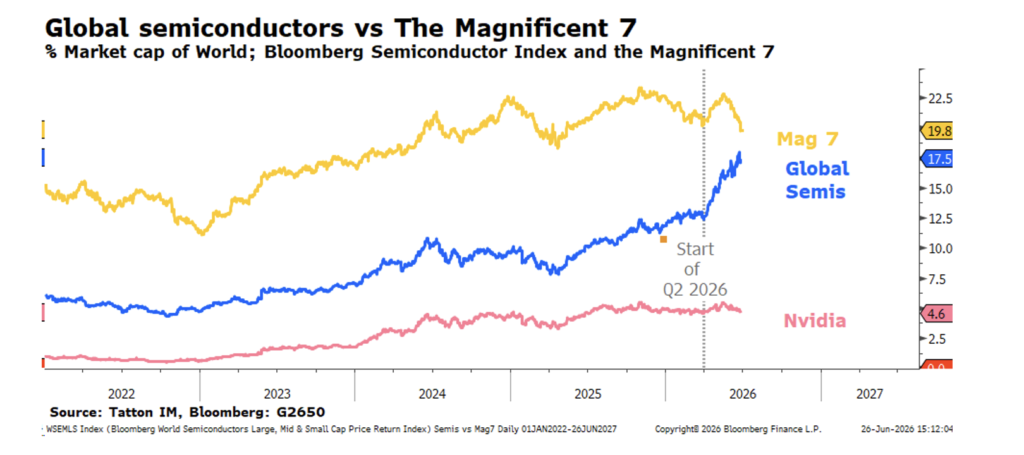

Not even US memory chip manufacturer Micron’s incredible earnings results were enough to spur a broader rally. The chipmaker’s quarterly profits were 15 times higher (!) than the same period last year. That briefly buoyed AI stocks, but the US tech-heavy Nasdaq index still ends the week lower. Investors look wary after so many months of gains.

The chart below shows the remarkable rise in global semiconductor stocks through this second quarter. The ‘Magnificent Seven’ initially kept pace (other than Nvidia) but have now handed over the torch to chip manufacturers. Given this phenomenal performance, it is no surprise that quarter-end rebalancing chipped away at their share prices.

Counterintuitively, falling oil prices could themselves be depressing market sentiment slightly. After the surge of speculation in energy supply contracts over the last few months, oil futures are now among the most traded financial instruments in the world, in value terms. Falling oil prices therefore mean financial losses for speculators. Holders of energy contracts have to sell other assets to cover their positions, which could be tightening overall market liquidity over and above the aforementioned quarter-end rebalancing.

Liquidity conditions are seemingly dominating short-term market moves even more than economic factors right now. That does not tell you much about the long or even medium-term, though. Long-term asset prices are driven by economic fundamentals. For those, cheaper oil is definitely a good thing.

Dollar rises at renminbi’s expense

The dollar’s recent strength could be another problem for global liquidity (it tightens financing conditions for non-US companies). The world reserve currency is now breaking out of the weak range it has been in for 18 months.

The dollar even gained on China’s renminbi – having consistently slid against the renminbi in those 18 months. China’s woes continue; last week that hurt its stock market and this week it hurt the currency.

We have argued before that a strong renminbi is a policy choice – putting international reputation above competitive exports. Contrary to that view, Absolute Strategy Research (ASR) suggested this week that renminbi strength might be a knock-on effect of Beijing’s move to settle international commodity payments in its own currency. As Chinese importers no longer need dollars to buy commodities, Chinese commercial banks have a surplus (from finished goods being sold for dollars), pushing down the dollar relative to renminbi. ASR suggest Beijing might reverse the dollar surplus, weakening the renminbi.

We suspect that might indeed happen even if the strong currency was deliberate. Regardless of how the renminbi strengthened, its strength has clearly hampered Chinese financial conditions. Beijing has achieved what it wanted from a strong renminbi (contracts are settled in renminbi because it is strong), so it now has an incentive to weaken it.

Back to bubble talk

Big tech (Mag7) underperformance has resurfaced the AI “bubble-burst” talk. Allianz’s CEO called SpaceX’s huge bond sale a bubble sign, and Micron boasted about escaping its historic classification as a cyclical stock, thanks to billions in long-term contracts. The more people tell you it will go up forever, the more you wonder if we are at the peak.

AI stocks – and global stocks generally – have been rallying since late 2022, so nerves are understandable. Historically, such runs usually led to overextended equity valuations.

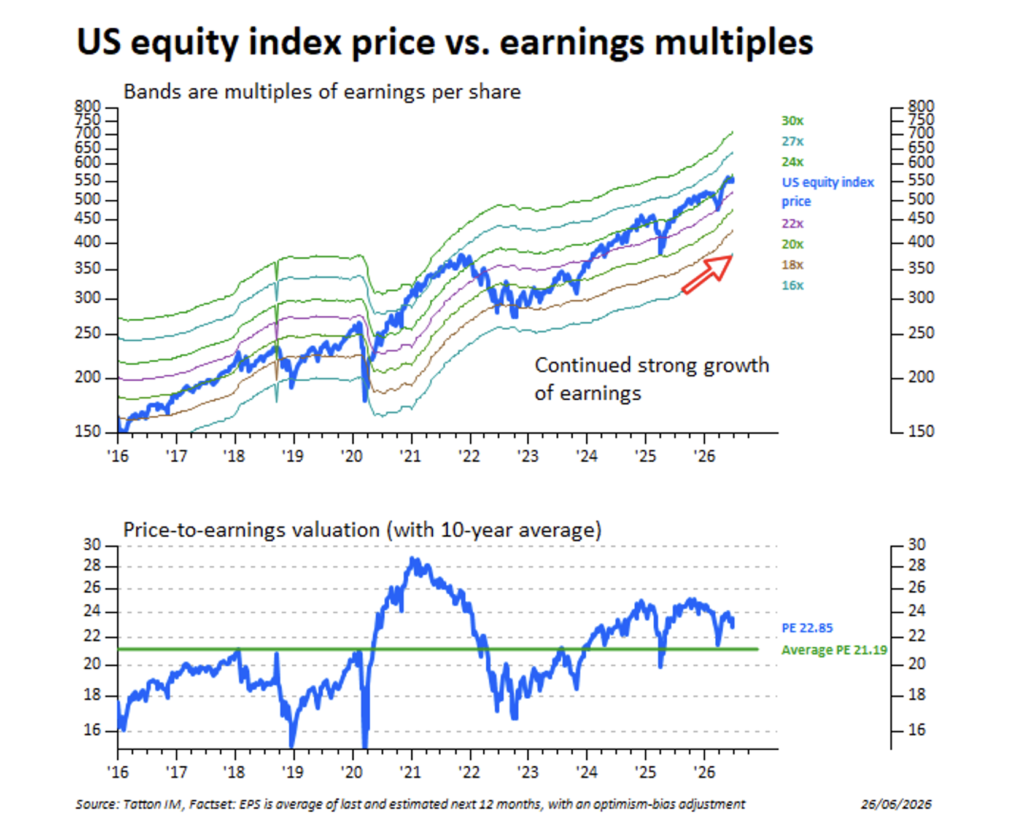

However, in the classic price-to-earnings valuation sense, big tech is probably not a bubble. In fact, equity valuations have fallen in 2026, because tech profits have been growing even faster than share prices (see next page’s chart).

You could, of course, argue that the earnings themselves look like a bubble. One might look at the falling prices of AI compute (possibly due to the proliferation of cheap Chinese AI models) and say that the good times cannot last for the likes of Micron.

Unhelpfully, Apple and Microsoft announced this week that higher chip prices will be passed on to consumers. This is to shore up deteriorating margins, but it risks hurting demand. Meanwhile, the US administration is interfering again in the release of frontier AI models. Reportedly, OpenAI has been asked to slow new releases just as it tries to compete more aggressively with Anthropic.

However, AI demand is clearly growing rapidly too. Chipmakers will obviously not grow like this forever. But business confidence numbers – particularly in manufacturing – suggest they can keep growing a while longer.

It is no surprise that the party is still going, given the vast sums raised to build datacentres. As argued before, relative commodity pricing (rallying copper, stagnating iron) suggests companies are stockpiling essential materials but not actually building yet. The implication is that there is even more economic growth to come.

After periods of strong stock market growth, it is natural to be sceptical of further gains. What we do in such periods is to look at the economic data and assess whether the underlying fundamentals justify or contradict the market moves. Judging by those, you would not want to get off this bus for a while yet.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.