Market Update: Reasons to believe

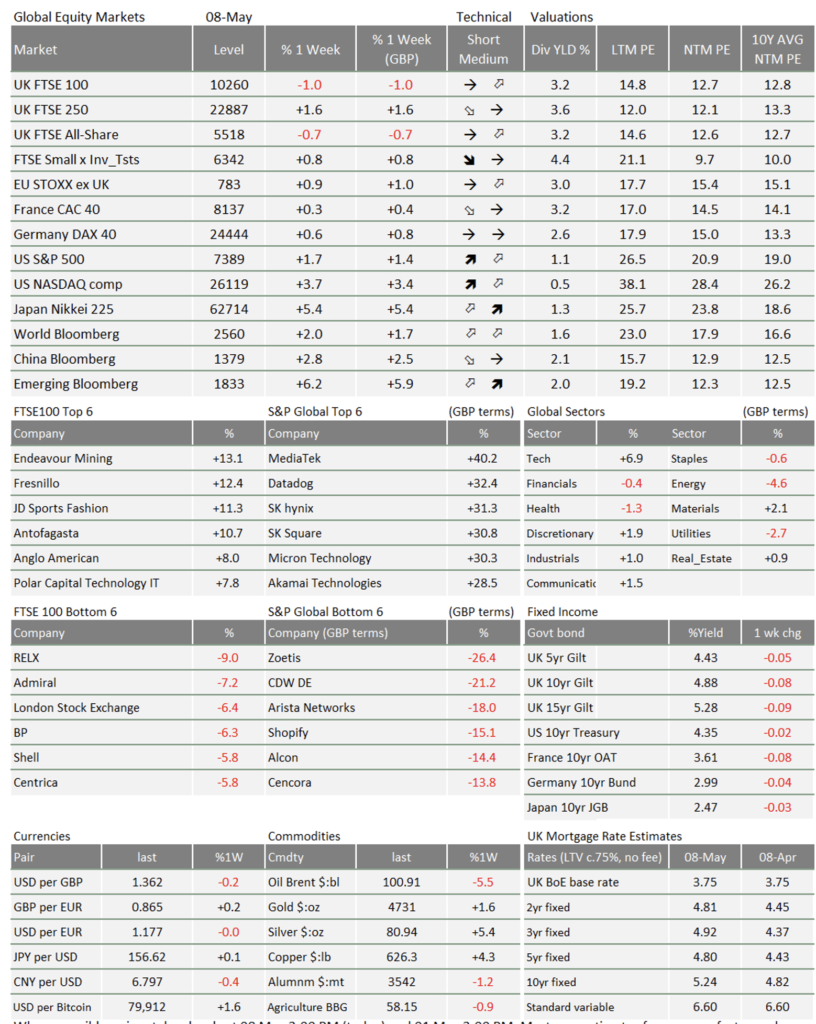

Markets are feeling hopeful. Iran is still mulling over Donald Trump’s proposal to end the war and reopen the Strait of Hormuz, but investors are betting on a done deal. Oil prices dropped from around $115 per barrel [pb] on Monday to below $100pb. Stock prices took another leg up – helped by strong corporate earnings and some decent economic data. In local currency terms, US equities continue to outperform, but a weaker dollar makes their weekly performance look much more in line with other markets.

Is it really over?

Operation Epic Fury is over, according to US Secretary of State Marco Rubio, apparently having achieved all of its objectives. Given that “Project Freedom” (in which the US Navy would escort ships through the Strait of Hormuz) lasted one day, we are left to guess what the goals were.

However, it is probable that peace talks will have been successfully concluded in time for President Trump’s visit to China late this week. China seems to be pushing its Iranian ally to accept a deal that will resume oil and gas shipments through the Persian Gulf, in exchange for US sanctions relief. Tellingly, Iran’s foreign minister was in Beijing last week to talk about “regional and international developments”.

By now, we should know better than to declare the Middle East crisis over, but what we can say is that the risks look less risky than a week ago. The world will need to rebuild its depleted fuel reserves, so oil prices are unlikely to fall rapidly, regardless of what happens in the next couple of weeks. But the medium-to-long-term outlook for global energy markets has tipped back towards oversupply. The UAE’s exit from OPEC – and likely increase in oil production – backs that up. So does the sharp fall in Shell’s share price last week, in spite of stellar profits.

If the Iran saga really is ending, what next for the Trump show? The president’s apparent détente with China could presage another episode of tariff aggression towards Europe. The EU signed a trade deal with the US last year, but Brussels has pursued a policy of “strategic under-implementation” since, according to trade expert Sam Lowe. European policymakers have not yet removed the tariffs they promised – though neither has the US, they might argue. Trump, visibly affronted by Europe’s refusal to join his war, will be looking for a reason to hit back at Brussels.

Nevertheless, tariffs are not an easy win for Trump. US consumer inflation expectations may not have shifted much higher in the past six weeks, but his policies have done nothing to lower general prices. So, there is reason to believe that a warming of relations with Xi could mean lower tariffs with China at the same time as Trump hits Europe.

Resilient US economy isn’t helping the dollar

Throughout the Iran war, global growth has been much more resilient than expected. The purchasing managers’ indices (PMIs – measuring business confidence) were revised upwards for April, from already strong levels. It is not only the US looking bright (UK PMIs were also surprisingly strong) but it is especially the US. American consumers are buoyant.

Today’s US employment data indicates that, for most people, there is no reason to be fearful about redundancies. The jobs market added 115,000 in April and is growing again after a winter hiatus, while there is little sign of significant AI-related impacts. Hourly wages are showing less strength, growing only slowly at +3.6% year-on-year, which is only just above inflation; that allowed bond yields to remain stable rather than rise, a good combination for the equity markets.

This is feeding through into a phenomenal increase in corporate earnings. There has been much discussion about market concentration – with big tech leaving other companies in the dust. That is true for the S&P 500, but small and mid-cap indices are actually showing strong earnings growth too.

With lower risks and continued US equity outperformance, it is a little surprising that the dollar has resumed its decline. We have written before about how the fragmentation of global trade means more investment required outside of the US – dragging the dollar down. The global reserve currency’s soft patch last week could be a sign that dollar decline is now the default trend.

Incoming new Fed chair Warsh is a peculiar species of dove

Equity price-to-earnings valuations have cheapened since the start of 2026, and global growth has become stronger. If you did not know there was a war going on, you would think that is a pretty strong environment for stock markets. It helps that government bond yields fell back from their highs last week too (improving stocks’ relative attractiveness by comparison).

The yield fall was particularly strong in the UK, but we would avoid any political explanations. When UK bond (gilt) yields rose the week before last, we said it was more about the gilt market’s structural imbalance than political drama. The same goes for last week: inflation expectations fell, so highly inflation-sensitive gilts fell too.

Signals of tightening monetary policy detract slightly from the global equity outlook. But, if the Middle East crisis does indeed calm, we might expect central banks to loosen once more. The Federal Reserve already looks set to cut interest rates under new chair Kevin Warsh, even though the US economy does not need much help.

With strong US growth, the only way for Warsh to square the circle on rate cuts is to reduce the Fed’s balance sheet of government bonds. He has argued exactly that for years – that the Fed should wean capital markets off central bank bond purchases. Many are sympathetic to Warsh’s view, but it will mean a reduction in the liquidity that has buoyed markets for nearly two decades.

The Fed is not a dictatorship (to Trump’s chagrin), so Warsh will have to convince his committee colleagues – including outgoing chair Powell – of his low-rates, lighter-balance-sheet plan. Liquidity reduction will therefore be slow, if it happens at all. That is good news for markets; too fast, too soon could be painful. The Fed’s brave new world is tomorrow’s problem. Today, markets have found reasons to believe in the reasons to believe.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.