Market Update: Waning momentum – growing concerns

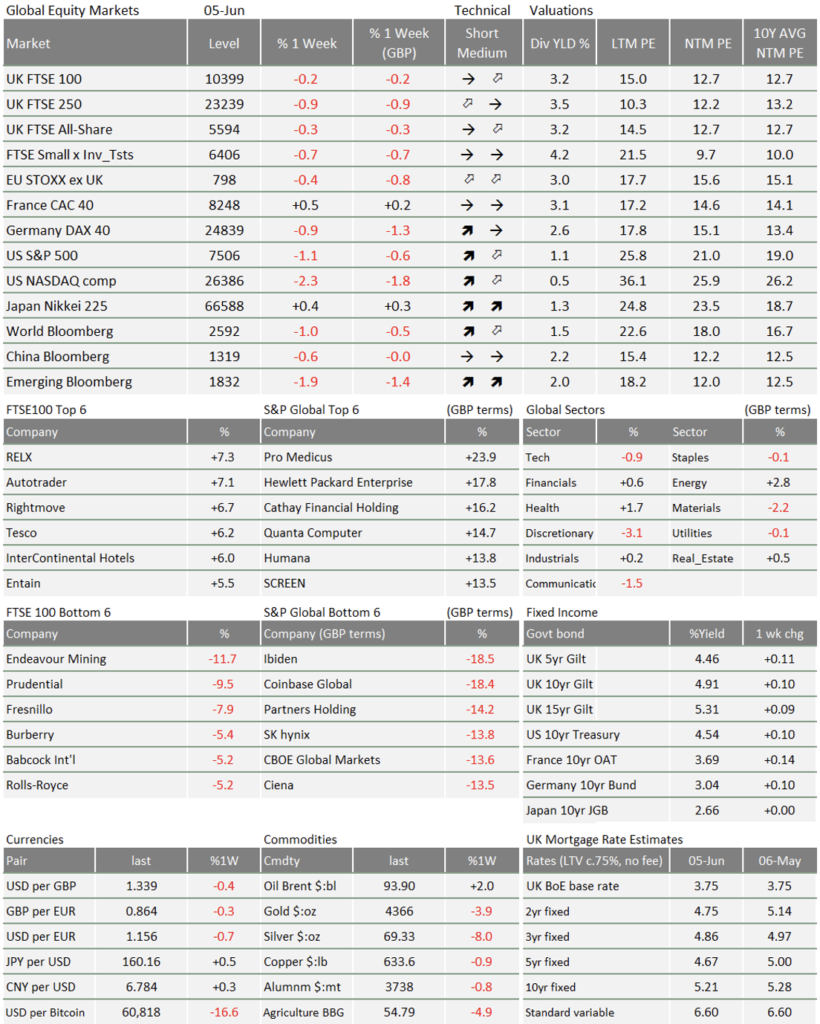

Until Friday lunch time, it was a fairly dull week for markets. News of an Israel-Hezbollah ceasefire eased concerns but did not materially change the Middle East stalemate. As at Friday afternoon though, traders were digesting a stronger than expected US employment report. May’s surprising bounce in job creation suggests a stronger US economy than might have been expected, given higher fuel prices.

Bond yields bumped higher after the US data. Investors had been rotating away from the tech darlings towards more ‘ordinary’ stocks, but they now appear more focussed on potential interest rate rises than economic growth. The US IT-led rally from the start of April is waning, and markets are down about 1.5% as at Friday, although a stronger US dollar is offsetting some of that weakness in sterling terms.

Past peak hype?

Shares in semiconductor manufacturer Micron dropped 7% on Thursday, after disappointing sales projections from competitor Broadcom. That is partly profit-taking, after a phenomenal few weeks for AI chipmakers. But it is also a realisation that manufacturing microchips is a cyclical business after all – AI boom or not. Micron’s sell-off came just days after it announced a massive increase in production. Make hay while the sun shines, at least.

This particular chapter of the AI investment story might be ending. Google owner Alphabet’s plan to raise $80bn in fresh equity issuance triggered a fall in the broader ‘Magnificent Seven’ US tech stocks. With trillion-dollar IPOs looming from SpaceX, OpenAI and Anthropic, investors worry that there might be too many new shares for the market to swallow.

Investors did not mind big tech firms borrowing billions to develop AI last year, as long as debt issuance did not disturb their incredible earnings-per-share growth. Equity issuance is different. That requires extra money coming into the market – just to keep share prices level. That extra capital will have to come from somewhere, most likely sales of other assets. That might also explain last week’s market rotation.

Trade and capital barriers re-emerge

The US is pursuing protectionism again – this time by imposing 10-12.5% tariffs on trading partners that (Washington claims) are not enforcing laws against forced labour. It is a thinly veiled attempt by the Trump administration to claw back the tariff revenues that it will soon lose out on, once the 10% universal tariff expires next month, following a US trade court ruling.

The “Section 301” tariffs will replace the expiring “Section 122” and create another set of regulations, but they will not change end prices. Effective tariff rates will rise from 10.2% to 10.7%, according to Bloomberg Economics, well below the original IEEPA tariffs. Further US tariffs are likely, but we doubt there will be reciprocal tariffs from trading partners.

There will be other protectionist measures, however. US companies’ increasing need for capital is unlikely to be sated by China, after Beijing announced tighter restrictions on Chinese tech investment going overseas. The regulations have been in the pipeline for a while and will come into effect next month, rather conspicuously preventing many Chinese investors from buying into the slew of US tech IPOs. The ‘overseas’ designation includes Hong Kong, Macau and Taiwan, which hurt HSBC and AIA shares.

The “protective and defensive” measures are designed to stop foreign entities contravening national interests. Beijing is no stranger to capital controls, but it is still significant to see them used explicitly as a weapon in the US-China tech race. We suspect the government has another reason to keep Chinese money at home too – to direct China’s massive savings pile into the domestic market.

Just as markets were feeling better about the Middle East’s impact on global trade, fresh hurdles arise.

Show me the money supply

Retail investors are not as happy as they were a few weeks ago, particularly in the cryptocurrency market. We see this in Bitcoin’s 20% monthly fall in dollar terms. Meanwhile, cryptocurrency exchange volumes have been consistently falling in 2026.

Under new Federal Reserve Chair Kevin Warsh, Bitcoin’s prospects are unlikely to change. Warsh plans to change (reduce) the way the central bank provides liquidity to the financial system, weaning markets off the Fed’s bond buying support that has sustained them for nearly two decades. That is a respectable aim, but one that will inevitably weigh on asset price valuations – particularly speculative assets like crypto.

Since the global financial crisis [GFC] of 2008, we have seen a dramatic rise in M1, the narrow measure of central bank-generated money, i.e. cash. However, M4, the broadest measure that includes bank deposits and certain financial instruments, has remained fairly static. Warsh’s argument is that, by reducing reliance on M1, banks will be forced to create money through lending, boosting M4 and driving economic growth. That could well be positive for the economy, but tighter general liquidity is not good news for equity price-to-earnings valuations. Hopefully, valuation pressure would be offset by higher profit growth, but it is a worry for stocks nonetheless.

We do not expect Warsh to unveil this plan at his first Fed meeting as Chair later this month. The Fed will almost certainly leave interest rates and balance sheet operations unchanged – though May’s strong employment data increases the chances of a hawkish signal. Before that, the ECB will meet and is all but certain to raise rates from 2.15% to 2.4%.

The Bank of Japan is likely to raise too, while the Bank of England will probably keep rates steady but signal a hike ahead. Although energy prices are pushing up headline inflation, central bankers are helped by some fairly weak core inflation (excluding volatile food and energy).

Warsh’s balance sheet reduction plan is likely to come up at the Jackson Hole conference for central bankers in August. Markets have mostly convinced themselves that Warsh does not have enough power or support at the Fed to implement his grand plan by himself. That may be true, but his recent appointment of two seemingly ideological advisers (one of whom contributed to infamous MAGA initiative “Project 2025”) gives the impression of a Fed chair preparing to fight. Markets will watch that conference even more closely than usual.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.