Market Update December: Christmas tidings of comfort, if not joy

Looking back, the year has exceeded some expectations and underdelivered on others. In terms of our expectations for the economic recovery and capital market performance, 2021 has been better for investors than we dared to hope and forecast at this time last year. On the other hand, I am surely not alone in having hoped the vaccination drives that began one year ago would have ensured further progress in putting the pandemic behind us than where we are now.

The Omicron wave feels like a real setback to the trajectory towards normalisation of our everyday lives. Christmas plans are once again being altered radically, disappointing those expecting a return to their pre-pandemic travel habits. This is not just bad news in respect of our festive activities, but will undoubtedly dent seasonal revenues for retailers and the hospitality sectors.

Yet, over this past week, the Christmas messages we received from central banks was distinctly one of continued normalisation, or rather phasing out of the extraordinary monetary support put in place to see the economy through the worst of the pandemic’s economic shutdowns. This tells us that their economists see the current Omicron episode as short-lived and unlikely to have a material impact on the general upwards direction economies around the world have taken since the beginning of the year.

Benign market moves suggested that central bankers had once again successfully managed market expectation and that most investors similarly see the Omicron episode as likely to be short- lived. However, politicians cannot afford to take a similarly optimistic ‘wait and see’ position, and will have to assume the worst until science informs them of the actual impact on public health of this latest COVID mutation. Until then, prudence and politicians’ natural self-interests dictate making every attempt to reduce transmission, even if it impacts economic activity in the short term.

The hit to consumer and business confidence will be the key follow through for next year. If this strain of the virus is more contagious and less dangerous for most individuals (for whatever reason), it will be important for businesses that they can see the politicians acknowledging the evolution, and adapting accordingly.

The major central banks told us about their expectations for growth in this week’s meetings, and collectively see a reasonably strong growth path being maintained through 2022 and into 2023. This has enabled almost all of them to shift policy away from the current ultra-easiness. Perhaps the most uplifting aspect was that all central bank commentators considered the Omicron outbreak a bump, rather than a barrier. We discuss in more detail the Federal Reserve Open Market Committee’s decisions below (where we also discuss how they may not always be as impressively successful as this week). However, the one central bank that is having a bit of an issue with aspects of its credibility is… the Bank of England (BoE).

The decision by the Monetary policy Committee (MPC) to raise rates on Thursday was a surprise (just as surprising as the decision to not raise rates in November). Yes, the increase was only 15 basis points (bps), taking the base rate from 0.1% to 0.25%, and we should take heart that the MPC too sees the Omicron episode as a temporary influence. One could point out that the BoE’s bond-buying quantitative easing operation ended only very recently and it needed to see if there was any impact before taking any further policy steps. Yet the BoE’s briefing of the underlying situation for December differed very little from that in November and, subsequently, Governor Andrew Bailey seemed to indicate that the path to higher rates was still in the future. In the words of Allan Monks of JP Morgan: “It has been hard to read the BoE’s reaction function of late, and while some members responded to the confusion surrounding the November meeting by saying less rather than more, that only added, in our view, to the difficulty in understanding what they were thinking in the run-up to this meeting… 2021 will not go down as the BoE’s finest for clarity ofcommunications, but at least 2022 brings hope”.

Much of the uncertainty seems to stem from whether inflation has the potential to become a bigger issue that central forecasts have indicated. So, does the UK have a more problematic inflation outlook than others? Are we on a path to much higher rates? Here’s Allan Monks of JPM again: “CPI is on track to climb to a peak of around 5.7% next April and remain close to 3% into 2023 [if there were to be no tightening]. The BoE’s forecasting model imply that 20bps of tightening would be necessary to reduce medium term inflation by 0.1%. This would imply (about) 120bps of tightening would be necessary to return inflation to target. While [JPM’s] forecast does show this level being reached by end-2023, surprises could force the BoE to act faster.”

Right now, however, none of the UK markets are behaving as if there is a big problem brewing. Sterling is stable and the equity market has kept up. If anything, it may have started to outperform.

Another thought we take away from this week’s juxtaposition of central bank direction compared to public health policy is that monetary policymakers have seemingly – and with a certain amount of courage – moved towards a post-pandemic mindset. Meanwhile, politicians have continued to resort to very similar restriction of movement and crowd management policies, just as they have with every previous COVID wave and mutation. Eventually, politicians too will have to decide whether, on balance, it is still constructive to shut down vast parts of societal activities with every new variant. The question will be at what level of public health impact we have reached the point when the virulence of the latest COVID mutation has become comparable to what we have always lived with, and accepted as the natural impact of what we know as seasonal flu.

Since we started the year with Brexit, it may be appropriate to close it also with a thought on Brexit. The outcome of the North Shropshire by-election provided a surprise and unwelcome ‘Christmas gift’ for the Johnson government, but perhaps also marked a shift in priorities that were not mentioned in last night’s victory speeches. The constituents of a previously staunchly Brexit- supporting constituency, perhaps inadvertently, voted for the only party committed to seeking the UK’s eventual return to Europe – an ironic way to give Boris Johnson a bloody nose. Meanwhile, Jersey issued French trawlers with more fishing licenses and the UK’s Northern Ireland Protocol negotiating team conceded that the European Court of Justice may be the arbiter in matters which are considered under European law. Have we moved beyond the dogmatic Brexit and are about to see a more pragmatic way forward? The UK’s economy would certainly be grateful, and provide a good basis for a solid return on such ‘investment’.

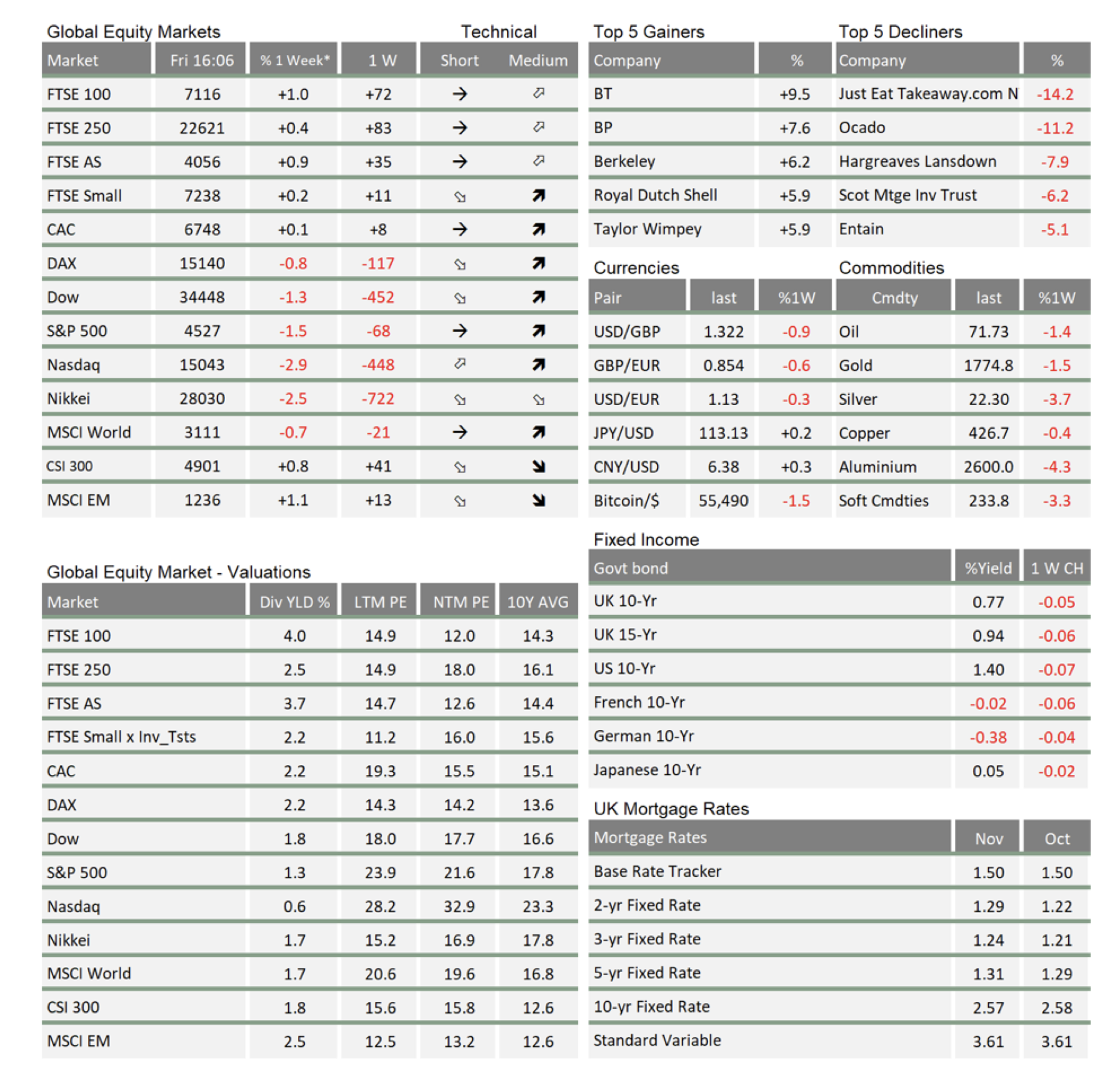

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.