Download our latest FREE Personal Finance Magazines and Financial Guides , found in our Digital Library.

Budget 2017: What you need to know to make the most of your financial choices

The Chancellor’s Budget on 8 March was the first of two due in 2017. The final spring Budget came little more than three months after an Autumn Statement that suggested government finances had taken a post-referendum turn for the worse. However, the latest short-term economic numbers turned out much better than the Office for Budgetary Responsibility’s (OBR’s) November projections.

This good news gave the Chancellor a little ‘wriggle room’, but instead he chose to offset some modest increases in spending – mostly focused on social care – with tax and NIC rises mainly aimed at the self-employed. For once, the volume of Budget documents issued by the Treasury shrank significantly, but there were still some surprises to be found in the detail…

BUDGET HIGHLIGHTS

A reduction in the dividend allowance from the current £5,000 to £2,000 from 2018/19.

A 1% increase in the main Class 4 NIC rate to 10% for 2018/19 and a further 1% addition to 11% for 2019/20.

A one year deferral in the start date for Making Tax Digital (MTD) for unincorporated businesses and landlords whose turnover is below the VAT threshold (£85,000 from 1 April 2017).

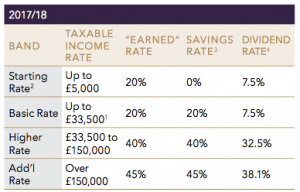

An increase in the personal allowance for 2017/18 to £11,500 and a corresponding rise in the higher rate threshold to £45,000, although in Scotland the latter figure will only apply to savings and dividend income.

A new 25% tax charge on transfers to qualifying recognised overseas pension schemes (QROPS), other than for those who have ‘a genuine need’ to transfer

Three measures to help small businesses cope with the changes to business rates, due to take effect in April 2017, starting with a new £50 a month cap (in 2017/18 only) for businesses that lose Small Business Rate Relief.

PERSONAL TAXATION

Income tax

The personal allowance will increase to £11,500 and the higher rate threshold will rise by £2,000 to £45,000 for 2017/18. In Scotland, the 2017/18 higher rate tax threshold will remain unchanged at £43,000 for non-savings, non-dividend income only.

The personal allowance will increase to £11,500 and the higher rate threshold will rise by £2,000 to £45,000 for 2017/18. In Scotland, the 2017/18 higher rate tax threshold will remain unchanged at £43,000 for non-savings, non-dividend income only.

National insurance contributions

The national insurance contribution (NIC) upper earnings limit and upper profits limit will increase to £45,000 for 2017/18, in line with the higher rate income tax threshold.

Class 4 NICs will increase from 9% to 10% in April 2018, coinciding with the abolition of Class 2 NICs. A further increase to 11% is set for April 2019.

Dividend allowance

The tax-free dividend allowance, which was introduced at a level of £5,000 in 2016/17, will be reduced to £2,000 from 2018/19.

Different forms of remuneration

• Benefits in kind: The government will publish a call for evidence on exemptions and valuation methodology for the income tax and employer NICs treatment of bene ts in kind (BiKs). Legislation in Finance Bill 2017 will set the date of 6 July for an employee to make good on BiKs which are not accounted for in real time through PAYE (BiKs that are not payrolled). This legislation will take effect for tax liabilities arising from 2017/18.

• Accommodation benefits: The government will publish a consultation with proposals to update the tax treatment of employer-provided accommodation and board and lodging. This will include proposals for when accommodation should be exempt from tax.

• Employee expenses: The government will publish a call for evidence on the use of the income tax relief for employees’ expenses, including those that are not reimbursed by their employer.

PENSIONS, SAVINGS & INVESTMENTS

Money purchase annual allowance

Money purchase annual allowance

The money purchase pension annual allowance will be reduced to £4,000 from £10,000 for 2017/18, following a consultation issued with the Autumn Statement.

Qualifying recognised overseas pension schemes

There will be a 25% tax charge on pension transfers on or after 9 March 2017 to qualifying recognised overseas pension schemes (QROPS). Exceptions will be made to the charge, allowing transfers to be made tax free where people have ‘a

genuine need to transfer their pension’ and:

- Both the individual and the pension scheme are in countries within the European Economic Area (EEA); or

- If they are outside the EEA, both the individual and the pension scheme are in the same country; or

- The QROPS is an occupational pension scheme provided by the individual’s employer.

Changes to tax treatment of foreign pensions

From 6 April 2017, the treatment of foreign pensions will be more closely aligned with the UK’s domestic pension regime, as previously announced. Legislation will clarify that all lump sums paid out of funds built up before 6 April 2017 will be subject to the existing tax treatment.

Life insurance policies

Life insurance policies

As previously announced, the tax rules for part surrenders and part assignments of life insurance policies will be amended to allow policyholders who have generated ‘a wholly disproportionate gain’ to apply to HMRC to have the gain recalculated on ‘a just and reasonable basis’. The changes will have effect from Royal Assent.

NS&I Investment Bond

The rate on the new NS&I Investment Bond announced at Autumn Statement 2016 will be 2.2%. The bond will have a three year term and will be available for 12 months from April 2017. It will be open to anyone aged 16 and over, subject to a minimum investment of £100 and a maximum of £3,000.

CAPITAL TAXES

Capital gains tax

The annual exempt amount (AEA) for individuals and personal representatives will rise to £11,300 for 2017/18, while the AEA for most trustees will increase to £5,650 (minimum £1,130).

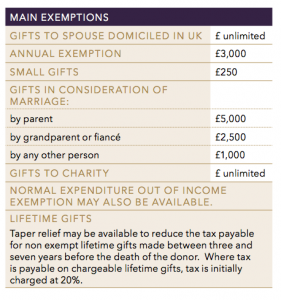

Inheritance tax

The nil rate band remains at £325,000. New deemed domiciled rules apply from 6 April 2017 for inheritance tax (as well as income tax and capital gains tax).

BUSINESS TAXES

Corporation tax rates

Corporation tax rates

As previously announced, the rate of corporation tax will fall to 19% from April 2017 and to 17% in 2020.

Tax treatment of appropriations to trading stock

Businesses with loss-making capital assets will not be able to obtain a tax advantage by converting them into more exible trading losses. The changes take effect from 8 March 2017.

Tax simplification for cash basis

The entry threshold for the cash basis of assessment will be increased to £150,000 and the exit threshold will rise to £300,000. The rules on capital and revenue expenditure within the cash basis will be simpli ed to make it easier for businesses to work out whether their expenditure is deductible for tax.

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

DISCLAIMER:

This blog and its attachments or links should not be relied upon as advice, except to the extent that advice is set out in an attached bespoke Suitability Letter. Information is based on our current understanding of taxation legislation and regulations. Any levels and bases of, and reliefs from, taxation are subject to change. The value of investments and income from them may go down. You may not get back the original amount invested.Past performance is not a reliable indicator of future performance.