Market Update May: The UK bounces back – or is it just politics?

There has been a great political awakening across the world in recent years. The issues of the day have become visceral divisions. These arguments have had significant impacts on all aspects of our lives, including capital markets.

There has been a great political awakening across the world in recent years. The issues of the day have become visceral divisions. These arguments have had significant impacts on all aspects of our lives, including capital markets.

In the UK, this has been most evidently played out in the great Brexit drama which, aside from its impacts on foreign investment and asset valuations, has been the main driving force behind the value of Sterling.

The government assures us that Brexit is now a settled affair (Jersey fishing rows, Northern Ireland’s trade position and ongoing negotiations about the services sector notwithstanding). Therefore, market commentators have turned their attention towards a familiar political story: devolution and the potential break-up of the Union. This week, Britain headed into elections that might have some meaningful impact in that respect.

First, the Conservative Party by-election victory in former Labour stronghold Hartlepool will have roused Prime Minister Boris Johnson from his despondency. He remains fond of red walls even if his fiancée isn’t. The voters attracted to Johnson seem to see a politician whose failings are small enough to make him human, and they perceive he has delivered on their issues so far.

This morning, Sterling has strengthened back towards its recent highs against both the US Dollar and the Euro. However, probably of greater importance is what would usually be considered the more humdrum local elections. The added spice is that they could set the stage for several independence pushes, from Scotland to Northern Ireland and even Wales.

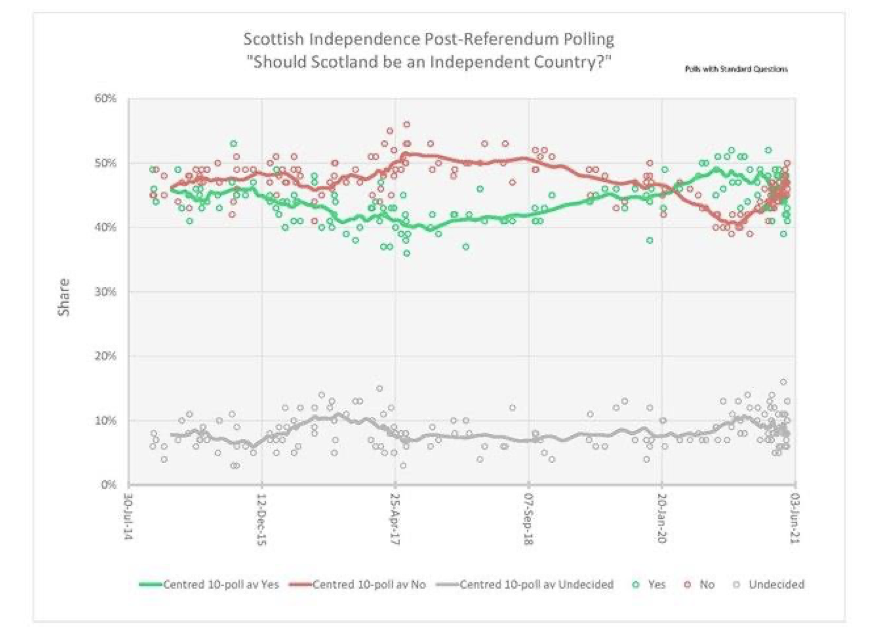

To remind ourselves, it is less than seven years since the last Scottish independence referendum. On 18 September 2014, the people of Scotland decisively answered the question, “Should Scotland be an independent country?” The “No” side won with 2,001,926 (55.3%) versus “Yes” at 1,617,989 (44.7%). The turnout of 84.6% was the UK’s highest since the January 1910 “universal suffrage” general election.

We will not get involved in musing whether the regional outcomes indicate that referenda are more or less likely, let alone whether any referendum might see a vote for independence. We would note, though, that the regional responses to coronavirus through 2020 meant the Scots accorded their regional government a much higher approval rating, which fed into support for independence, as the chart below indicates. However, it also shows that recent dynamics have begun to reverse the position.

While Brexit may be a source of rancour in Scotland and Northern Ireland, it also highlighted the enormous costs which come from separation. The argument that Brexit has changed the nature of the Union – and that the central government should revisit the independence question – is also not likely to carry weight. Perhaps oddly, the Johnson government seems not that fond of “letting the people be heard” just now.

It has been interesting to note how sensitised UK markets have been to the political news-flow over the last few years – something we are still seeing now and should expect to continue. We await patiently the local elections result but, like us, currency markets appear not to be expecting earthshattering changes to the shape of the Union. Indeed, although commentators have made much of this story, in reality Sterling has been rather insensitive to the election news.

In the past, short-term moves in the Sterling exchange rate have been more directly influenced by central bank announcements than British politics. However, it would be hard to discern much influence at the moment here either, despite the Bank of England (BoE) holding its own vote this week.

The BoE’s Monetary Policy Committee (MPC) voted in favour of maintaining interest rates at the current 0.1% level, as well as continuing its £875 billion target for bond purchases. MPC members did opt to reduce the pace of those monthly bond purchases to £3.4 billion a week – down from the current £4.4 billion a week – to be reviewed again at the next MPC meeting in August. But with the overall target still standing, policymakers assured us this would not materially change anything, with which we agree.

Markets shrugging off this news is therefore not much of a surprise. After the deepest recession on record, and with an economic recovery still in its infancy, all expectations are that the BoE will keep interest rates flatlining and liquidity flowing for the foreseeable future. In fact, the biggest surprise was a dissenting vote from the MPC’s outgoing chief economist Andy Haldane, who voted to reduce the asset purchase target by £50 billion, arguing that the growth objectives had been reached and that the current policy response needed to be trimmed. Haldane’s dissent will be his last before leaving the BoE, having made a name for himself as a contrarian. Still, it was enough for former MPC member Danny Blanchflower to call him a “blithering idiot” on Twitter. Who said monetary policy was boring?

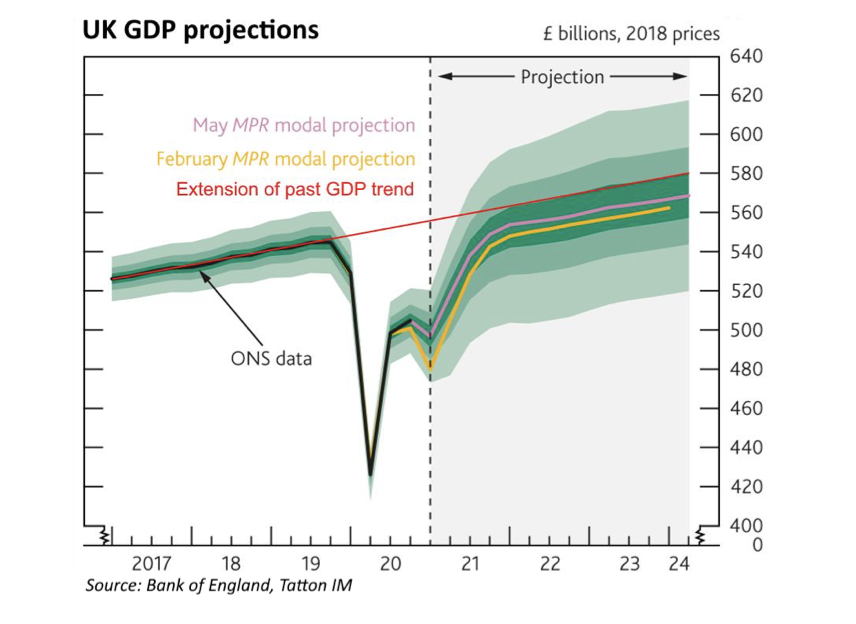

Haldane’s departure should mean less drama and more consistent messaging at the BoE, but we also suspect that it sets up the MPC for a more dovish stance (preferring lower rates). Despite holding policy steady, it delivered a substantial upgrade to growth forecasts for this year – up to 7.3% from 5.1%. This comes as other parts of the growth picture are also improving, including a doubling of how much savings the BoE expects to be used during the post lockdown bounce-back, and a much more favourable global growth outlook. Much like in the US, BoE guidance suggests it will consider tightening policy once inflation is consistently at or above its 2% target. According to its own forecasts, this means interest rates will follow the path currently discounted by the market, and likely stay on hold until at least 2023.

Despite the US Federal Reserve (Fed) officially changing its policy response framework last year favouring a bias toward loosening policy (with less emphasis on inflation and more on employment), the BoE maintains the same framework as before. However, the reality is that it cannot resist the wider change in global monetary policy; where the Fed leads, other central banks tend to follow. But we suspect the BoE’s stance also reflects a less rosy picture of the UK economy than it lets on. Despite the upgrade to short-term growth, when looking at longer-term forecasts we can see policymakers expect the economy to remain below its pre-pandemic trend for many years. According to its outlook from 2023 and beyond, the UK’s output gap will drop to 0%, meaning a permanent drop in activity compared to what was expected at the beginning of 2020. Our calculations put that at around 2.5% of lost GDP.

There could be several reasons for this. At the simplest level, we could take this as a sign that the BoE expects long-term scarring effects of COVID to hamper the UK economy indefinitely. But the downgrades could also be Brexit-related. With less immigration and higher barriers to investment, expected growth would likely have taken a hit even without the impact of the pandemic.

We suspect policymakers have ‘neglected’ to be specific about the reasons for the drop-off because of their political savvy. The BoE was greatly criticised in the run-up and aftermath to the Brexit referendum, after downgraded growth forecasts were derided in the media as part of ‘project fear’. Former Governor Mark Carney came in for particular criticism for his public musings, which Andrew Bailey is no doubt keen to avoid.

The flipside to this, however, is that the BoE could well be sending the government its own message on the economy. Reading between the lines of its forecasts, the MPC clearly believes that greater investment – both public and private – is needed to make up for what has been lost because of Brexit. This is likely to become even more of an issue once COVID effects fade and the recovery gets underway, but the BoE can only do so much to stimulate business investment. At a certain point, fiscal policy as well as trade policy progress will need to take some of the pressure off.

Paradoxically, any political news that damages the value of Sterling could end up helping the BoE. We have written before that, despite its continued easing, financial conditions in the UK are actually tight relative to global peers – in large part because of the recent strength of Sterling. If it comes back down – for better or worse – that would go some way to easing conditions. After all, once again, there is only so much the MPC can do.

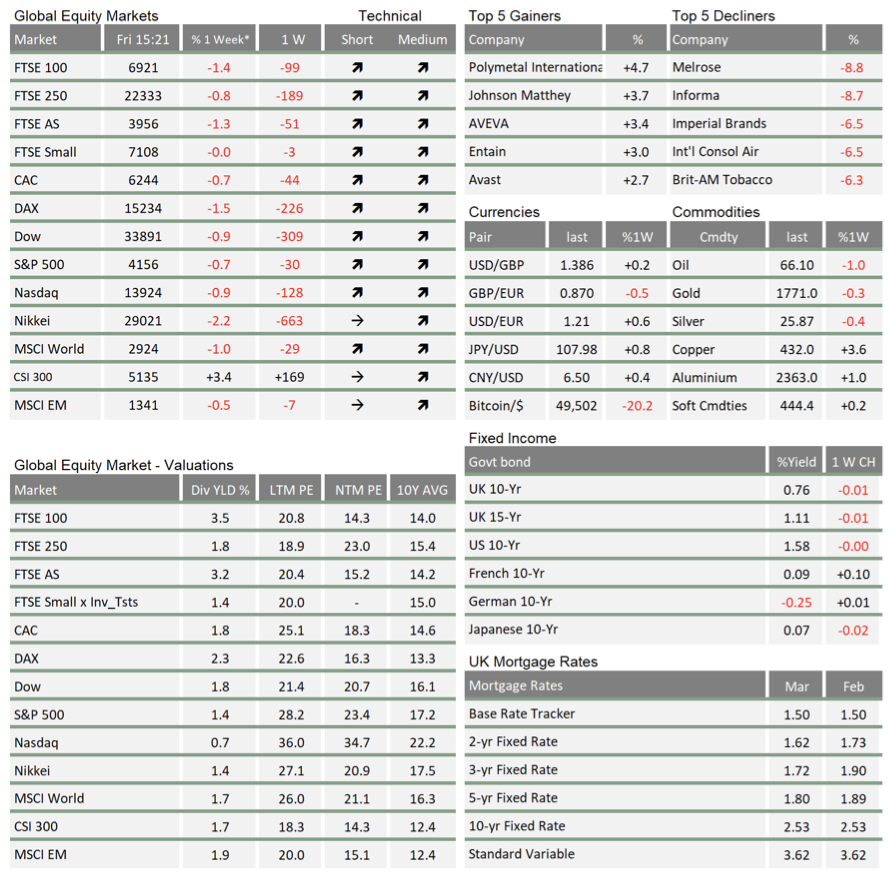

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.