Market Update: War disrupts energy markets

The Iran war has plunged markets into uncertainty with spot Brent crude oil above $105 per barrel (and having touched $120 pb) and European natural gas prices now more than doubled. European and Asian stocks have been hit harder than the US, and the dollar has risen – reversing recent trends.

Bonds are also under pressure, with the UK Gilt market especially impacted. UK 10-year yields have risen above 4.75% this morning and traders are now expecting that the Bank of England will raise rates this year rather than cutting.

Perhaps an oddity is that the US dollar is not higher by much, with the DXY index up only about 2% since the start of the conflict. Gold has also barely moved from last week’s levels. Investors may take some heart from this.

Korean stocks went on a wild ride, partly because East Asia is dependent on oil and gas imports, but also because of Korea’s popularity with speculative leveraged traders. Speculative positions are being shaken out – but overall the reaction wasn’t as bad as history would suggest. Maybe markets are desensitised to repeated shocks; the last oil and gas shock in 2022 didn’t destroy the world economy. Many suspect this won’t either.

Markets are no longer ignoring the risks. The ‘known unknowns’ are the war’s length, outcome and collateral damage. Inflation is projected higher everywhere, but economists’ projected growth impacts are mild and variable compared to the market’s fears. The US, a net oil exporter, could benefit while Europe and Asia suffer. That also depends on the end state: will it be regime shift (Venezuela), regime replacement (Iraq) or state collapse (Libya)? We suspect the attacks were opportunistic rather than geostrategic (i.e. starving China of oil) but that doesn’t mean things can’t escalate. Markets are focussed on oil and gas, but all sorts of trade ships through the Persian Gulf.

Ironically, war has distracted markets from previous worries (AI disruption, private credit, tariffs). The global economy has hummed in the background: growth indicators have improved for Europe, North America and Australasia, though China set its lowest growth target since 1991. China (and its trading partners) will at least benefit from the focus on demand. The UK spring statement barely registered, rapidly becoming irrelevant. Investors were ambivalent to economic data before the war, but business surveys were better than expected in the US and Europe. US employment came in weaker on Friday, but not because of AI.

If things calm, markets could easily turn positive, and investors that panic-sell often miss out on the broad recovery that follows.

Known unknowns return

The US and Israel’s war against Iran has plunged capital markets into uncertainty. No one knows how long it will last, what the endgame is or how much the global economy will be disrupted along the way. Markets are famously ignorant of human suffering but hate uncertainty. So, it is hardly a surprise to see some extreme price movements. But not knowing is not the same thing as fearing the worst. We started 2026 with expectations of stronger global growth and corporate earnings – and that should still be the focus for investors. We cannot downplay the risks from this conflict, but missing out on the next leg up would be a risk too.

Markets shake but don’t break

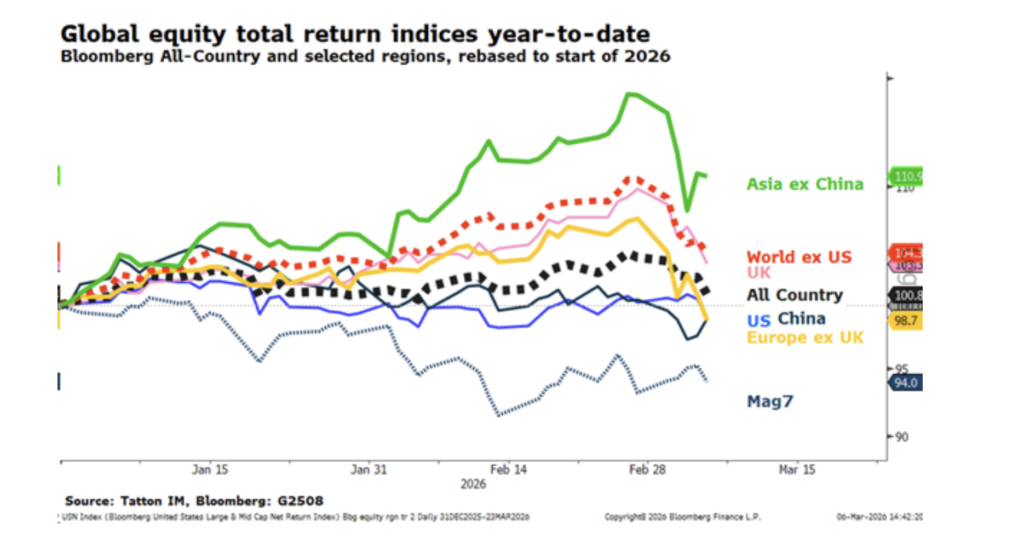

Markets were thrown out of alignment by the geopolitical events this week. European natural gas prices nearly doubled at the start of the week, reversing a year-long downward trend. European stocks were hit much harder than the US, after months of outperformance. The dollar spiked against global currencies, after sustained weakness. The biggest price action came in Korea: its stock market sold off around 20% on Monday and Tuesday, before recovering 12% on Thursday. Incredibly, Korea’s market is still up around 30% since the start of 2026.

East Asia is particularly at risk, due to its dependence on oil and gas imports. Korean volatility also shows how assets favoured by speculative leveraged traders (i.e. hedge funds) are the most vulnerable.

All things considered, the aggregate global equity market reaction was not as bad as historical precedent would have suggested. Europe and Asia came under the most pressure. The UK’s FTSE 100 held up a bit better, due to its high proportion of energy companies. The sell-off seems like a shake-out of speculative positions in the previously profitable “cyclical versus tech” trade (value versus growth). Investors worried about AI disruption may have bought the Magnificent Seven tech stocks (rediscovering their ‘quality growth’), which rose 2% in sterling terms.

Perhaps markets have, in general, become desensitised to repeated shocks. The last global oil and gas shock came in 2022, and it did not destroy the world economy. Oil and gas prices have not spiked as high as they did after Russia invaded Ukraine but, even if they do, plenty of investors would back the world economy to overcome them.

The war’s known unknowns

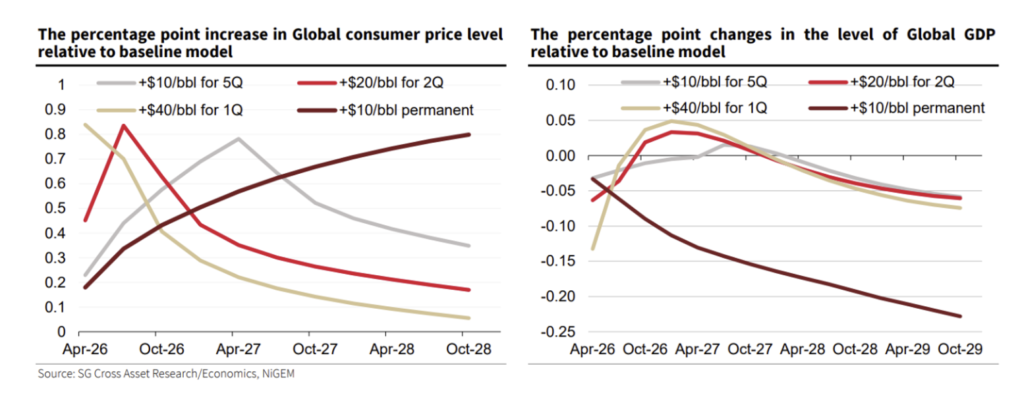

We do not think the risks should be ignored. There are ‘known unknowns’ about the length, outcome and collateral damage from the Iran war, the most obvious oil’s inflation impact. We write about that separately, but the chart below (from Societe Generale Economics and Cross Asset Research) shows some projections for global growth and inflation. They look at temporary rises over different periods, and a permanent (longer than four years) impact scenario:

Consumer prices are projected higher everywhere, but global growth is barely affected, falling initially, then reversing before settling at a lower trend. More importantly, growth will differ regionally. The US, now a net oil and gas exporter, might actually benefit, at least in the short-term. Asia is hit hardest, followed by Europe.

Investors worry about the short-term, but also about the possible end states. Is this a regime shift (like Venezuela), a regime replacement (like Iraq) or an future failed state (like Libya)? Trump seemingly prefers a short war. Judging by the apparent lack of military preparedness, he may have only wanted sabre-rattling in the first place. But wanting to keep it brief does not mean he will.

There is some suggestion that the Venezuela and Iran attacks are part of a broader hawkish strategy to starve China of energy supplies. We think that is unlikely (the US has offered to protect tankers through the Strait of Hormuz, more of which are bound for Asia than the US) but, again, that does not mean things cannot escalate in that direction.

Then there is the disruption along the way. Markets are understandably focussed on oil and gas, but all sorts of trade ships through the Persian Gulf. The world has only just recovered from years of supply chain problems – and now another shipping crisis could be upon us.

Markets are distracted but the economy keeps going

The irony is that the war has distracted markets from their other worries. Just last week, everyone was panicking about AI destroying the software industry and a potential run on private credit firms. Those themes have not gone away, but few are talking about them anymore. Neither are markets focussed on Trump trying to reimpose tariffs after the Supreme Court loss, when that could equally disrupt global supply chains.

In many respects, the world economy has been humming in the background. Until recently, 2026 growth indicators rose as high as 2% for the combined economies of Europe, North America and Australasia – up from 1.6% in 2025.

This week, at the National People’s Congress, China set a 4.5%-5% growth target for 2026. While this is the lowest target since 1991 (a recognition of its economic challenges), its population will benefit from Beijing re-emphasising domestic demand. This will also boost the rest of the world, particularly its near-neighbours in Asia.

In the UK, the chancellor’s spring statement barely registered as news – partly because it did not contain anything new, but mainly because it rapidly became irrelevant. Rachel Reeves spoke about lower inflation, lower debt and improving growth – and she was not wrong – but all of those are now in doubt.

Investors were ambivalent to economic data even before the war, but many components have improved. Business confidence surveys were better than expected in the US and Europe. US employment data was improving, but then February’s data, released today, strongly disappointed. The non-farm payroll dropped 92,000 thanks to the strike and weather, however, layoffs do not seem to be AI-related, judging by tech and service job data.

If things do calm down, markets could easily turn positive. Investors that sell out of short-term panic often miss out on the broad recovery that follows. In uncertain times, we always emphasise the importance of ‘time in the market’ over ‘timing the market’.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.