Market Update: Markets hold their breath

Donald Trump’s apparent olive branch to Iran helped to temporarily stabilise markets last week. Stock prices gained a little in the early part of the week, government bond yields fell back from recent highs, and energy prices dropped back from last Friday’s peak. None of these moves were that big, however, and, more importantly, all were brief.

Markets had a bit of relief, but only a bit. Trump announced on Thursday night that he would extend today’s deadline, but Israel has said it will escalate its attacks. There is a chasm between the opposing sides and uncertainty about each side’s demands. We seem to be in a holding pattern of sorts. There is a reasonable chance that we do see genuine de-escalation but, the longer we carry on like this, the worse the global growth impact.

Boundary setting isn’t de-escalation

The ultimatum Washington issued last weekend – for Iran to reopen the Strait of Hormuz or see its energy infrastructure destroyed – was postponed on Monday. Buyers of the TACO trade (Trump Always Chickens Out) will not be surprised. Both the US and Iran tested the boundaries of what the other might consider acceptable last week (i.e. not damaging long-term Middle Eastern oil and gas production). The threats continue, but the fact both backed away confirmed, for markets, that the boundary exists.

That relieved bond and equity investors, confirming that escalation is not endless. Escalation is also limited by the fact that President Trump’s 15-point “action list” for Iran, submitted through mediators in Pakistan, supposedly does not include demands for full regime change.

But a lack of escalation is not, in itself, de-escalation. Washington submits a peace plan with one hand, and sends an extra 1,000 troops to the Middle East with the other. Even if this is just to establish a credible threat, Tehran clearly does not believe that Trump’s peace plan is genuine. Neither, seemingly, do betting markets: Polymarket’s odds of a ceasefire before the end of April are still below 50%. If this is a TACO, it is a soggy one.

In the meantime, oil and gas exports are still held up in the Strait of Hormuz. The relative pricing of oil and natural gas futures contracts implies a resumption of supply and within a timescale that does not empty the world’s reserves. But, if the blockade continues, energy prices would climb higher and the medium-term global growth outlook would fall further.

From inflation pricing to degrowth pricing

We had the first release of economic data since the war started this week, in the form of Purchasing Manager Indices (PMIs – measuring business confidence). They largely confirmed what everyone had been expecting: business sentiment has been less bruised in US than in Europe and Asia. That is all about the impact on energy prices, particularly natural gas.

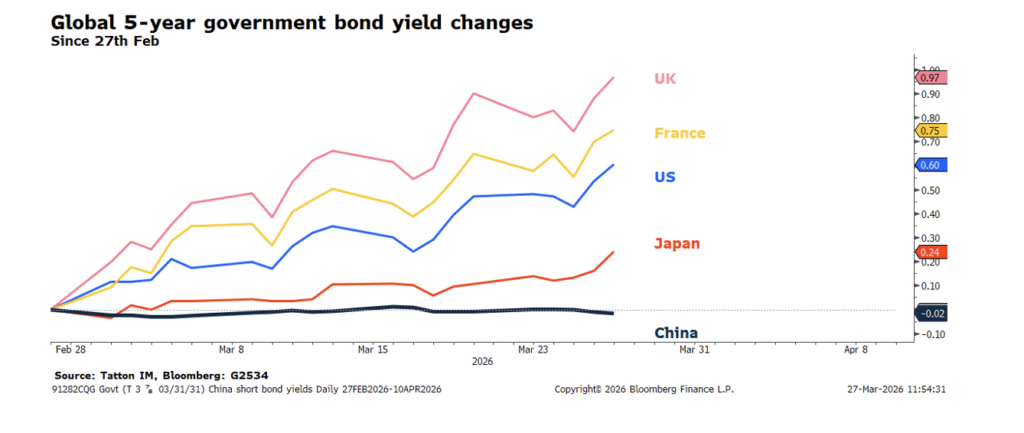

That suggests lower medium-term growth, which, all else being equal, should mean lower government bond yields (as they are supposed to reflect the background rate of economic expansion). That logic is why bond prices (the inverse of yields) are a good investment counterweight to equities – but the opposite has happened this time. The only bond market that is offering any offset against stock losses is China. Below is a chart of the change in five-year government bond yields:

That is because, in China, the oil shock is seen less as an inflation risk and more as a growth dampener. The lesson from China’s bond market is that supply shocks are not all about inflation. For US, European and – particularly – UK bonds, the impact on implied inflation expectations has been substantial. Indeed, the move up in bonds’ inflation component has been much higher than the one implied by oil futures. Meanwhile, relative growth expectations, measured by real (inflation-adjusted) yields, has been relatively small.

That could change. Central banks across the developed world sounded the inflation alarm the previous week, but their communications last week were noticeably more growth-focussed. If the war drags on and keeps looking like a global macroeconomic hit, long-term government bond yields could therefore fall.

Liquidity squeeze loosens but brace for next week

The result of central banks signalling tighter monetary policy last week was a tightening of financial market liquidity. That contributed to higher market volatility. In contrast, last week’s slightly easier messaging has loosened the liquidity squeeze. That was another key reason for the slight rebound in stock prices.

We see this relief in gold prices too – which had a torrid previous week, but stabilised a little last week. In general, holders of speculative assets are under less pressure. That is true even for the ailing private credit sector, and, notably, there is no sign of a knock-on effect from recent private credit fund closures to publicly traded bonds.

This is good news, but it might change this week, if only for technical reasons. This week is the end of the quarter, end of the financial year, and a long Easter weekend to boot. Those are usually times when trading is light, meaning less short-term liquidity. Small selling pressures can be amplified in such circumstances, so this week could be a little nervy. If that does happen, however, it will likely be a short-term technical blip, rather than a sign of a broader momentum shift. That is, of course, not taking into account what happens with the war. For now, markets are in stasis.

![]()

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.