Market Update June: Going up Sideways

May’s returns numbers are in, and the headlines are as follows: a rotation from tech to financials – and from value to growth – as well as a bit more downward pressure on bonds. We have included our usual ‘in review’ table and monthly comments below. Overall, it was a quiet month.

May’s returns numbers are in, and the headlines are as follows: a rotation from tech to financials – and from value to growth – as well as a bit more downward pressure on bonds. We have included our usual ‘in review’ table and monthly comments below. Overall, it was a quiet month.

After the sharp rise in economic growth expectations during the first four months of the year, economists in the US have grown used to a more measured pace of policy announcements, especially now that the Biden administration has passed its crucial ‘first 100 days’ yardstick. President Biden proposed a $6 trillion spend budget for 2022 which would have been unthinkable a few years ago. However, US politics has also reverted to its normal pattern when a Democrat is in the White House, with the Republicans just saying “no”.

Regarding bonds, the US Federal Reserve (Fed) announced that before autumn it would start selling the $14 billion corporate bonds it bought last year via an emergency lending facility. This is a tiny amount compared to the Fed’s overall balance sheet and had no impact on credit spreads, nor on other markets. As we have mentioned before, bond yields are much more stable now and equity markets quite like these periods.

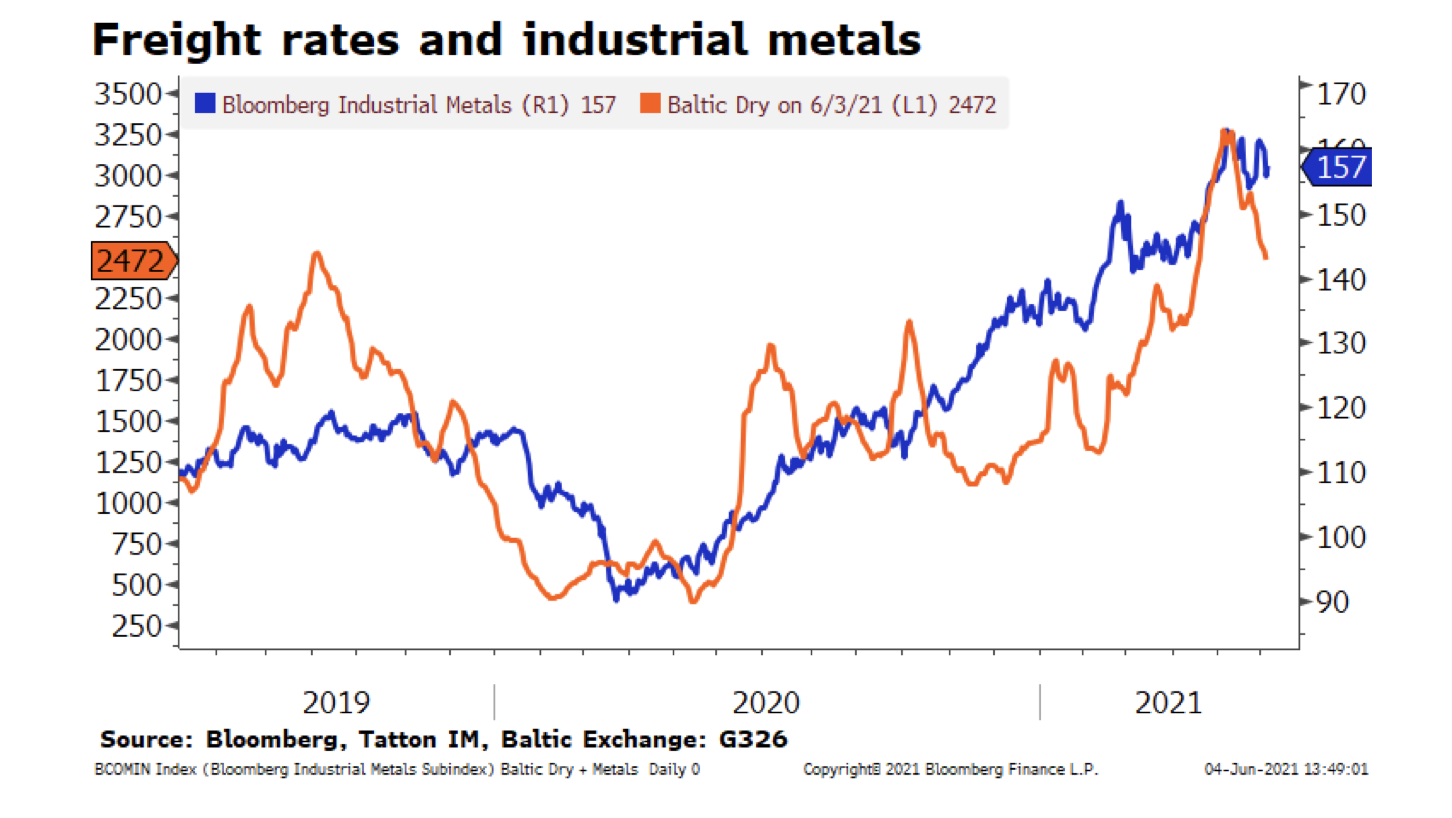

Corporate confidence remains elevated, as various Purchasing Manager Indices showed this week. Supplier delivery times are still long, and Chinese shipping prices have risen again during May. However, the Baltic Dry Index is showing signs of turning over from its recent highs and metals prices have also slipped somewhat recently, which may indicate a little less global pressure on goods prices.

This week, Morgan Stanley told us that analyst earnings expectations are stretched, and that some disappointment is around the corner. Improvements in the global economy are key to the earnings forecasts, and employment gains are the key to the global economy’s progress. The US non-farm payroll (new jobs count) increased by 559,000, which was below expectations, but not disturbingly so. Equities rose a bit, while bonds were unchanged.

As investors, one of the challenges we face is to identify trends in the global economy and then work out how to invest in the assets benefitting from those trends. One such trend could be a second phase of globalisation. The first phase was a big expansion of global trade into emerging nations. The second phase will be about those nations moving into a more developed framework.

This week, the FT’s David Pilling wrote about last year’s statement from Ghana’s president that the world’s second largest cocoa producer might consider stopping the export of cacao beans to Switzerland, one of the world’s largest chocolate manufacturers. Essentially, Pilling makes the point that emerging economies will eventually ‘emerge’. They will no longer need to rely on neo- colonial countries to gain some small part of the value chain. Rather, the people of that country will have the necessary skills and organisation to do it for themselves.

The exploitation of emerging market countries rich in raw materials has been going on for centuries. However, for modern food, oil, and mineral companies (such as Nestle, BP, Shell and Rio Tinto) the current global political climate looks especially challenging. Now the G7 appears on the brink of agreeing to a 15% “global minimum corporation tax”, all global companies will probably have to face up to paying more tax. While this is mostly targeted at the tech platforms, it will have an impact on older companies as well. However, the emerging markets’ rising confidence in their pricing power is a threat to their margins which may continue over a long period. Of course, that is in addition to the climate change pressures that are already coming to the fore.

To combat these pressures, companies will need to be prepared to change their cultures radically and swiftly. Some are making efforts, but have a long way to go. Still, these companies have become global giants through their ability to “get stuff done”, especially when it comes to physical infrastructure. It is likely that the way we view these companies will change dramatically in the next few years, and change of that sort can be exciting and potentially profitable.

For the emerging nations, the improving governance structures which lead to pricing power is an all-round positive. The general deepening of their economies should benefit all domestic asset classes. Of course, no country’s path can be smooth, but the focus on removal of corruption is an enormous gain. As in the 1990s, it may be that global growth will happen at the same time, but the reasons to be positive on emerging markets may lie elsewhere.

There is a worry about the inflationary impact this may bring to the established economies. Perhaps we shouldn’t get too hung up about this, as such effects will take place over a long period. However, it would be fair to say that while the first phase of globalisation was disinflationary, the second phase will probably be mildly inflationary.

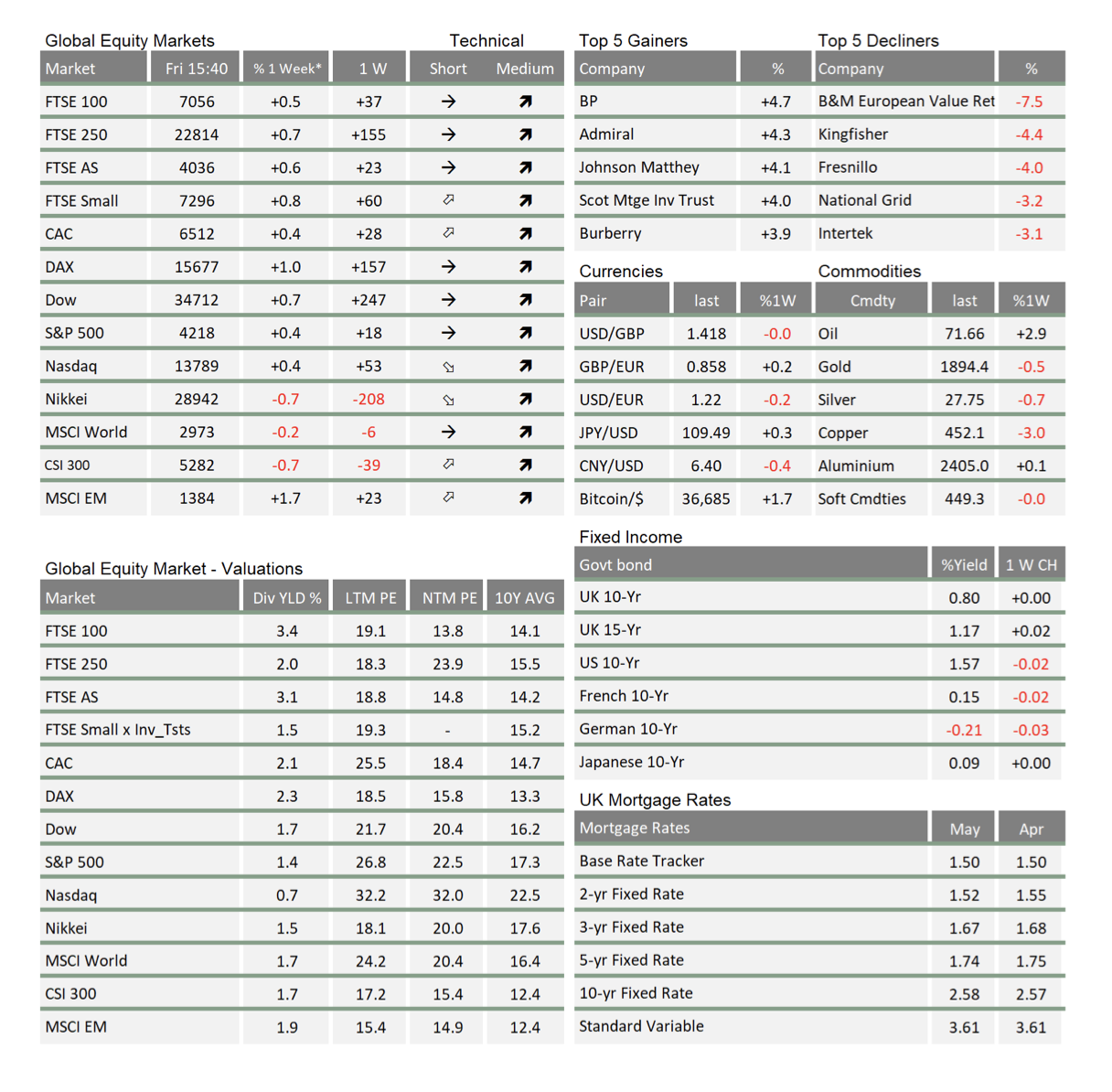

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.