Market Update: Resilient equity markets, rising risks

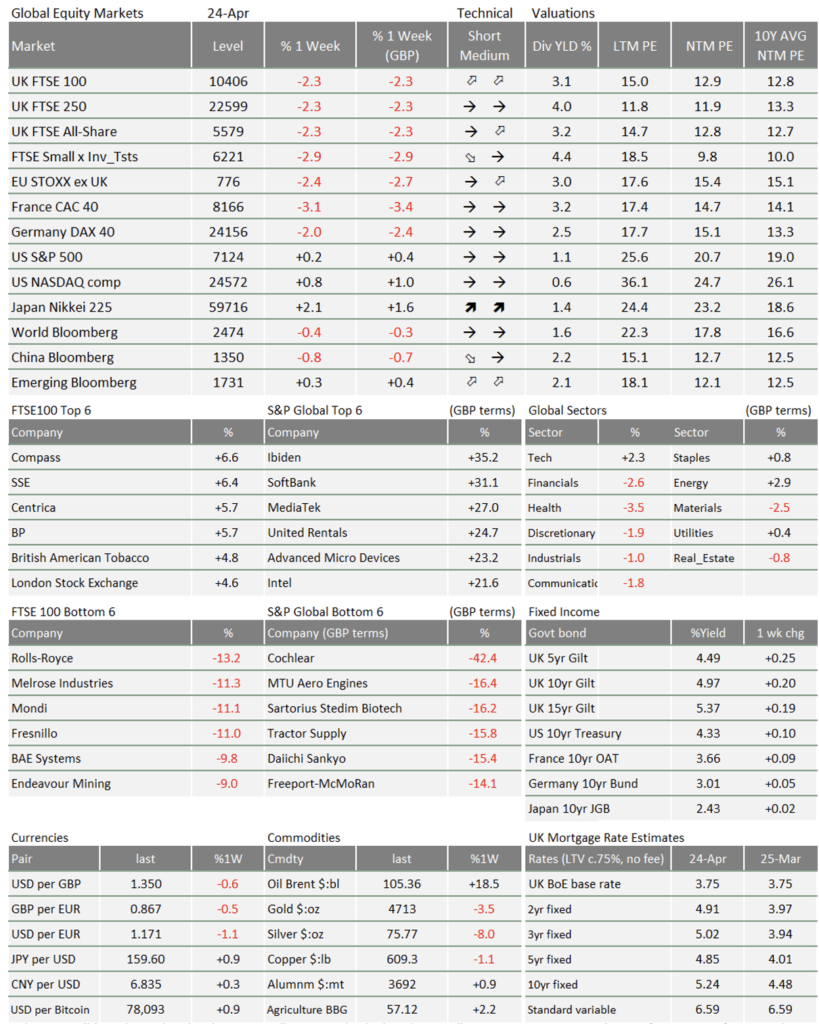

Risks have risen compared to a week ago, but global stocks are little changed. The Middle East conflict has simmered down into a tense stalemate, with ongoing dialogue but little progress. Global equity indices are in a holding pattern, although US stocks have now outperformed for two weeks. It is an uneasy calm, with oil prices and government bond yields rising back up.

The good news is that the latest economic data covers the period since the start of the Iran war, and they show a relatively resilient global economy. Markets will struggle to get excited without tangible progress toward resolving the oil shock, but underlying growth fundamentals are strong.

Risks creep higher

The ceasefire between the US and Iran has nominally been extended, but the US continues to blockade the Strait of Hormuz and the Islamic Revolutionary Guard Corps [IRGC] is still seizing or attacking ships in the waterway. With a flurry of military activity in the Persian Gulf, it is hard to work out what the current state of play is, let alone what might happen next.

Whether things escalate from here depends on how Tehran responds. If President Trump is right about “infighting” among the Iranian leadership, it could be a while before negotiations can make any real progress. Iranian politicians, of course, deny any internal power struggle, but it seems pretty clear that the war has made the regime less stable.

That does not necessarily mean there will be a regime change (depending on what you class as a change) and it could result in the IRGC being politically strengthened. US network NBC reports today that some Western diplomatic sources believe they are becoming more stable and hardline. Already uncertain outcomes for Iran’s regime are now even less predictable.

In the meantime, oil prices have risen steadily through the week, with a slight respite today. This is the first week since the end of March that Brent Crude has finished trading higher than where it started. That reflects the fact that, for all the talk of ceasefire, the current stalemate is not sustainable for the world economy – and particularly unsustainable for other Gulf states. Time is not on our side, and the risk to equities creeps higher the longer things stay like this.

Growth expectations push up rate expectations

Another risk factor for stocks is the move up in government bond yields, making them less attractive by comparison. The biggest yield moves this week came in short-term bonds, reflecting higher interest rate expectations. That is not just about energy prices: the latest economic data show that businesses and consumers are more resilient than we might have thought. Global growth looks surprisingly strong despite the oil shock – lessening the need for rate cuts. We cover April’s business sentiment surveys in a separate article.

The UK is a case in point. Much of the focus right now is on sharply higher input costs, skirting over the fact that business and consumer confidence is holding up well (although there is a larger-than-usual discrepancy between similar measures). The Bank of England will take note and probably change its somewhat dovish rhetoric (preferring lower rates) in the coming weeks. But this is not the dreaded ‘stagflation’ of high inflation and low growth. Far from it, some elements of inflation may have moved up because growth looks stronger.

Since the war broke out, we have been relatively positive on long-term bonds – as some of the reaction seemed a little overdone or inconsistent. The latest data is a challenge for our view and for bond prices (the inverse of yields), but the challenge comes from better growth fundamentals, rather than higher fiscal risks. If that is right, it should still mean a decent outcome for equities.

Déjà vu of muddling through

Strong business sentiment data is also backed up by the continued improvement in corporate earnings growth. We already knew that was the case for US companies, but this week we have seen a surprising pickup in European earnings growth too. That does not match up with the narrative around Europe’s energy vulnerabilities, or the fact that European sentiment data is by far the weakest of the bunch. Business confidence numbers are not great, and today’s German IFO business survey was the weakest since the 2020 pandemic collapse.

Earnings results are backwards looking, so we would probably view negative sentiment data as a slightly more accurate guide – but we will watch European earnings closely for more clues.

On a global level, most of the signals suggest that things are not quite as bad as feared. This puts markets more or less back to where they were last summer. Trump’s back-and-forth over tariffs led to some panic and plenty of recession predictions a year ago but, in the end, global corporate earnings growth kept ticking along.

Some of the other risks are receding too. Kevin Warsh is now certain to become the Federal Reserve Board Chairman after Trump and the Department of Justice dropped the questionable probe into Jerome Powell. While always a likelihood, the news has helped US bond yields to fall slightly. Earlier in the week, during the Senate Confirmation hearing, Warsh dismissed any claims he would take monetary policy cues from the president. He could hardly say anything else, but his testimony still helped bolster his reputation with markets as a fairly orthodox candidate, not just by Trump’s standards.

The president has a habit of making big announcements when markets are shut for the weekend – so if everyone is worried about something else come Monday, we should not be surprised. Fortunately, recent history shows that markets and the economy are capable of ignoring the noise and keeping their pace.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.