Market Update: Calmer markets?

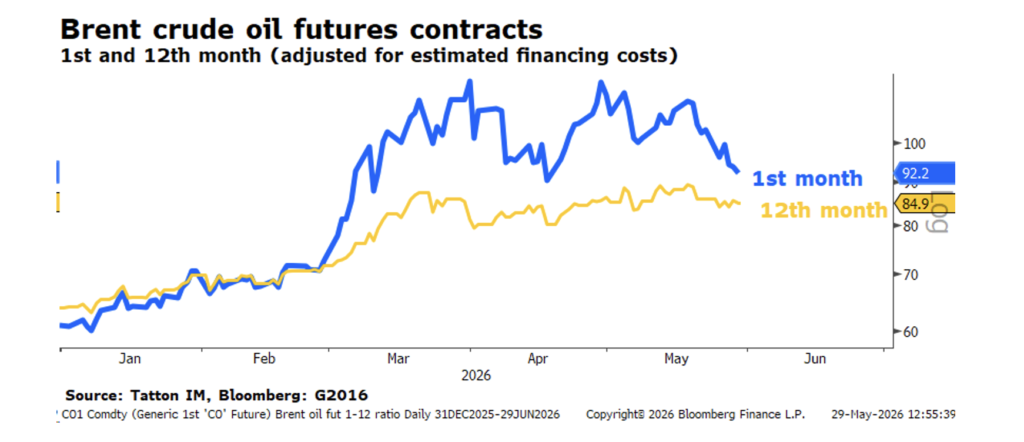

Global stocks pushed higher last week, led yet again by global tech stocks. Semiconductor chip makers were especially strong. On Thursday, Axios reported that US and Iranian officials had agreed a 60-day ceasefire extension, during which they would negotiate a resolution to Iran’s nuclear program. The ongoing talks have calmed nerves and substantially lowered oil prices – to below $90pb at the time of writing, down from $110pb at the start of last week.

Government bond yields dropped back too, easing a key source of recent market tension. Small and mid-cap companies have had a period of underperformance given the increase in financing costs so the decent fall in bond yields has helped them resume upward momentum.

In the end, May turned out to be another strong month for global stocks with falling price volatility, both in implied and realised terms. More surprisingly, bond yields ended roughly where they started in the US and lower in the UK and Europe. Contrary to the chaos still playing out in the headlines, markets look sanguine.

Time is more on our side than we thought

A US-Iran deal has been supposedly “imminent” for about seven weeks now and the ceasefire memorandum still needs final sign-off from Donald Trump, so we should not hold our breaths. We at least get the impression that Trump wants the war wrapped up before the US midterm elections in November, and China is reportedly pressuring its Iranian ally to accept the proposal. In any case, lower oil prices help relieve near-term inflation.

Even if the Strait of Hormuz stays closed, the global energy market is clearly more flexible than it seemed a few months ago. The Middle Eastern crude deficit is ameliorated by a mix of production increases elsewhere, strategic reserve releases, the lifting of Russian sanctions and – most importantly – a reduction in oil demand. The warmer weather helps with that, as does the fall in Chinese consumption.

We said before that time was not on our side in this war. The surprising thing in May was how western countries have been able to muddle through the oil shock without it feeling too much like a crisis, even if other regions are feeling real pain (African farmers are unable to plant crops, and Vietnam has a jet fuel shortage). However, while a sense of global crisis has declined, the longer oil contracts have not fallen as much. This indicates that global energy traders think supply will remain tight into the winter.

If it does so, we will certainly feel the effects too (Europe’s gas storage levels are towards the bottom of the seasonal range and are rising less quickly than usual), but for now, the squeeze on markets has not been as bad as many prognosticated.

Sluggish China might want to pressure Iran

China’s oil utilisation has fallen since the war started – suggesting constraints on domestic demand. The government has also effectively tightened financial liquidity; it has asked companies to pay suppliers more quickly (which is related to the “anti-involution” measures). While this improves supplier company cashflows, it means the paying companies are raising debt to cover the cashflow. Thus, there’s been a step up in both local government and corporate bond issuance.

The interesting thing is that the oil shock is coming through stronger as a direct growth problem rather than indirectly through broad inflation. That could be a result of centralised economic policy leaning on economic activity itself, rather than letting markets do it through prices. Chinese bonds are the only ones with lower yields now than at the outbreak of the war – reflecting lower growth potential. That growth hit is now reflected in lower stock prices too. Unless Beijing steps up its economic support yet again, Chinese companies will struggle.

Alternatively, Beijing could lean on Tehran to accept a deal with the US. Rumour has it that Chinese officials are already doing so but, realistically, Xi Jinping has enough leverage over Iran to force its submission if he really needed it. China’s current malaise is not dire enough to pull out that option. In the meantime, they are happy to let the US get bogged down in another costly Middle Eastern war.

Growth isn’t as good as it once looked

Another reason bond yields fell last week was because global growth looked a little worse than we thought at the start of the month (bond yields, in theory, reflect future growth and inflation). US growth for the first quarter disappointed slightly, and personal income figures were notably lower than expected. Retail sales are still holding up, thanks to the ever-resilient US consumer, but that basically means Americans are funding their spending out of savings.

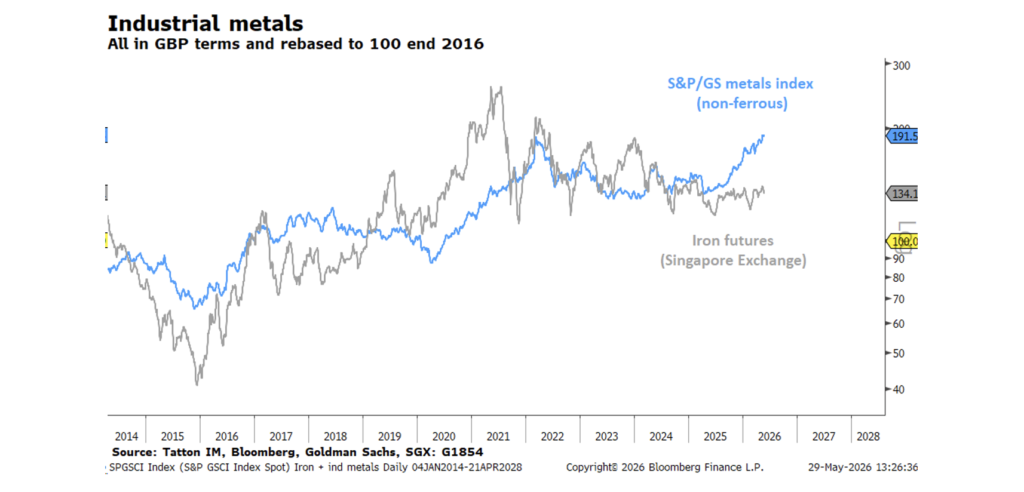

US – and even global – economic growth is driven overwhelmingly by AI infrastructure investment. This is once again pushing up computer chip prices, exemplified by a stunning rise in share prices for semiconductor companies. This is also contributing to a sharp rise in prices for industrial metals (though we discuss a different factor underlying metals in a separate article). Curiously, one industrial metal has not joined the party: iron.

Steel is a crucial building component, so this suggests overall global construction is soft. Residential construction numbers from the US and UK back that up, although Europe is doing better on this front.

The massive funds that AI firms are raising will go into constructing datacentres, but iron prices do not tell us there is currently a big step up in actual work. We suspect that the discrepancy comes from stockpiling critical components like copper and lithium, but the building has yet to start in earnest.

If that is right, the current global growth picture looks a little drearier. On the flipside, it should mean lower inflation and future interest rates, reinforcing the helpful bond yield falls we have seen and that there will be strength in construction in the not-too-distant future. It is a reversal of the narrative we had a few weeks ago – where growth looked a little too resilient, in the face of higher input costs, leading to inflation and bond worries. Instead, we see some slight gloom, but certainly no doom.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.