Market Update: Don’t fear the rebalance

Capital markets were choppy last week, unsurprisingly. At the end of a very strong year in stock markets, investors typically rebalance their holdings and take profits, so mild selling pressures are to be expected. This absence of a Santa Rally should not be taken as a sign of underlying risk sentiment deterioration. On the contrary, overall risk appetite feels strong – particularly from bullish US investors.

Syria’s sudden revolution had all the makings of a classic geopolitical shock – completely unexpected, with the potential to escalate and disrupt energy markets – and yet markets were largely unaffected. We seem to be in a cycle of big geopolitical stories popping up only to die down just as quickly, as with South Korea’s ‘martial law for a day’. Last week, South Korean markets and currency bounced, following the negative impacts from their President’s bout of near-insanity.

Geopolitics will swirl around markets through the holiday period, with Syria’s regime change now added to the mix. These stories are unnerving when they happen, but maybe it is a pattern we will have to get used to. You certainly would not bet against more short-lived geopolitical flares during a second Trump presidency.

For Europe, the focus will remain on noises from the Ukraine-Russia conflict. It continues to have a depressing effect on Europe’s economy, one which has worsened through the year. Thus, the ECB continued its path of lower rates with a cut in the deposit rate of 0.25% (to 3%). This was actually a disappointment of expectations, although the statement and press conference (often the most important parts of the decision-day process as they provide forward guidance) were slightly dovish.

Shares in Alphabet, Google’s parent company, burst upwards after a reported breakthrough for its quantum computing chip. The supercomputers it could support are a long way from being deployed, but Google proclaimed that the chip can solve an artificial test problem a mind-boggling 10^25 times quicker than the other fastest computers in the world by approximately.

The speed of Alphabet’s rally made it look like a short-squeeze of investors who had bet against the firm, probably exacerbated by low year-end volumes. But it is notable that investors seem to have shrugged off Google’s antitrust litigation – which as it stands could still see the tech giant broken up. No one really knows what will happen to the myriad Biden-era tech antitrust cases now, but tech executives are cosying up to Donald Trump’s team (like Mark Zuckerberg’s donation to Trump’s inauguration fund), if that is any indication.

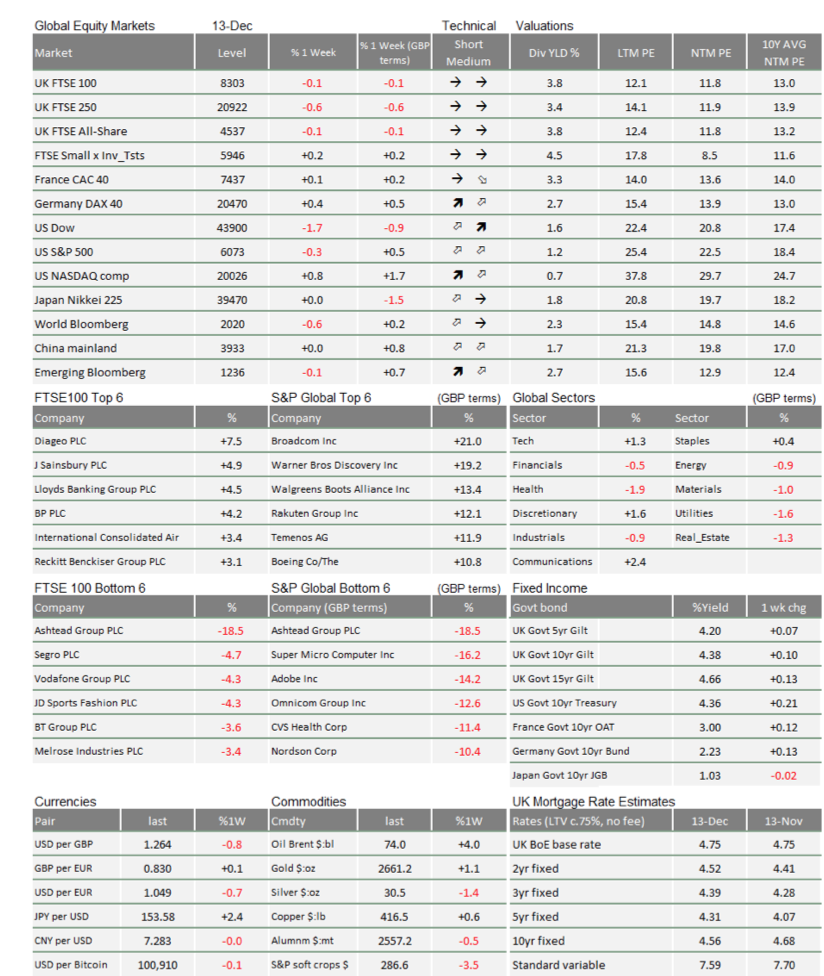

China announced more policy action, but this was once again more a signalling of intent than specific proposals. The clearest imminent actions related to monetary policy and so the Chinese 10-year bond yield fell to 1.75%, while the currency shifted weaker against the US dollar. But, as has happened frequently after policy ”announcements”, equities could not maintain the early gains. Maybe next year will be different.

With risk appetite strong and central banks cutting interest rates – the Swiss and the Canadians also cutting by half a percentage point – investors might wonder: Will we get the famous ‘Santa Rally’ heading into Christmas? It depends on your expectations.

Equities probably will not keep surging into year-end as they did last December – but that came after a really mediocre year for markets to that point. This year, prices have moved up relatively uninterrupted since the autumn. We currently see many of the same themes as this time a year ago: central banks have pivoted to more accommodative policy, US growth is expected to strengthen and big tech in particular is benefitting. In one sense, the Santa Rally has been going on for quite a while.

That is the gift that US markets have given to global investors. Many – particularly US investors – think it will keep giving into the new year. That is not an entirely unreasonable expectation, but we would suggest some caution. We discuss this in more detail in our yearly outlook.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.