Market Update: Challenged optimism

The Iran War keeps dragging down markets. Israel’s strike on Iran’s South Pars gas facility, followed by Iran’s strike on a Qatari liquified natural gas facility – the largest in the world – saw crude oil spike above $115 per barrel and European natural gas prices surge. The FTSE 100 dropped 2.3% on Thursday, and European stocks similarly fell. Escalation has forced markets to reconsider their optimistic view on the extent of the war. At the same time, though, we suspect these events have made de-escalation more likely.

The events have worsened market liquidity as geared investors had honour margin calls – which could become its own issue. As we write, energy prices are down from Wednesday’s highs, but both equity and bond markets are struggling.

Israel isolating itself and Trump looking for an ‘off-ramp’?

We wrote last week that, despite choking short-term oil supply, neither side of the war looked likely to destroy long-term oil and gas production. Cue the US attacking military targets on Kharg Island – through which 90% of Iran’s oil exports flow. Tit-for-tat gas site attacks this week marked a more disruptive phase of the war for long-term global growth. Further escalation in this direction will panic markets even more.

President Trump threatened to “blow up” the South Pars gas field if Iran continued striking Qatari sites, but the subtext was that he disapproved of Israel’s initial South Pars attack. Regardless of Israel claims that it coordinated the strike with the US, Trump clearly does not want Israel to attack energy infrastructure in a way that hurts the US’ other Middle Eastern allies.

This backs up the narrative that Washington is looking for a way out of what they started. It is increasingly clear that Israel has its own objectives, which might conflict with the US, and with the Arab nations with which Israel had improved relations in recent years.

The US already has an incentive to de-escalate, and it might try to create an Israeli incentive to do the same. But incentives do not always turn into actions. This is a nervous phase for markets. Everyday without a resolution looks like a bigger threat to the world economy, rather than just a short term energy price push.

War hurts markets in unexpected ways

The fear factor is having strange effects on markets. Russia – one of the few clear winners from the oil shock – saw its currency drop this week. Energy import-dependent China saw its currency fall too, but similarly dependent Japan saw the yen rise.

Strangest of all was the significant fall in gold prices. Gold is the stereotypical ‘safe haven’, but prices have dropped more than 10% since the war started. Counterintuitively, this could be a signal of a need for liquidity. Central banks are signalling tighter monetary policy and people need cash right now. Gold may not appear currently to be functioning as a safe haven, and speculative traders who have put on leveraged positions will be wondering what is going on. However, many participants bought gold in the past months and years for just these periods of geopolitical shock. When they happen, the safe haven is there to provide cash liquidity – by selling it.

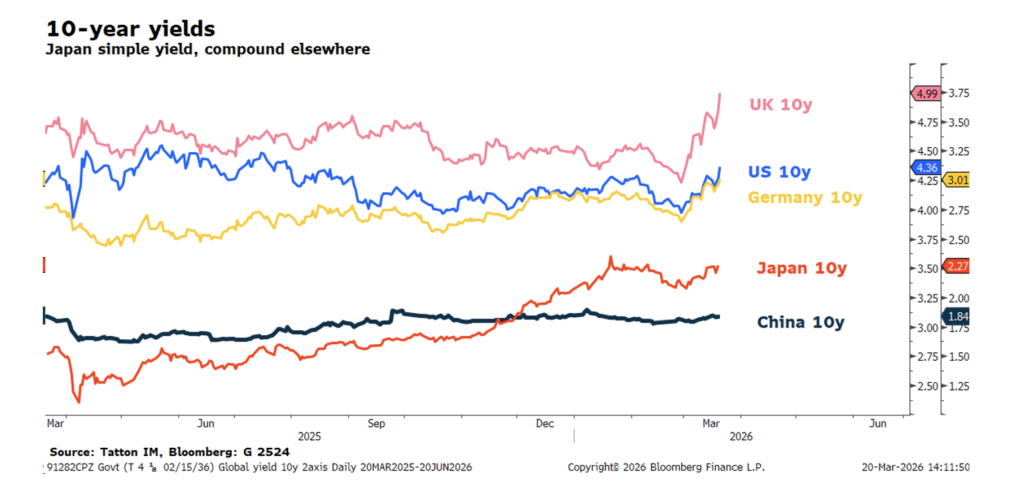

The bond market reaction has been understandable in some ways but perplexing in others. Government bond yields are rising to new highs – as you might in an inflation spike, but against what you would expect in a growth scare. The chart below shows the main 10-year government bond yields over the past year:

If investors were really worried about global growth, you would expect higher credit spreads (the difference between corporate and government bond yields), as private sector defaults become more likely. And yet, while US high-yield (non-investment grade) credit spreads are ending the week towards recent highs, they are not wider than last week. European credits have widened more, consistent with worries that European growth will be harder hit.

Nevertheless, credit markets were under pressure before the beginning of March. Some of the weaker holders (generally those that are more leveraged) seem to have been squeezed out ahead of the shock.

Central banks signal tighter policy, less liquidity

The war overshadowed some important central bank meetings. There were no interest rate changes from the Federal Reserve, the Bank of England (BoE) or the European Central Bank (ECB), but all issued inflation warnings about energy prices. The BoE’s committee voted unanimously to keep rates steady, and even talked about potentially raising them. But we suspect this messaging is more about managing inflation expectations than signalling future policy.

The BoE will have welcomed February’s labour market report. Wages are rising marginally, with little sign of a wage-price spiral. Unfortunately, the oil shock makes past data basically irrelevant.

The same is true in the US. February’s producer price inflation showed a surprising increase in the services sector, suggesting that, even before the war, the US economy was more inflationary than expected. The Fed’s dots plot (monetary policymakers’ rate expectations over the next few years) suggests one rate cut this year – just about – but its inflation forecast moved up. Chairman Powell is signalling that, since the Fed does not know what will happen with the war, the best he can do is project stability.

The risks have increased, and both near-term supply and demand have weakened. At the same time, central banks are not signalling any monetary accommodation – the opposite, in fact. That effectively means that short-term liquidity is being squeezed. Even if the geopolitical outlook improves, the liquidity squeeze alone will make things difficult for markets into the quarter-end.

However, the underlying global growth picture gives reasons to be hopeful for what comes after the shock. Despite the hits on energy infrastructure, the world’s potential energy production is not yet significantly impaired. Should that remain the case after this conflict passes, supply will resume while most regions will want to invest in closer (and probably renewable) energy sources. That could well reverse the current stagflationary dynamic from the war: more growth potential and less inflation risk – a hopeful outcome from a difficult situation.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.