Market Update November: New COVID Variant Flattens ‘Black Friday’ Feeling

It was a Thanksgiving week of mixed news. The European COVID case surge was surpassed in negative impact by the fears of a new variant emanating from South Africa. US markets hit new highs just before the holiday, but Black Friday has felt a bit dark. In itself, a new variant is not surprising. New variants are always a risk, but each of the past ones has been dealt with by the vaccines. Still, we cannot be complacent, and the next few days will be subject to uncertainty as the world waits for more information.

It was a Thanksgiving week of mixed news. The European COVID case surge was surpassed in negative impact by the fears of a new variant emanating from South Africa. US markets hit new highs just before the holiday, but Black Friday has felt a bit dark. In itself, a new variant is not surprising. New variants are always a risk, but each of the past ones has been dealt with by the vaccines. Still, we cannot be complacent, and the next few days will be subject to uncertainty as the world waits for more information.

Almost all market moves seem to be in line with the expectation of a hit to global growth. Government bond yields fell, although corporate bonds were less in favour because of credit risk concerns; oil, metal and equity markets retrenched. Travel and leisure companies were especially hard hit. The one slight oddity was that the US dollar fell rather than continuing its recent rally.

In the US, former president Donald Trump has indicated intentions to campaign for the 2024 election which, in turn, has pushed the Democrats to suggest Joe Biden will fight for another term. It’s probably too early really to know, and the mid-terms will be much more important. Biden is making headway now on both fiscal packages, which may aid his flagging approval rating but, right now, markets are betting on a gridlocked Senate and House. Of course, in general, many investors see that as a positive.

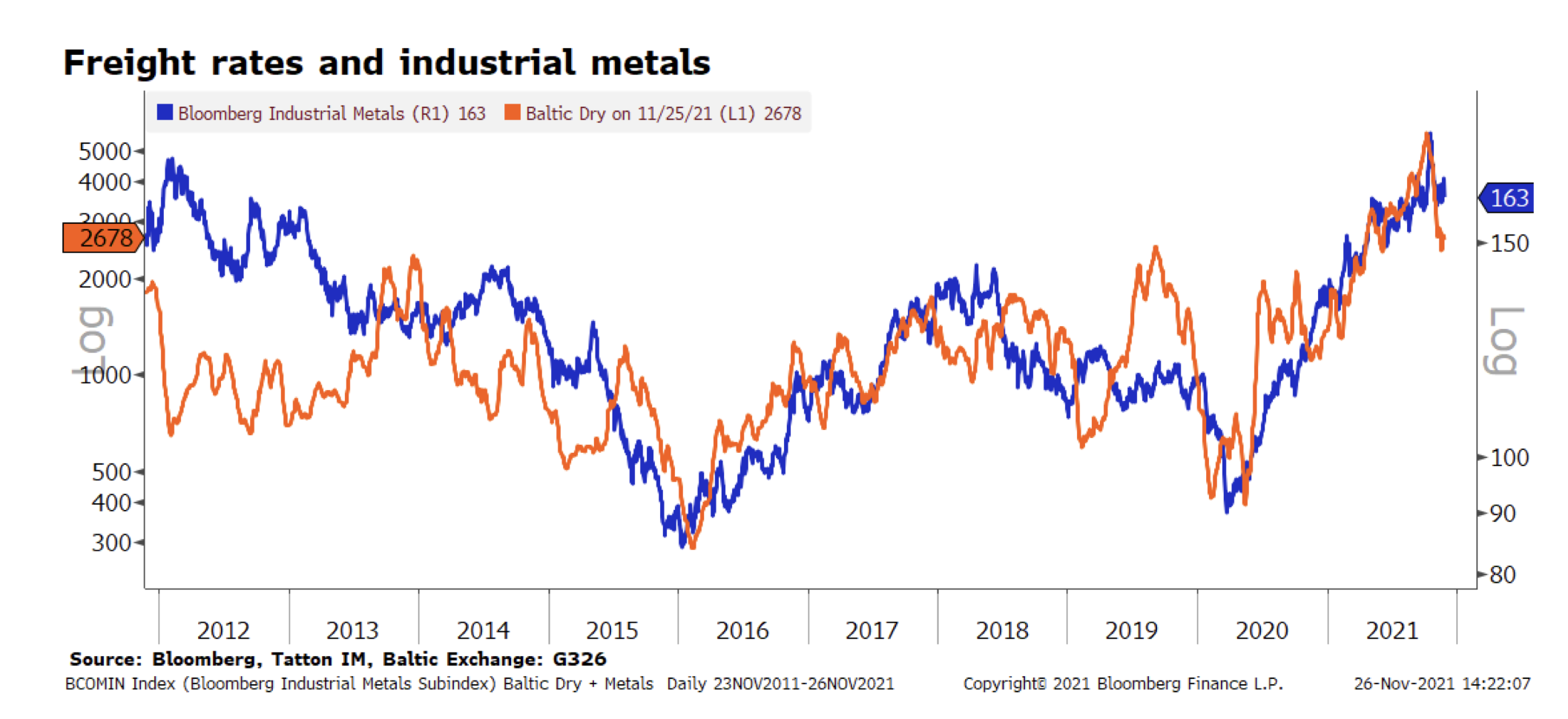

Indeed, there’s good reason to think that the global economy is on a bit of a roll. In the US, the weekly data on unemployment showed the lowest (single week) number of initial claims since 1968. The labour market has shifted into an even higher gear. Employment globally is strong, corporate confidence about sales is very positive, while there are signs that supply chain issues are easing up. There may not be enough truck drivers, but the container ships are moving more easily. One indicator is the Baltic Dry index (below) which seems to have peaked, and which may indicate a bit of potential slack in commodity prices.

However, the minutes from the last US Federal Reserve (Fed) meeting gave markets further reason to expect some attempt to exert a firmer grip on monetary policy in December, as does Jerome Powell’s reappointment as Chairman. The 6% year-on-year consumer price inflation is also testament to that and, as we’ve said before, the Fed’s policy is far from tight. Meanwhile, the European Central Bank (ECB) has followed the Fed’s earlier playbook in indicating a change to bond buying sometime in the future, but not for now. the ECB has a fixed envelope related to pandemic buying: the Pandemic Emergency Purchase Programme (PEPP) which is widely expected to be wound down. However, the Asset Purchase Programme (APP) already in place before the pandemic is expected to be increased to €40 billion, to ensure that the tapering is smoother.

But even a slight flex of the major central banks’ hand may affect markets. Perhaps we’re already seeing that in the prices of the more speculative assets. Bitcoin is going through another more volatile period, as is Tesla. Meanwhile, some of the ‘profitless’ smaller US growth stocks (early- stage companies which are yet to get into the black) have seen an exit of investors after a very strong run through 2021.

Global equity market breadth has narrowed as well. The recent winners have been the US mega- caps. Outside of these stocks, equity prices have been marking time. And, after the Q3 earnings season, US equity analysts have become less positive, with downgrades outnumbering upgrades for the first time since the start of the pandemic. Thus, the slow-moving policy tempo may coincide with the faster-moving virus news and lead to increased volatility. With markets still only just off their highs, there are plenty of profits in this year’s bag, and a big temptation to book it before trading volumes get too low.

Regarding global politics, we look at the new German coalition in the next article. Its formation was expected, but the good-natured approach offers hope for stability and pragmatism, while also making headway in green initiatives.

This week, the euro has weakened faster than the yen, which had previously been the leading decliner of the past three weeks. The yen is a bit of a conundrum. Japan has a structural current account surplus which one would usually associate with a strong (expensive) currency. The biggest factor in that surplus is a corporate sector which chooses to hoard rather than spend. It ought to drive investment capex, which ought to lead to strong profitability. But it hasn’t yet. We take a look at the yen and some implications of the incoming prime minister’s new fiscal package in the second article.

Asia has been a global growth weak spot, courtesy of China’s policy mix. Now, for the first time in a year, we have some positive signs. Admittedly Tencent was the subject of more regulatory pressure again. However, the People’s Bank of China has been increasing liquidity and the government appears to be back on a spending path. A rapprochement of sorts between the US and China could help trade, in which case there could be a welcome boost to real activity and a further easing of supply chain issues in the new year. In short, near-term wobbles may be present at the start of December, but with little to worry us too greatly.

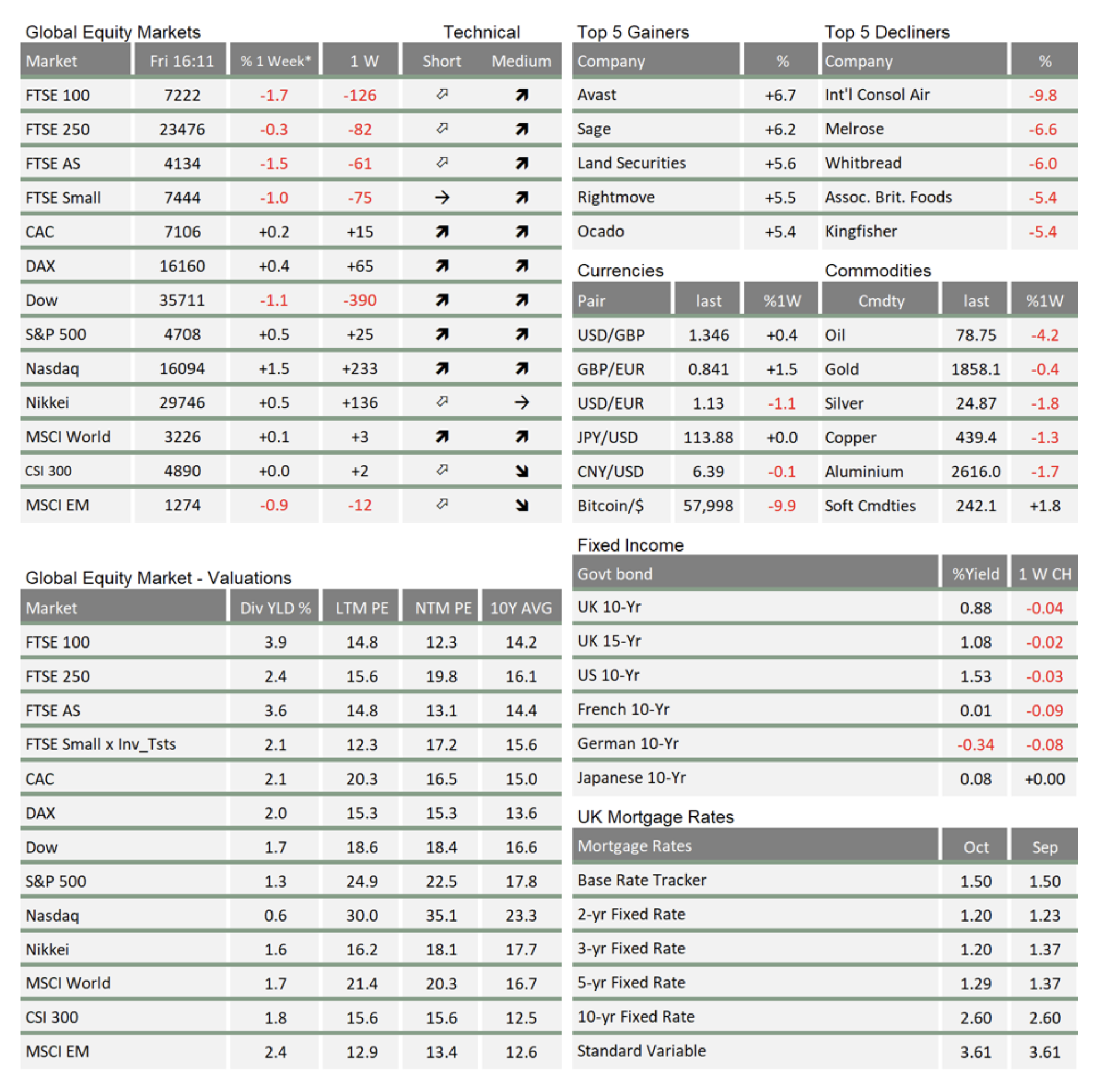

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.