Market Update: Bonfire but no rockets

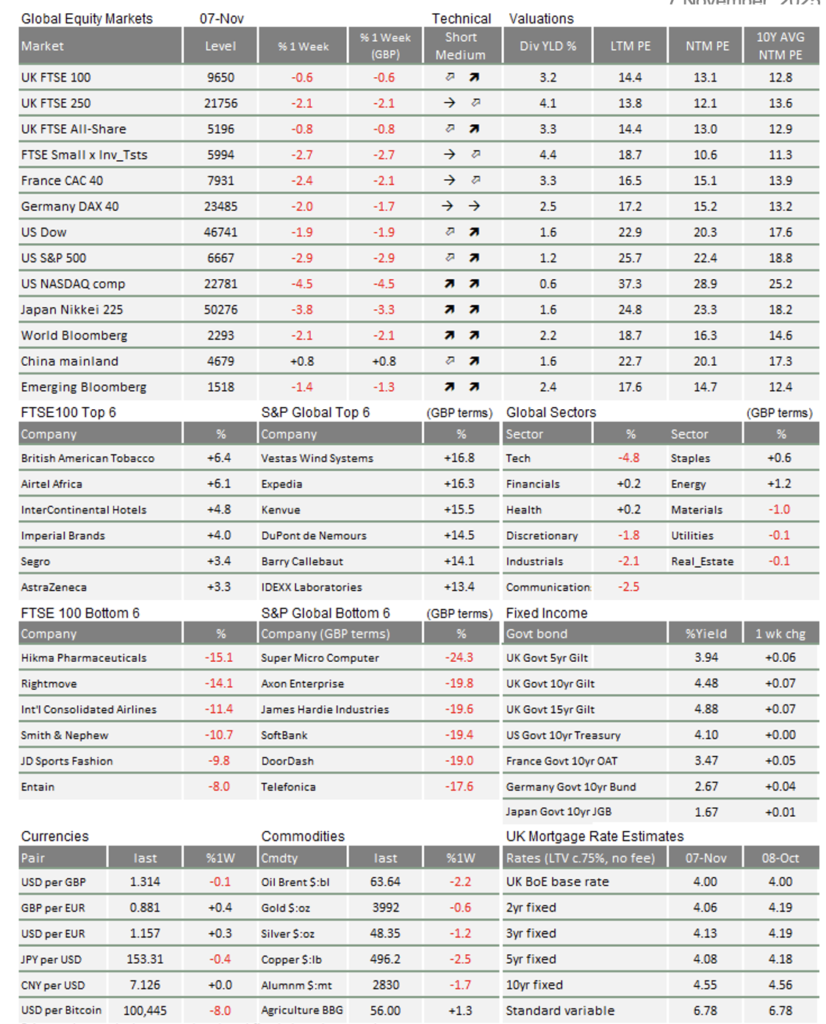

After a pleasingly strong October, it was a tough first week of November in capital markets. Stocks sold off 2-3% virtually everywhere, and the biggest tech stocks were particularly vulnerable. Media commentary put this down to valuation vertigo – investors doubting whether future corporate earnings can live up to the promise of high price-to-earnings stock valuations. That is not quite how we see it, given there was no real new information about the shape of the global economy last week. The only change we observed was the steady deterioration of market liquidity. We keep saying it, but the drying up of liquidity means bumpier markets. It does not mean worse long-term returns, though – far from it.

Weaker sterling underpins UK markets

In the run up to the November Bank of England meeting, we said that markets were underesti-mating the chances of a November interest rate cut from the Bank of England (BoE). The Monetary Policy Committee’s (MPC) voted 5-4 to keep rates steady last week, much closer than expected. Barring a fiscal loosening in the treasury’s autumn budget or a remarkable resurgence in economic activity (we expect neither), the BoE will cut rates in December. There is an outside chance that the rate setters on the MPC could even vote for another cut in February.

Rachel Reeves’ Tuesday pre-budget briefing was a big departure from previous budget protocols and has been followed by Friday’s leak of income tax rises of 2% in each band. And yet, unlike other major markets, UK stocks held up fairly well (at least until Friday). Government bond yields fell too. This is partly down to a weaker sterling last week, which makes our markets more attractive to international investors and our large caps’ overseas earnings more valuable. Sterling softness will also help British exporters. Previously, our currency had gained against global peers for most of 2025, which sounds like a good thing but can weigh on domestic producers. For UK investors, meanwhile, sterling’s fall this week also took the edge off foreign equity weakness.

UK government bonds (gilts) are also being supported. Last week, a renowned US bond manager told us how sterling bonds were their main non-US holding, a remarkable thing given that, in our previous meetings, they told us that the UK bond market was probably too small to consider. The Chancellor’s (likely) fiscal discipline is gaining fans and stands in contrast to the US and France.

Across the channel, European economic data has been lacklustre. Industrial production numbers from Germany have disappointed, which we discuss in more detail in a separate article. On the plus side, Eurozone loan demand is improving. We have spoken much about US liquidity being hampered by the Federal Reserve in recent weeks, but it is worth noting that the European Central Bank is not constraining liquidity to the same extent. That helps the Eurozone outlook.

It’s only a bit about the economy

US stocks struggled, particularly the large cap tech companies. The financial media put this down to fears over stretched equity valuations, and whether big tech will be able to deliver enough profit growth to back them up. This narrative follows on from underperformance of US small cap stocks last week, and the worries about growth in the world’s largest economy. The US government shutdown – now officially the longest in history – is clearly biting. Employment statistics from non-governmental providers Challenger, Gray and Christmas, released on Thursday, point to a surge in layoffs.

We should be careful about this narrative. Not much US economic data has been released recently, thanks to the government shutdown itself, and the data that has been released is mixed overall, rather than bad. The Challenger Gray job loss estimates were high, especially given that this is usually a season of hiring, not firing. On the other hand, ADP reported stronger private sector hiring than expected for October.

In any case, big tech stocks are not that sensitive to short-term US growth. The AI investment theme that has boosted tech valuations is not supposed to be cyclical. And while many have fretted over an ‘AI bubble’, recent corporate earnings reports show that the theme still has room to run.

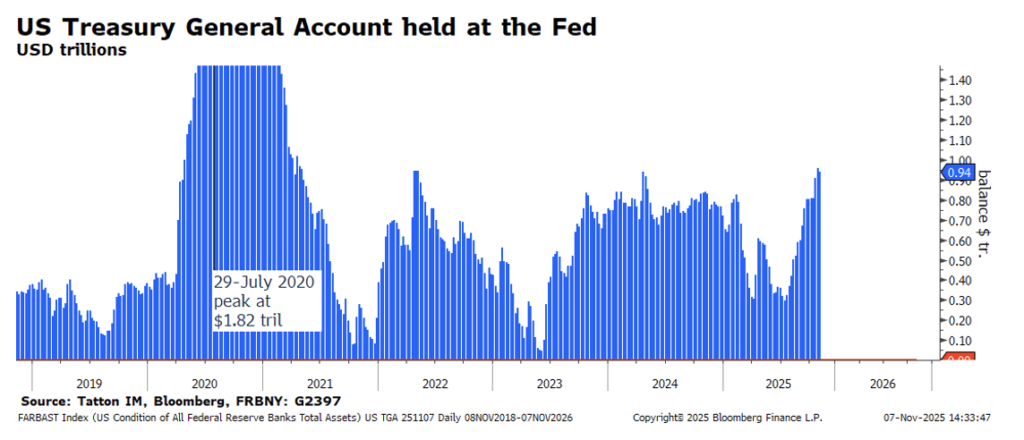

We do think last week’s sell-off is related to the government shutdown, but not because of valuations. The shutdown has halted federal payments, which means money collected by the treasury goes straight into the government’s ‘piggybank’ the Treasury General Account (TGA), see chart below. The TGA balance can have a big effect on liquidity conditions; more money in the TGA means less money in the financial system. Tighter liquidity means fewer asset buyers, and hence more volatile markets.

When government opens, investors will probably return with their cash

To be clear, we are not saying that investors do not have legitimate concerns about tech valuations. But markets’ current anxiety is more about whether there are enough buyers around in the short-term, and not about whether long-term profits will be good enough.

Investors are selling down their equity positions (and other speculative assets, like cryptocurrency) because they need cash. This phenomenon is concentrated on the US, but the effects spread all over the world, thanks to global financial links. Japan’s Nikkei 225 also sold off sharply this week, after impressive returns in October.

Amid these market jitters, we should remember that the long-term investment outlook is solid. Global growth seems to be improving, and corporate profits have stayed strong virtually everywhere. If you are bullish about long-term growth and markets drop back, that suggests there is a buying opportunity. Investors probably will not feel that way until the US government shutdown ends, but once that happens – and the TGA balance starts flowing out again – we expect there will be more buyers than sellers again.

All of that leaves us in the same position we have been for weeks: current volatility is a bumpy ride to a good destination.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.