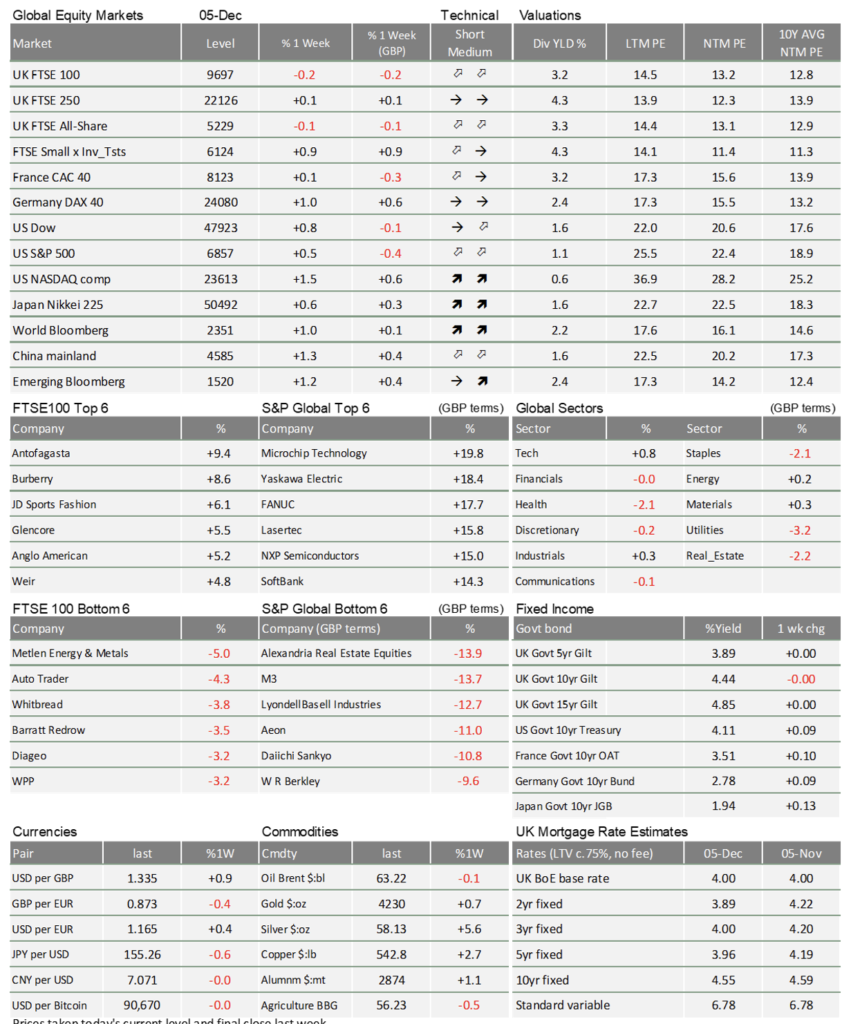

Market Update: Next stop, Santa Rally?

Capital markets felt a little better in recent weeks, but with emphasis on “a little”. Global stocks gained incrementally through last week, putting most of the November market downdraft behind them. Underlying these moves is a genuine improvement in the economic outlook for next year. Interest rates are now certain to fall again and, even though there have been doubts over US and global growth momentum, corporate earnings have proven resilient.

All the conditions seem to be in place for a Santa rally to close 2025, but we are not seeing it yet. Fortunately, considering how strong investment returns have been since April, we do not really need one this year.

The Fed will cut, but will it regret it?

We have seen quite the turnaround in markets’ expectations for the US Federal Reserve (the Fed). Two weeks ago, bond traders saw less than half a chance of a December interest rate cut. Now it is a near certainty, confirmed by ADP’s weaker US employment figures from November. The US shed 32,000 private sector jobs last month, versus an expected 10,000 gain, but because the Fed set a December cut in stone, equity markets took the news well.

However, it was interesting to hear Former Fed governor Rob Kaplan, now vice chairman at Goldman Sachs, argue that another Fed cut should not come before January. Kaplan’s point was that it is better to be a little late than wrong. Delaying a cut might turn out to be a tactical error that weakens employment, but that can be rectified by a catch-up cut next month. However, if the Fed cuts now and finds in January that the US labour market is tighter than it thought, it risks embedding higher inflation for a sustained period.

A deceptively tight jobs market is certainly possible, given the administration’s deportation drive and lack of skilled construction and engineering labour. Indeed, data released on Thursday showed initial jobless claims well below expectations, suggesting the opposite of the ADP figures.

The Fed is struggling with both internal and external division. Trump appointee and perennial dove (preferring lower rates) Stephen Miran has reportedly lost influence on the rate-setting committee by repeating arguments the other members consider settled. But that could change, depending on who Trump appoints as Fed chair next year (bond investors told US Treasury officials they are “concerned” about Kevin Hassett’s potential appointment, according to the Financial Times).

Externally, the US economy itself is split between good fortunes for big tech and owners of financial assets, and tougher times for the rest. Notably, ADP’s reported job losses were concentrated among smaller businesses. This “K-shaped economy” has become a hot topic for investors, so we dedicate a separate article to it.

Santa Rally is missing its elves – private investors don’t yet feel festive

Those doubts aside, rate cuts improve an equity market outlook which is already decent. Companies are starting to revise up their earnings forecasts at a stronger rate – with small and mid-cap US stocks improving particularly well. That went hand in hand with an outperformance of smaller US stock indices last week. It is too early to tell, but that could be the green shoots of the market rotation – away from mega tech toward the lesser loved names – that we suggested last week.

Investors are still concerned about equity valuations, and certain metrics (like price to sales) do show that global stocks are historically expensive – even more so outside the US, in fact. But historical valuation averages are not always a good guide to where prices should go next, particularly after years of upward trend.

Fundamentals look good and markets recovered somewhat last week, but retail investors are still not stepping in to ‘buy the dip’ like they used to. There is feeling that, after three years of strong returns, the party must surely be coming to an end.

The sharp sell-off in cryptocurrencies – the year’s other darling asset of retail investors – might be an underrated part of this. Cryptos have a significant wealth and liquidity effect on a particular cohort of (usually) private retail investors, which this year have often also been the marginal buyers of equity. Traditional institutional investors sometimes feel a bit of Schadenfreude when cryptos sell-off, because they doubt their fundamental asset value and long for healthy corrections. But even if that is right, billions in value being wiped out will inevitably have knock-on effects on global stocks.

2025 doesn’t need a Santa rally

Plenty of UK investors seem to be in that nervous bracket. Many moved some of their investments into cash ahead of last week’s autumn budget, for fear of wealth taxes and the like. We need to see that private investor capital coming back, but it has not happened yet. It seems that the negative public reception of the budget has Britons still concerned.

However valid those feelings may be on a personal level, they are at odds with the positive market reaction to the budget. International bond investors ultimately saw it as a sign of a prudent borrower and therefore win for bond stability. UK bond yields this week remained below their pre-budget levels, and stocks are holding up decently. UK retail stockbrokers anecdotally voiced concerns, that UK investors sitting in cash risk missing out on the next leg up in markets – not just for UK assets, but globally.

We said last week that all the ingredients for a Santa rally are here, and that only seems more true now. For whatever reason, it is not happening. The heartening thing for investors is that, after such a strong run, it is not needed. 2025’s returns will look strong overall and provide a decent starting position for 2026.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.