Market Update: FOMOOP – Fear of missing out on peace

As we were writing, Iran declared the Strait of Hormuz “completely open” and markets rose sharply. This time, bond yields fell back too. Even before that announcement, equity markets had, more or less, decided that the war is over – thanks to US-Iran talks and the Israel-Lebanon ceasefire. US stocks rose above their late February peak for the first time since the conflict began. Investors are now focussing more on strong earnings growth than geopolitical risks.

Understandably, many remain sceptical. It is unclear how long the Strait will stay open and how quickly shipping traffic can return. Damage has already been done to the world economy and the consequences will not be removed instantaneously.

Not yet out of the woods

Equity traders are clearly optimistic that peace will hold, but oil markets were a little less so. The one-year futures contract for Brent crude is above $75 per barrel (even after the announcement on Friday afternoon), well below the current price of just below $90pb, but significantly higher than $60pb, the level at the start of the year. That implies both a longer-term inflation impact, and perhaps a bigger hit to growth, than stock markets are pricing in. Already, we are seeing knock-on effects from higher energy – as we discuss in a separate article on food prices.

Even $75pb oil, a year from now, assumes de-escalation continues in the Middle East. That assumption could well be right, but we have seen false dawns before. Before the latest breakthrough, the US was also blocking ships out of the Persian Gulf – putting it in direct opposition to Chinese interests. Neither the US nor China have the appetite for direct conflict, which may have contributed to US-Iran negotiations. If ceasefire talks stall or go backwards from here, though, the greater risk of US-China tensions could re-emerge.

If the optimistic view that the war is all but over is right, what comes next for the Trump administration? A politically bruising war might prompt the president to avoid rocking the boat for a while, but that is not his style. Adventures beyond US borders are becoming less popular with voters, so there is a good chance the administration’s focus will turn back to the domestic agenda.

Already, the banks’ deregulation (centred around freeing up capital) has helped increase lending. The next stage of that deregulation is going quickly through the consultation process, and implementation is likely in the second half of this year.

Kevin Warsh, Trump’s pick for Federal Reserve chair, will soon take the reins at the central bank. With Warsh in place, and with the midterm elections approaching, this might be a good time for Trump to push other deregulation even harder. Markets may well like that.

Positivity is about liquidity

Stock markets are positive because the worst-case scenario has become less likely, allowing investors to focus on the upside. That might seem overly optimistic, but investors have become a little numb to political shocks in recent years. Last year’s “Liberation Day” tariffs proved that getting too negative carries a serious risk of missing out.

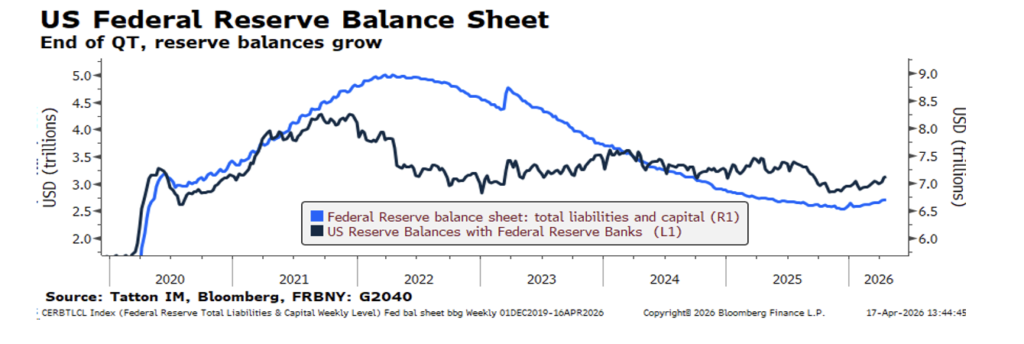

The good mood is helped by improving liquidity conditions this year. Liquidity was tight into the end of 2025, as the Fed tightened its provision and the US government shutdown sapped money from the system. Those conditions made markets react more negatively than you might have otherwise expected. If the Iran war had happened a few months ago, the selloff probably would have been worse. Since the start of 2026, though, the Fed has shifted from net bond sales to net purchases, easing liquidity conditions (the upwards tilt of the blue line in 2026 in the graph below).

When war broke out, leveraged traders (such as hedge funds) were forced to sell stocks. But fully capitalised long-term investors, for the most part, did not. Again, this was helped by improving liquidity conditions and past experience of overreacting to Liberation Day tariffs. Liquidity is now getting even better. This week, the dollar dropped and short-term bond yields fell. It should not be a surprise that market momentum shifted after central banks backed away from their hawkish rhetoric (preferring higher interest rates) in late March.

The green shoots are growing

Investors have plenty of decent data to focus on. The US first quarter earnings season started this week with some reasonably good results from the big banks (as discussed in a separate article). Earnings reports showed that US consumers are still spending, despite discontent about higher prices at the pump. This is helped by a stable labour market – contrary to headlines about tech layoffs. As many suspected, the US economy as a whole looks relatively insulated from higher energy prices. Higher consumer prices are merely resulting in a flow of money to US oil producers, rather than a flow abroad, like in Europe and Asia.

UK growth also came in higher than expected, with a 0.5% month-on-month expansion in February, versus expectations of 0.1%. The data is from before the oil shock, so we should not get ahead of ourselves. But it shows the UK was in a decent place heading into this latest crisis, at least.

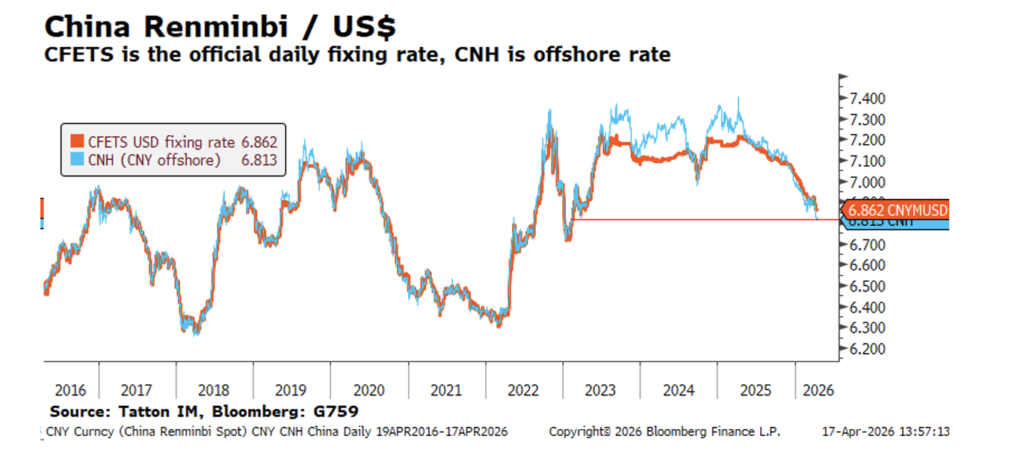

Given strong US growth, it is slightly odd that the dollar fell back this week. Strangely enough, the strongest currency has been China’s renminbi – climbing to a three-year high against the dollar – despite weak domestic growth and a sluggish equity market. The Chinese government has been guiding its currency stronger for a while now, and the Iran war has not knocked that trend.

The euro also gained last week. The prospect of lower energy prices undoubtedly played a big part, but we suspect that some of the gain was down to populist Viktor Orbán’s election loss in Hungary. Orbán has seriously stifled European cohesion over the last decade, often to the detriment of the wider European economy. Politics might get a little less disruptive on the continent from now on. Markets think the same is true for the world.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.