Market Update November: Dollar strength and divergence caps a dull week for investors

Despite the negative news flow, be it COVID or politics, UK consumers are proving their resilience once again with both October retail demand and domestic consumer sentiment pointing up. Perhaps the buoyant jobs market is encouraging the UK public to be less concerned about inflationary pressures eating into their disposable incomes than some economists would expect, or it is equally possible that higher energy and food prices have not quite hit home yet.

Despite the negative news flow, be it COVID or politics, UK consumers are proving their resilience once again with both October retail demand and domestic consumer sentiment pointing up. Perhaps the buoyant jobs market is encouraging the UK public to be less concerned about inflationary pressures eating into their disposable incomes than some economists would expect, or it is equally possible that higher energy and food prices have not quite hit home yet.

Whatever the cause – and usually there are several – the UK microcosm neatly reflects the ongoing dispute about the current bout of inflation that continues to separate academics and investment analysts into opposition camps of ‘permanent’ and ‘transitory’. The most recent elevated inflation readings of over 4% across Europe/UK and over 6% in the US seem to settle the argument in favour of ‘permanent’. Interestingly, the ‘transitory’ camp has not given up, pointing towards all the anomalies that can be found everywhere in this unusual recovery.

Their most relevant themes are that inflation pressures have been driven by a significant shift in consumer demand – away from services towards physical goods – and the increased costs of energy while wage rises remain focused on a few very specific sectors (and typically the lowest paid). Given travel and general social activities can be expected to return as a more considerable proportion of consumer demand as the pandemic turns endemic over the coming year, and that energy supply shortages are expected to ease by the energy sector itself, it is not too hard to see where camp ‘transitory’ is coming from. Camp ‘permanent’ also appears to neglect the effect that higher prices and surging demand have on the ‘animal spirits’ of market economies, where all recent signs from the corporate world have been pointing towards a rapid ramping up of economic activity to satisfy demand before it changes its mind.

In our view, inflation pressures are real and more longer-lasting than anticipated, but they are also not surprising given the upheavals the global economic system has gone through while consumers are also suddenly displaying a very different demand function. However, we also expect many of the factors that are driving up this pressure now to reduce meaningfully over 2022. This should mean that the 2021 aggregate upward price push is likely to prove permanent, whereas inflation above 2-4% will not turn structural but instead prove to have been a transitory element of the COVID recovery, and part of the awkward transition phase to a mid-cycle environment of economic expansion.

Capital markets appear to continue to have a similar view, with market-derived inflation expectations elevated for the near term, but then trending lower for the longer term. This observation segues neatly into the other mayor observations of the week, which was renewed strength of the US Dollar, especially against the Euro.

Long-time readers of The Tatton Weekly may remember us writing in the past how the direction of inflation-adjusted yields in the US fixed interest markets have provided a decent indicator for the direction of the exchange rate (FX) of the Dollar. Well, recently this signpost has not been as useful, with the Dollar rising considerably despite US real yields falling. There have been many attempts made at rationalising this unusual behaviour, but it would appear to boil down to – you guessed it – COVID. The big up move by the Dollar on Friday morning which took place as Austria became the first European country to reimpose a full lockdown, in a bid to arrest the rapid increase in new COVID cases, seemed to confirm our suspicion.

US Dollar strength appears to anticipate that the European Central Bank (ECB) will be forced to keep interest rates lower for longer than will be the case in the US. Since last year’s COVID waves, the recovery of western economies had been progressing more or less in lockstep, but it seems this may be about to change as central banks start to diverge on their journey towards monetary normalisation. Unfortunately, this would not be great news for the cyclical rebound, as a strong Dollar has in the past always been a considerable headwind to global trade and especially the economic health of emerging markets.

As always, short-term market movements do not make a trend, but continued Dollar strength has the potential to slow the recovery more than is already priced in on the back of the existing headwinds discussed above.

Not surprisingly then, that investors experienced another dull week in terms of market movements, and it is entirely possible this might extend through to the pre-Christmas period. While dull is perhaps no bad thing as we move towards the end of what has been a very pleasing year for investors thus far, we would be saddened if we were robbed of the promise of the year-end joy that the seasonal Santa Rally brings at the end of the year.

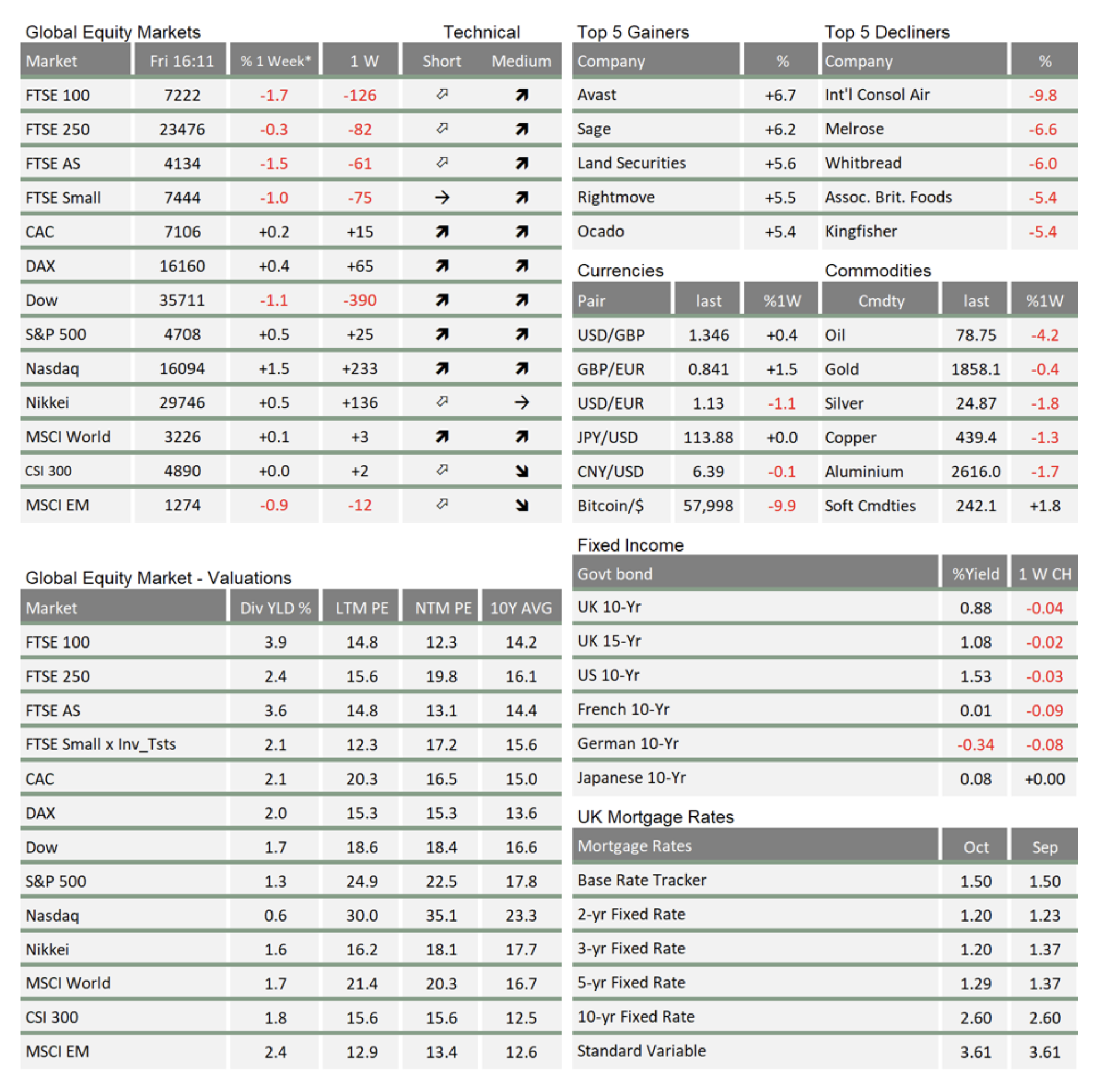

* The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values

** LTM = last 12 months’ (trailing) earnings;

***NTM = Next 12 months estimated (forward) earnings

Please note: Data used within the Personal Finance Compass is sourced from Bloomberg and is only valid for the publication date of this document.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.