Market Update September: Taking a step back to look forward.

Stock markets have stabilised and started trading sideways, in a sign of healthy consolidation following their extraordinary recovery rally since late March. Notably, the darlings of the recovery, namely US large cap tech and growth stocks, are no longer the leaders. This bodes well for a gradual sentiment shift among investors. Capital is no longer piling into the ‘fear trade’ that saw investors flocking towards apparently virus-proof businesses of our new virtual, digital, stay-at- home existence. Instead, investors are buying into the return-to-normality trade of the more physical parts of the economy, like manufacturing.

Stock markets have stabilised and started trading sideways, in a sign of healthy consolidation following their extraordinary recovery rally since late March. Notably, the darlings of the recovery, namely US large cap tech and growth stocks, are no longer the leaders. This bodes well for a gradual sentiment shift among investors. Capital is no longer piling into the ‘fear trade’ that saw investors flocking towards apparently virus-proof businesses of our new virtual, digital, stay-at- home existence. Instead, investors are buying into the return-to-normality trade of the more physical parts of the economy, like manufacturing.

Similarly, the resurface of political anxiety over Britain’s post-Brexit trading conditions with the European Union (EU) has calmed over the week. For one, reports have emerged of negotiations progressing on one of the two remaining Brexit trade deal sticking points – fisheries. Full sovereignty over state aid decisions, the other make or break issue, also appears far less unsurmountable, since it transpired that with the previous week’s free trade agreement with Japan, the UK government has already agreed to more stringent constraints on state aid than are currently the bone of contention with the EU.

In the US, the political establishment on both sides made it clear they would take a dim view to any future trade negotiations should the UK undermine the Northern Irish Good Friday agreement for the sake of Brexit. Therefore, it seems increasingly unlikely that the government’s ‘nuclear’ negotiation option of breaking an international treaty has much life left in it.

Unfortunately, and despite these positive developments, the mood of UK private investors may well have become quite clouded again, due to the reintroduction of wide-ranging coronavirus constraints and concerns over what this may mean for the economy and stock markets. Have heavy dark clouds re-appeared on the horizon, then?

It is worth taking a step back to reflect, before making predictions based on our most recent experience (even if that is a very human approach). Just as we all underestimated what was ahead of us in March, we may now be overestimating what the second wave of infections could bring – and for how long. The facts tell us that the fear of what might happen drove the Covid containment measures, which then caused the economic slump. We would argue that if the public health impact across Europe and the UK back in March had been at as low a level (relative to the infection count) as it is at the moment, then much less severe containment actions would have been taken. The reason we are seeing the government reimpose soft lockdowns across large parts of the UK is a resurgence of the fear that severe cases and fatalities will return to April’s levels.

While such action seems rational (even if still quite damaging to the economic recovery), the general levels of justified fear are likely to decline with every week that passes by without a repeat of April’s public health pressures. Importantly, every week also takes us closer towards the formal licensing of COVID-19 vaccines. Here, reports that the German-US joint venture between BioNTech and Pfizer may be reaching approval and first roll-out by the end of October were the highlight of the week. This is considerably earlier than experts had dared to project, and provides a strong perspective for an alternative means of protecting those truly vulnerable to Covid, compared to restricting the lives of everyone. The UK’s own Oxford University/AstraZeneca vaccine trial is also back on track after the health issue with one of its test patients was confirmed as an undiagnosed previous condition and therefore unrelated to the test vaccine.

The BioNTech/Pfizer project alone is projecting to have produced 100 million doses by the end of the year and we know that AstraZeneca is also already producing their vaccine at volume under the assumption (and business risk) that it will gain approval. This should mean that, starting from November, fears for those most at risk from COVID-19 should reduce materially, given their numbers are small compared to the entire population.

Based on the above, we suspect the near-term impact of the second wave may be far less than what it currently seems. If people across Europe continue to be able to keep the public heath impact as low as it has been in Spain and France, and the arrival of a vaccine remains on course, the fear currently driving the public response could dissipate quite rapidly.

Given the entirely new set of threats that 2020 has presented to us all, it is very understandable that we resort to guidance from our most recent experience. However, in this instance, this may not be the best advice for investors. For example, a number of virus-related uncertainties are beginning to approach the end of their natural life. With their expiry, a significant volume of pent- up activity could add suddenly to every aspect of the economy, as consumers behave similarly ‘de-mob happy’ as they did following past periods of wartime constraints. While much of the normalisation expectation has already been priced into financial assets since March, we can see from China’s recent economic development that there is considerably more economic upside from a true Covid recovery than may be priced in presently. This is particularly true for all those sectors and companies shunned as the losers of the coronavirus crisis, and therefore present promising bounce-back potential. For the coming weeks, we at Vision Wealth will therefore be focusing on realigning our investors’ portfolios to the sector rotation dynamics that have historically followed severe recessionary periods. Beyond that, we will once again look at focusing on the previous uncertainties for investors. The US election and our own Brexit arrangements may well become the more important dynamics for us to assess in the last quarter of 2020. Fingers crossed.

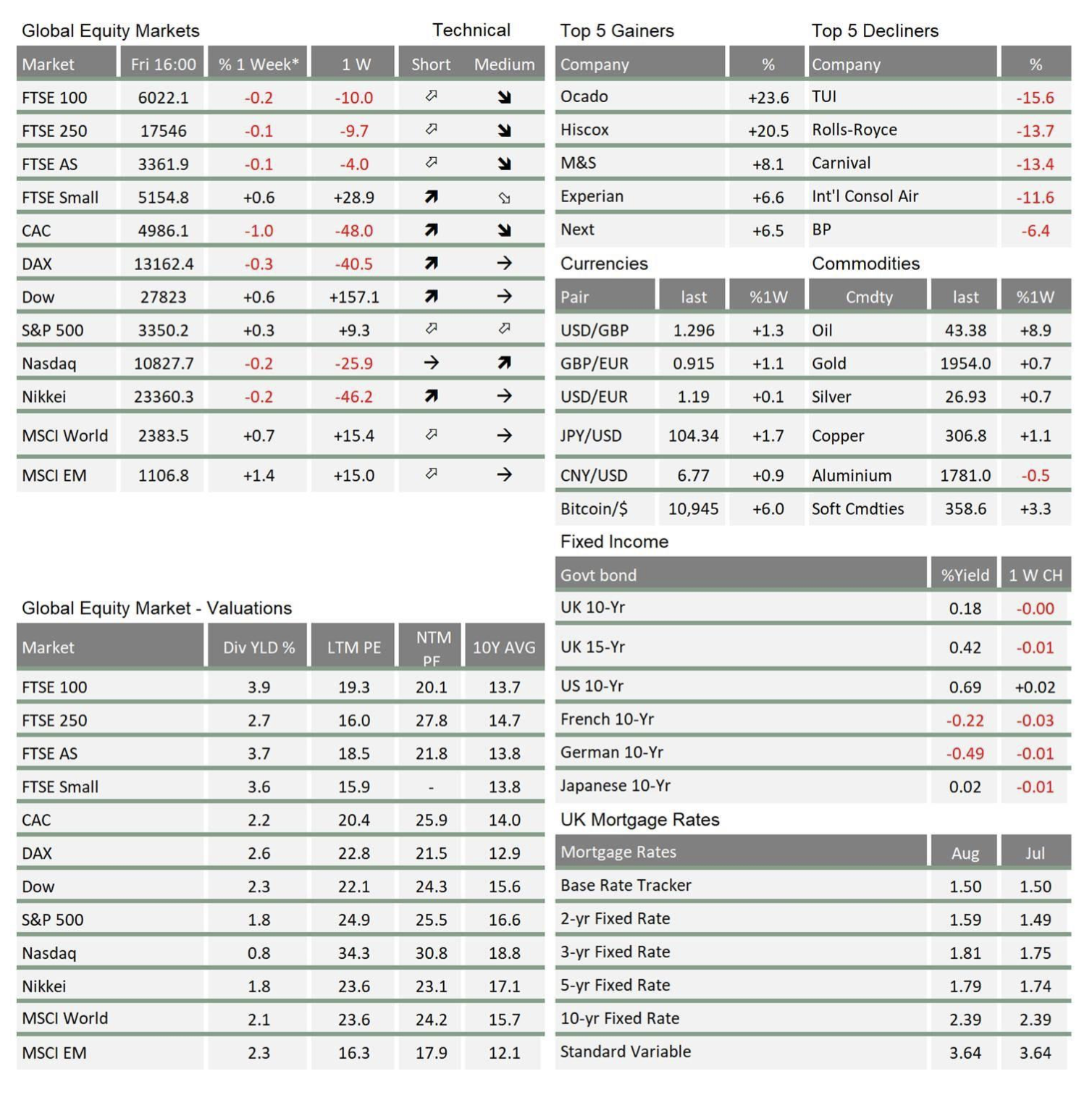

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.