Market Update: Tornado rather than hurricane

With apologies to Banksy, Christian Adams, Hedgeye, 14 August 2024

Tornado rather than hurricane

The market storm calmed as quickly as it broke and leaves us wondering what we may learn from this storm that never was.

Would ‘Kamalanomics’ mean US fiscal expansion?

Kamala Harris is possibly more likely to be US President than Donald Trump. We look at some aspects of their likely fiscal policies.

The long-term case for Japan

Japan’s stock market suffered the biggest decline in the week before last’s rout. Was it a sign that belief in the Japanese’ companies earnings growth potential is faltering?

Tornado rather than hurricane

After stocks sank in early August, we warned that volatility could ripple on, and the market storm turn into a full-blown hurricane. But last week saw a remarkable dying-down of the volatility, like a whirlwind that passes in an hour: stock markets climbed up all over the world, with no hint of pullback. The rally has been so strong that global stocks are almost exactly where they were at the end of July – before the sharp sell-off. Fears that sparked the midsummer sell-off seem to have faded too, helped by stronger-than-expected US economic data.

Market positivity is of course good to see – and we said all along there was enough to be positive about – but the rapid and sustained turnaround is a little eerie. Our medium-term outlook is still pretty bright, but we think further market mood swings remain likely.

Economy proving the doubters wrong?

The turnaround was undoubtedly helped by some good economic data last week. Here in the UK, GDP grew 0.6% in the three months to June, in line with economist expectations and marking the second consecutive quarter of expansion. It means year-on-year growth in Q2 was the strongest it has been since late 2022, a sign that Britain is finally recovering from its recent difficulties.

Fears about the US economy have faded too. Stocks were buoyed by Thursday’s retail sales report, which showed a month-on-month increase of over 1% in July. This was accompanied by a range of positive consumption signals: lower long-term yields are leading to more mortgage refinancing (indicating confidence about borrowing to spend) and automobile demand is picking up from weak levels. All of these suggest that the American consumer is still proving the doubters wrong.

Recession fears in recent weeks had been focused on unemployment and how it might spiral. The ‘Sahm Rule’ recession indicator that was triggered a few weeks ago, for example, is based on the idea that, when job losses start rapidly increasing, that feeds into weaker demand, weaker sales and hence further job losses. The thought that we might be on that precipice was one of the reasons markets were so jittery.

But if the unemployment spiral was happening, we would see it feeding through into weaker consumption. Consumption would be among the weakest of US economic indicators – but actually it looks like the strongest. The US economy is undoubtedly slowing, but consumers are yet again the force to keep it going. That should only improve when interest rates come down. If the US does pull off a ‘soft landing’ (growth slows enough for rates to come down, without going into outright contraction) we can thank American consumers’ resilience.

Let’s not get ahead of ourselves.

We have every reason to think a soft landing is on the cards. As we noted the week before last, for example, corporate credit has been very stable, compared to the turmoil in equities. That suggests investors are still very willing to lend to companies – the opposite of what you would see if a recession-induced bankruptcy wave was about to hit. But we should not confuse this soft landing with a ‘no landing’ scenario (growth comes back strong without any material slowdown).

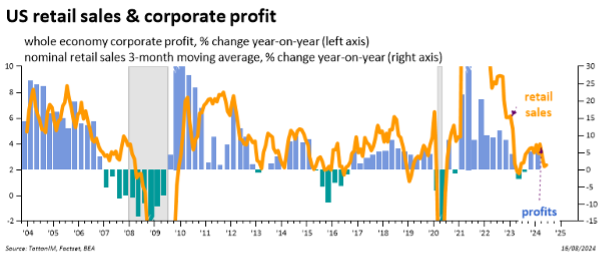

US nominal retail sales were up 1% month-on-month in July, but it was growing from a fairly low base in June. Looking back over six months, retail sales have in aggregate been fairly sluggish. Yet, markets reacted like it was fantastic news. We mentioned the dampened oscillation that tends to follow large market corrections (like a pendulum swinging to a stop) the week before last, but for last week there seems to have been no oscillation at all.

Retail sales and corporate profits tend to change together, as we would intuitively expect. The chart below shows their relative behaviour. The retail sales data is slightly more timely than the whole economy profits data, and it indicates that next quarter’s profit growth is unlikely to be stellar.

Did markets overreact to negative signals before and are course-correcting, or are they overreacting to positive signals now? The answer is probably somewhere in the middle, but it is hard to say for sure yet. The direction of last week’s economic and financial signals was positive and did not add to the week before last’s negative outlook. But data are noisy (particularly short-term data like month-on-month retail sales) and there will inevitably be some releases that look a little worse. The worry is that markets could hyperfocus on those too, bringing another bout of volatility.

We will get a clearer picture after the Jackson Hole conference for central bankers, where Fed chair Powell is set to speak. Markets’ rate expectations moved down sharply after the unemployment numbers, suggesting a 0.5 percentage point cut from the Fed in September and more to follow. Improved signs since then suggest that 0.5 might not be needed, but we will have to wait and see.

Signals from around the world.

The ‘Magnificent Seven’ US tech giants have lost some of their magnificence in recent weeks, and Google’s legal troubles are probably not helping. A US judge ruled last week that the company had illegally monopolised the search engine market, but left the punishment for a separate ruling. Last week, the Department of Justice was reportedly considering a breakup of the company. Needless to say, that would be hugely negative for parent company Alphabet and the entire Mag7 – a sign that their market power might be challenged by regulators.

What happens will inevitably depend on who wins the presidential election. One suspects that a Harris administration would take a harder line than Trump. However, at one level, there is bipartisan commonality in Washington in their dislike of the mega-cap tech firms – but both sides accuse each other of being on the tech firms’ payroll.

Another rare point of agreement is fiscal laxity – to the detriment of the US fiscal outlook. We argue below that Harris might actually be better for fiscal discipline than Trump. Her improved odds recently might therefore be a positive for bond prices.

With some positive data signs last week (following the previous week’s meltdown) there has been talk that the Bank of Japan might be able to continue raising rates after all – possibly in December. This would likely strengthen the yen further, and interestingly the biggest beneficiary could be China. China has kept its own currency stronger than the yen this year (by maintaining a dollar-peg) but that has forced its central bank into tight policy. A stronger yen might allow the bank to loosen its grip, giving the world’s second-largest economy much-needed support.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.