Market Update: Stock market consolidation for now

Markets have had another relatively quiet week. The news, on the other hand, was full of debt panic and more Trump destabilisation. As noted in the past few weeks, investors seem to have become desensitised to these events. The things traders typically care the most about – important updates to company earnings and interest rates – had more muted consequences than usual. When markets rallied earlier in the summer, commentators sometimes strained for an explanation. We now have plenty of explanations – but not much market movement that needs explaining.

Underlying this is a slight tightening of global liquidity. Liquidity has been abundant for a while, providing a strong incremental flow into risk assets. Due to seasonal and political factors (described below), it is currently levelling off. So, for equity markets to keep having ‘more buyers than sellers’, investors may need to sell other assets to generate the cash. They may well continue doing so, but will need a stronger incentive than is currently out there. In the meantime, markets are waiting for a refuel.

Take each ‘Nvidia day’ as it comes.

The release of Nvidia’s quarterly earnings data has, in recent years, been a big market mover. Investors were extra attentive ahead of the chipmaker’s Q2 report on Wednesday, as it was supposed to give some clues about how the AI investment boom is going. Nvidia’s share price dropped a little after the release – but wider US markets did not react much.

You would think that means Nvidia’s results were soft, but they definitely were not. The chipmaking giant slightly exceeded analysts’ quarterly earnings and revenue projections – which were already exceptionally high. It just did not project the same stellar growth rate as in the early days of the AI boom. There is a growing sense that Nvidia is finding a plateau, albeit a very high one – $54 billion in revenue for the current quarter!

The biggest tech companies have poured money into AI infrastructure over the last few years, and their stock prices have been handsomely rewarded. But if businesses invest money, they have less money to give shareholders. Investors have been happy to forgo that money today for the promise of growth tomorrow, but lately we sense that that might be changing. If so, that means more money toward share buybacks or dividends and less money for buying ever more AI microchips.

Even if that happens, it would not mean the AI theme is over. It just means that maybe not all of the AI spending will go to Nvidia. Indeed, Chinese producers are being directed to aggressively build their own competitor AI chips. This competition is a good thing; it is what the world economy needs in order to benefit from new technologies. Many companies have been paying to build their AI capabilities; shareholders will want to see the earnings growth next.

Policy risks aren’t upsetting markets too much.

Last week ended with excitement around the Federal Reserve potentially cutting interest rates, but market momentum fizzled out this week. There was some suggestion that policy risks are holding markets back – most notably president Trump’s attempt to seize control of the Fed. Some saw the sharp rise in long-term government bond yields as evidence of these risks.

In considering recent bond market moves we do not think they are a big cause for concern. On Trump, the worry is that replacing Fed governor Lisa Cook, along with the president’s previous and upcoming appointments, gives Trump allies a voting majority on the rate-setting committee. While we should not underplay the attack on Fed independence, it is not exactly true that Trump would have control over interest rates. Fed chair Powell was a Trump appointee after all. We suspect markets saw it this way too, judging by the dollar not falling any further.

The other major policy risk is the potential disintegration of France’s minority government – which could lead to higher public debt if either the left or right parties obtain power. French bond yields moved higher than other European yields in response, but the biggest risk for wider markets is that this creates another euro crisis.

Yet, the euro strengthened last week, suggesting markets do not see this as likely. France’s struggles have led to a loss of momentum for European assets, though. European stocks have outperformed this year, but the French fiscal challenge dampens that positivity.

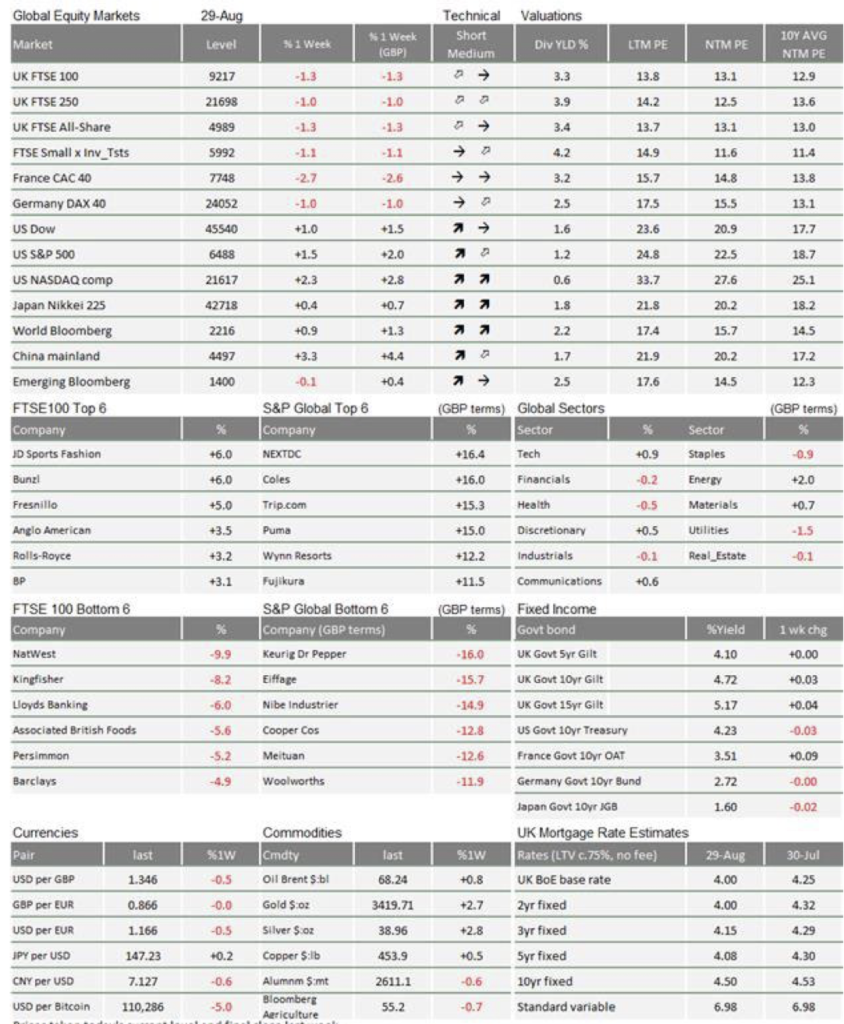

UK stocks fell last Friday, courtesy of a sell-off in banks. The rumour of a tax raid has made NatWest, Lloyds and Barclays (all large members of the FTSE 100) the week’s worst performers. The treasury is floating various ideas (two weeks ago it was the property tax idea) while encouraging talk of a big black hole in finances (now up to £40bn per year).

The loss of momentum is a loss of liquidity.

Stock markets are fizzling out everywhere. Part of this is the fact that government bonds now offer decent returns, so it is just that little bit harder to make the case for buying equities. Relatedly, as mentioned at the beginning, it looks like the strong liquidity that had propelled markets is levelling off.

For the last few months, the US government has been running down its Treasury General Account (TGA) – essentially spending its buffer of temporary savings as it approached its notorious debt ceiling. That meant the US treasury was injecting money into the financial system. But now, the TGA balance is building back up – ‘parking’ liquidity at the Fed, while the Fed itself is downward adjusting some of the policies that also added liquidity to the system. Overall liquidity is not tight; it just is not as loose as it was.

With less cash flowing in, in aggregate, investors now have to sell assets to buy stocks – which requires a stronger appetite for risk. But risk appetite is already strong, so for it strengthen further, markets need something else to get excited about. Nvidia’s results might have been enough to propel stocks a few months ago, but now investors need a new catalyst. That may well come, judging by recent improvements to global growth expectations. But it has not come yet.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.