Market Update: Calmer markets ahead of Trump inauguration

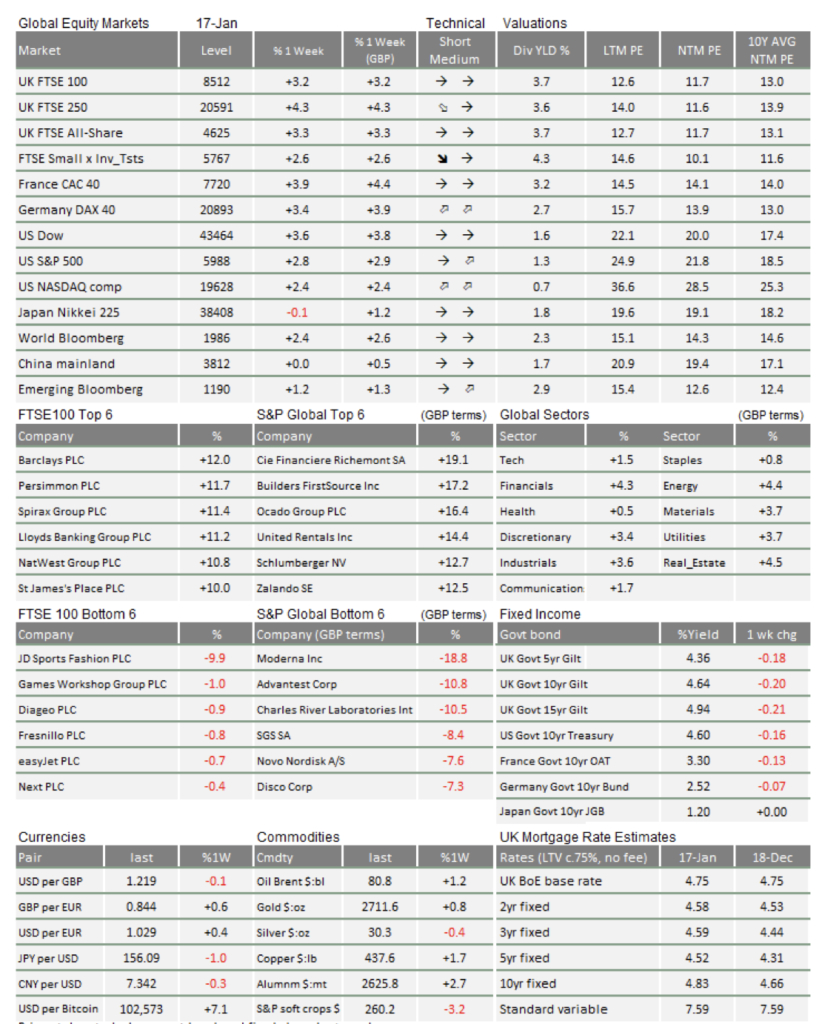

With global stocks bouncing back over 2%, last week was the best of the year! UK investors did not even have to rely on a weak pound to bolster Sterling-based returns. French stocks gained over 4%, while smaller cap stocks in most regions have outperformed larger caps – all good signs for broad-based growth.

Prices were helped by notably better bond markets – both here and in the US. One of the biggest concerns previously was that inflation would stay too high, stopping central banks from cutting interest rates further. Relatively benign inflation data released last week was enough to challenge that narrative, and markets breathed a sigh of relief. Investors now look ahead to Donald Trump’s inauguration next Monday. His policies will be a major driving force for markets this year, but we still do not know for certain what those policies will be. Thankfully, we start this impactful presidency in a calmer mood than we might have.

Gilt tantrum ends and the Bank of England softens its tone.

We said the week before last that the sell-off in UK government bonds (gilts) looked excessive. Sure enough, last week gilt prices rebounded, meaning lower yields. We end the week with the 10-year gilt at 4.64% and a yield decline of 0.2% from the previous level. This was helped by chancellor Rachel Reeves reiterating her commitment to fiscal discipline and, more substantially, by news that UK inflation undershot expectations last month. The important thing for the UK economy is that inflation data have made an interest rate cut at next month’s Bank of England (BoE) meeting more likely.

It got a little lost in the news coverage, but there was a notably dovish speech (preferring lower rates) from Alan Taylor, the BoE’s most recently appointed external Monetary Policy Committee member. Taylor clearly indicated that he thought UK rates were too high and should fall quickly. This is refreshing to hear, as much of the commentary about the UK economy has painted it as stuck in an inescapable low growth, high inflation trap.

Most analysts agree that annual inflation will move back above 3% in the coming months, if only because of higher energy prices. However, we have said for a while that there is a strong case for the BoE to ‘look through’ the near-term inflation data and focus on supporting growth. Judging by Taylor’s speech, at least one BoE official seems to agree. Energy prices will bite but are unlikely to induce further inflation. The effect of the national insurance rise is less certain – and the BoE will monitor it closely – but there is every chance that higher employment costs end up increasing unemployment and lowering wage pressures, hence decreasing long-term inflation pressures.

Markets hope the Fed can loosen policy.

As usual, global investors are more focussed on the US, where there have been similar fears about sticky inflation, stoked by last week before last’s strong jobs report. Those fears receded last week, thanks to an inflation report that was judged to be benign. Inflation was actually firmly in line with expectations (and higher than the previous month) but investors reacted as if it was below them.

The most encouraging signals are that wage growth is not especially high – despite job gains – and shelter costs are no longer contributing to inflation to the same extent they were. It is also clear that high interest rates are compressing economic activity, which you can see in the data for mortgage borrowing. This means that the Federal Reserve has room to become a little more accommodative, starting with a likely rate cut at the end of this month.

A looser Fed would be very welcome for capital markets globally, considering that global financial conditions have been getting tighter. This has partly been about the rise in bond yields (which thankfully fell back last week) but also due to the significant strengthening of the dollar. Because the dollar is the currency of global trade, a stronger dollar effectively means higher financing costs outside of the US (e.g. for emerging market companies that borrow in dollars but get revenues in their local currency).

Global uncertainties ahead of Trump 2.0.

Last week’s calmer bond markets are therefore welcome, but we should remember that global liquidity still looks tighter than for most of 2024. That means that forecasts for global growth are likely to be revised downwards as we go through the year – which is not a great environment for small companies in particular. It was notable that the equity bounce back became much more focussed on the usual US tech mega-caps as the week went on, having initially started in smaller cap stocks.

Oil prices also moved up, despite the historic Middle-Eastern ceasefire agreement, and the implication of fewer regional tensions. Oil’s rally looks like a pure supply-side story, coming after fresh US sanctions on Russian shipping. Prices for short-term oil contracts increased sharply, but longer-term contracts did not go up by the same amount. For the longer-term, the balance of global demand still points to lower growth.

This sets things up interestingly for Donald Trump’s inauguration on Monday. There are hints that Ukraine will be among the next administration’s top priorities during the early days – even ahead of the tariffs Trump has talked so much about. The standard assumption is that Trump will pressure Ukraine into ceding territory to get a quick resolution, but we have been having interesting discussions last week which suggest the opposite (more support for Ukraine) could happen.

No one knows for sure. Trump’s second term brings uncertainties, but plenty of potential rewards for investors. At the least, it is good that we start the four years with calmer markets than we saw at the start of the year. Long may that continue.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.