Market Update: It takes two to TACO

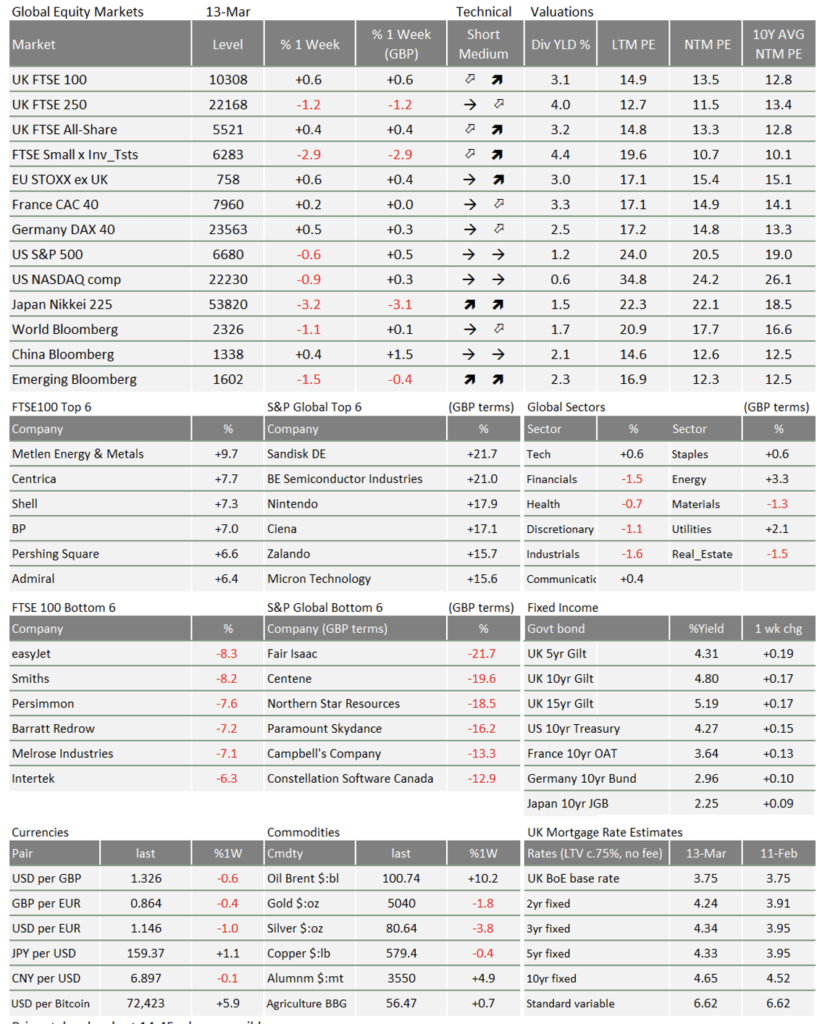

Stock markets pulled back over the last couple of days, as oil prices rose to around $100 per barrel (pb). Before that, equities had been holding up okay, particularly large cap stocks. Sterling has slipped about 0.5% against the US Dollar which has helped to offset some equity weakness, meaning global equity portfolios are only slightly lower. Bonds continue to be surprisingly weak, especially in the UK. The 15-year UK government bond now yields 5.16% (0.5% more than before the war).

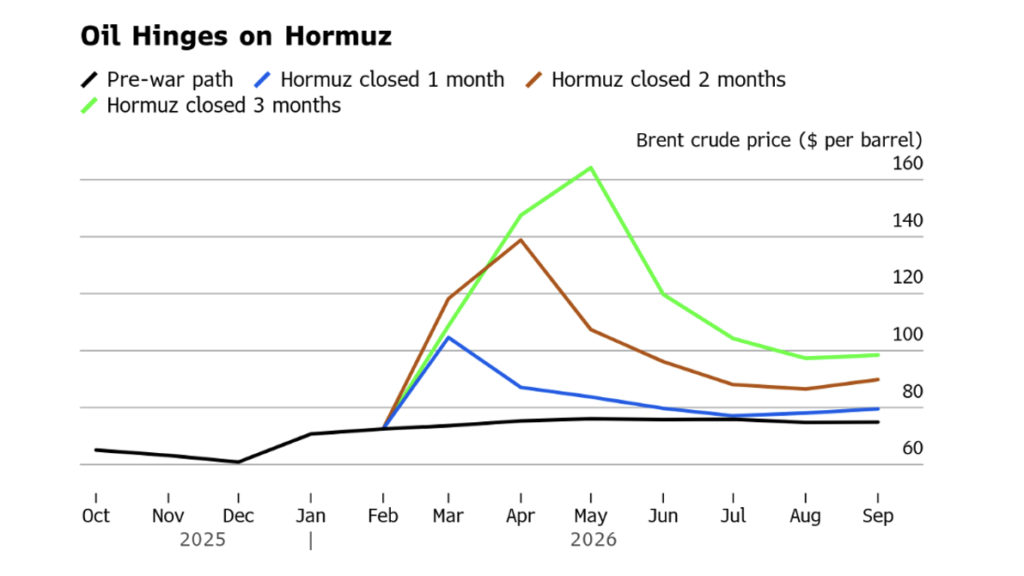

The Iran War has sent global oil prices on a wild ride over the course of last week – which we cover a separate article – but markets seem to be betting on a relatively swift end to the conflict, after which crude prices should settle back to a manageable $75-$85pb range. The ‘swift’ part here might be a little optimistic.

It takes two to TACO

Stock indices are below where they were last Friday but, compared to the dramatic escalation in the US and Israel’s war on Iran, markets still look sanguine. Investors have flocked more toward large cap tech stocks – reversing the cyclical rotation into small cap stocks we have seen so far this year. You could perhaps interpret that as a move into ‘safe haven’ quality stocks (though see below).

There was a sharp increase in long-term government bond yields across the world, meaning bond prices fell. Higher ‘risk-free’ government bond yields should make risk assets like equities less attractive by comparison, but there was no big fall in stock prices. That effectively means that the bond-adjusted equity risk premium has gone down. In other words, remarkably, investors see stocks as less risky, compared to bonds, than a week ago.

That can only make sense if you believe in the TACO trade (Trump Always Chickens Out). Undoubtedly, the Trump administration has an incentive to end the war soon: $100pb oil heading into November’s midterm elections is not a vote winner. Judging by Trump’s declaration of the war as “pretty much” over, he agrees. Perhaps he is already bored of his latest adventure, which lacks the immediate operational success of Venezuela.

But while we certainly see the incentive, we suspect markets might be overestimating Washington’s ability to end hostilities quickly. Iran clearly still has the capability and motivation to attack US and Israeli sites in the Middle East. There might not be an easy out for Washington. If that is right, the comparatively content view in stock markets makes equities vulnerable to a drawn out conflict.

The cyclical rotation was already vulnerable

In the US, among the worst faring stocks have been private credit companies, after a cascade of retail-focussed private credit funds halted redemptions (they stopped retail investors getting their money back), and analysts sounded warnings about private credit loan defaults. In a separate article, we write about why private credit woes are not 2008 all over again. It is still a bad situation of course, and the Iran War makes it worse.

The war is bad news for housebuilders. UK constructors have had an especially difficult week. So did smaller companies everywhere, which are more sensitive to interest rates staying higher-for-longer. Small-cap stocks had been doing well in 2026 but, even before the war, the data showed small-cap earnings growth starting to flounder, relative to large-cap companies. Cracks were already appearing in the small-cap cyclical rotation. The war split them open.

Earnings growth for large cap stocks has looked better, backing up the strong growth expectations markets had at the start of the year. But existing problems around private credit, small-cap struggles and looming AI displacement make investors nervous. If the war drags on for another few weeks, there is a danger that these anxieties bubble over.

Markets need lower bond yields and bonds need lower oil

The key to all of this is what happens in government bond yields: if bond markets relax and yields come back down, global investors will feel more at ease. It is slightly odd that long-term government bonds should be so sensitive to short-term volatility in oil prices. The standard explanation is that the oil shock increases long-term inflation expectations and hence interest rates – as one official at the European Central Bank (ECB) suggested last week.

We think that the ECB comments are more about managing inflation expectations, however. If central banks really expected a repeat of the pandemic’s inflation spiral, they could enact emergency rate hikes – not just talk about them.

Instead, we suspect that rapidly rising bond yields are about an increase in the risks attached to government bonds. The oil shock, if it persists, could force governments around the world to spend more on social support and defence. That worsens public debt metrics which are already bad amongst G7 nations – making bonds less attractive. Unhelpfully, the UK looks particularly vulnerable.

Over the last few decades, global government debt has increased relative to private sector debt –a signal of impaired private sector growth. At the start of 2026, it looked like that trend might reverse: AI promised to boost productivity growth, and tech companies were borrowing more, taking the growth burden away from governments. Regrettably, the oil shock has dashed those hopes over the short term.

The way for bond yields to fall back is for oil prices to settle back to manageable levels. That should provide yet another incentive for the US to end the war quickly, and markets are betting it will. We will have to wait and see. In the meantime, the stock market sell-off offers long-term investors an opportunity to use their end-of-tax-year liquidity to buy stocks at a relative discount. Earnings expectations have risen strongly since Christmas but index levels are back at the same prices. As the so-called Oracle of Omaha, Warren Buffett, once said in a letter to his shareholders “Price is what you pay; value is what you get. Whether we’re talking about socks or stocks, I like buying quality merchandise when it is marked down.”

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.