Market Update: IPOmania triggers market self-doubt

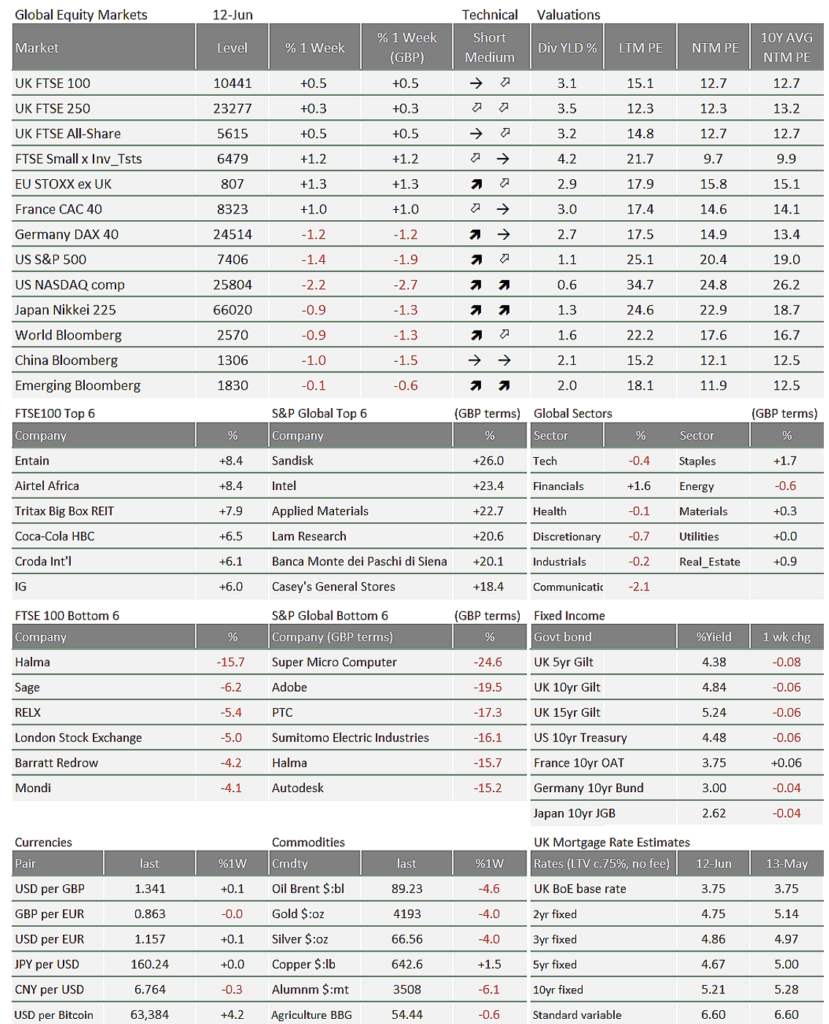

Equities started last week poorly but ended strong – a reversal of the week before. Trading liquidity was initially tight as investors contemplated a glut of newly issued shares, most notably today’s SpaceX IPO, but liquidity returned on Friday amid good news stories. Recent volatility has largely been in tech sectors. That is why UK and European markets were steady compared to the tech-heavy US, despite the European Central Bank (ECB) raising interest rates.

The underlying themes are the same as they have been for months, even if they are evolving. Most players in the Middle East conflict want peace and seem to be making progress. In the UK, the Prime Minister’s erstwhile allies are fading. UK bond (gilt) traders will be focussed on the Makerfield by-election this week, but global investors will care more about interest rates and Kevin Warsh’s first meeting as Federal Reserve Chair.

Mixed weather for a SpaceX launch?

The $75 billion of fresh SpaceX shares have reportedly met $350 billion in demand. Having set the initial price at $135 per share, secondary trading is indicated to open at $165 – though exchanges have delayed trading to find the opening balance.

Many wondered if it was bad timing for the biggest IPO in history. AI optimism has backed off from its peak and trading liquidity has declined. Alphabet (Google’s owner) just placed $85bn in fresh equity, of which $45bn have already been filled, absorbing almost as much of the available capital as the SpaceX IPO. Bitcoin – which has mirrored market liquidity and retail investor sentiment – failed to meaningfully recover recent falls. Having said that, tight liquidity and softer sentiment are partly because of the equity issuance glut.

At the time of writing, SpaceX’s floated shares are in strong demand. Funds tracking the Nasdaq will soon be forced to buy them, so the more speculative investors will look to lock in purchases now. But a true appraisal of the blockbuster IPO will have to wait a week at least. Lockup expiries (insiders being gradually allowed to sell their shares) could be more important than the debut day itself.

Those worried or excited about their portfolios’ potential SpaceX exposure should note that it will not be included in the S&P 500 for a year and only make up a maximum 0.5% of the Nasdaq and MSCI USA, even if the IPO is a resounding success. In other words: negligible in terms of a globally diversified multi-asset portfolio like Tatton’s.

Market sentiment has been weak recently. Many are once again worried about a dotcom-style bubble. Those fears are understandable, but there is a key difference between the AI boom and the dotcom bubble in 2000: right now, it is the biggest, most profitable companies demanding investment capital. Even SpaceX’s revenue is significantly larger than many of the 2000s companies that listed and quickly saw their share prices collapse. Moreover, leveraging those profits for investment in new technology makes it more likely that the current big tech winners will keep winning.

Thank China for (relatively) cheaper oil

China’s weak economy has gone under the radar – partly because of other global drama and partly because we have become used to it. Interestingly, China’s inflation expectations have moved up after years of deflation, thanks to higher oil prices and government mandates against price wars. But inflation has not stopped Chinese government bond yields falling – signalling persistently weak growth.

For the global economy, the most notable impact is China’s weak oil demand. Chinese oil imports have fallen off a cliff since the US and Israel launched their war on Iran. Indeed, that is one of the reasons oil prices have not spiked to the predicted $150-$200 per barrel level.

China’s low import figures are down to a range of factors (reserves, alternative sources, changing demand patterns) but the key question for the world economy is: what happens if that changes?

There are already signs of stress in global energy. European natural gas storage is currently at the low end of its seasonal range, and short-term gas futures contracts are getting more expensive. The shape of futures markets suggests this is a short-term problem but – like so many things – that depends on resolution in the Middle East.

Fresh narratives to come this week

After attacks by the US and Iran, it was difficult to see a resolution. Oil prices fell after Iran leaked a 14-point proposal following a meeting with the Qataris, but they rose once Trump said “The terms that Iran leaked out to the Fake News have NOTHING to do with the terms that were agreed to, in writing…”. That came only hours after he confidently announced for the 40th time (!) that a deal was “very, very close – probably the weekend”.

At least we know there was some sort of agreement. Both sides have a clear incentive: energy inflation is damaging US affordability, Trump’s biggest political weakness, while the Iranian regime needs money and resources to maintain its power. But that has been true throughout the over 100-day war. Both sides are factional and unpredictable, making an agreement difficult. There is always somebody on each side destabilising any potential outcome.

‘Factional and unpredictable’ could equally apply to Westminster. We are still waiting for Andy Burnham’s potential entry to Parliament this Thursday. In the meantime, Defence Secretary John Healey just resigned over what he says are insufficient resources for the UK’s Defence Investment Plan. The plan has been lingering for a while and there are suggestions that it could force the government to issue a new ‘War Bond’. That does not bode well for gilts, but regardless, yields barely moved last week. Like everyone, gilt traders are waiting for Makerfield.

The ECB’s clearly signposted rate rise did not move bonds or equities either. Markets are focussed on a much less predictable central bank: the Kevin Warsh-led Federal Reserve. Next week’s Fed meeting will be Warsh’s first, and we have written before about how his low-rates, light-balance-sheet approach could be a game changer for markets. If nothing else, we should at least have something else to talk about next week.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.