Market Update: A potential return to normal

Markets burst upwards on Wednesday, as the US pulled back from the precipice and announced a ceasefire with Iran. Oil prices dropped over 15% while bonds and stock prices rallied on the hope that global supply chains might quickly return to normal.

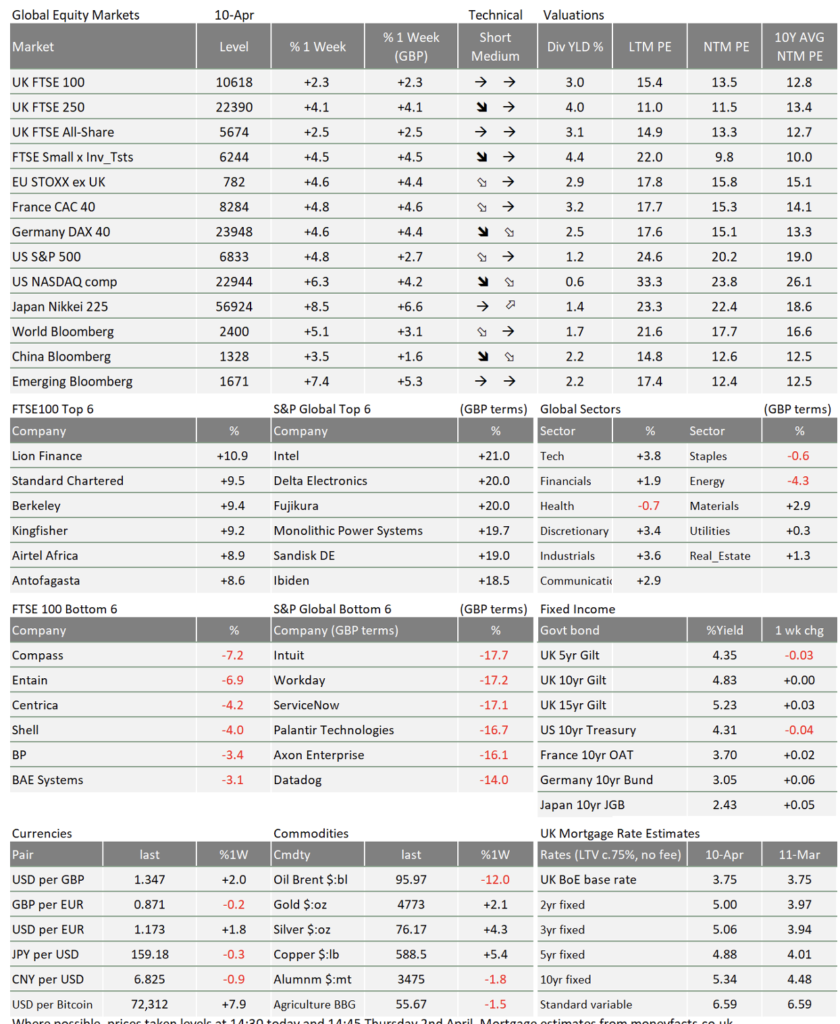

That optimism came under pressure through the rest of the week. The Strait of Hormuz remains effectively closed, while Israel places President Trump in a difficult position by continuing the attacks on Lebanon, incensing the Iranian leadership. However, although bond yields have risen slightly from the lows, equities have continued to rise and the US Dollar has fallen back against most currencies.

One cannot know definitively if this is the beginning of a lasting peace, what happens next, or the extent of the damage already done to supply chains. Markets see that we are in a better position than last week nonetheless. With analysts’ expectations of company earnings growth improving all the while, that is a fair assessment.

Ceasefire, what ceasefire?

According to the FT, fewer ships are passing through the Strait of Hormuz than before the ceasefire – a ceasefire Iran says has been violated by Israel’s strikes on Lebanon. Netanyahu’s offer of negotiations with Lebanon is still not an offer of a ceasefire. Trump, meanwhile, says the US military will remain close to Iran until they comply with “the real agreement reached”, and is demanding that NATO allies help police the Strait. Neither side can agree on what it was they agreed on, as US Vice President Vance seemed to admit himself.

Vance’s comments on the US and Iran’s “legitimate misunderstanding” and Israel’s limited offer “to check themselves a little bit” point to a growing split between the US and Israel. Either the US will pressure Israel to meaningfully halt its Lebanese assault, or the Straits will remain closed.

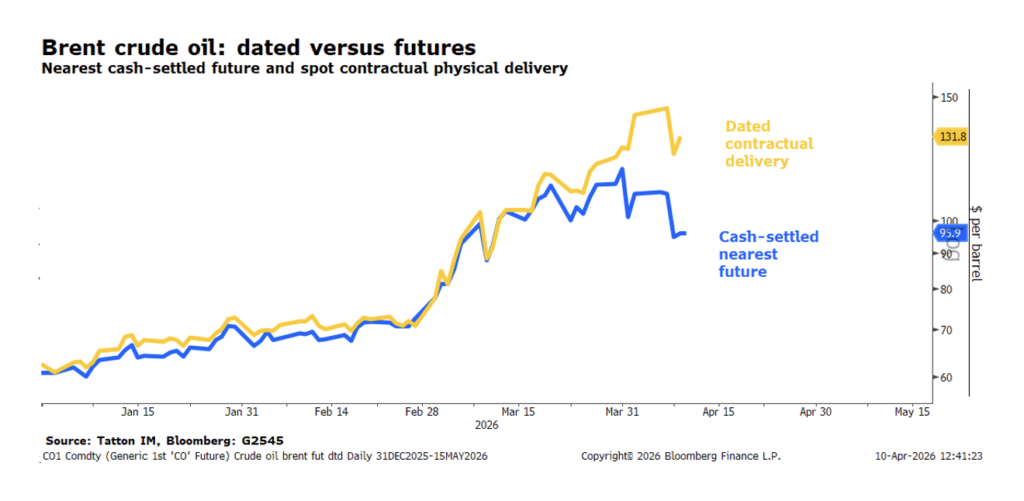

Markets might therefore be too optimistic. There is a disconnect between the relief in oil and equity markets, and the scramble for resources we see in the real economy. This is clearest in the difference between current oil prices and so-called spot dated price – which guarantee future oil delivery, a little different to a standard futures contract. The chart below shows spot dated oil price for June delivery is nearly 40% above the current near-contract futures prices, reflecting an extreme supply crunch in the next few weeks:

Even if the ceasefire holds, shipping traffic will take weeks to stabilise and limited global fertiliser supplies will have knock-on effects on food prices. Infrastructure repairs will constrain global supply chains, potentially for years. All of that points to greater inflation pressures than markets seem to realise.

Markets aren’t feeling the risks because fundamentals are so strong

You could argue that markets have been optimistic all throughout the war. March was bad for equity returns, but we never went into full bearish territory. Credit spreads (the difference between government and corporate bond yields) widened only slightly, and have already come down, showing no sign of systemic credit stress. Speculative investors sold plenty of stocks, but there was little sign of long-term ‘real money’ liquidating their holdings.

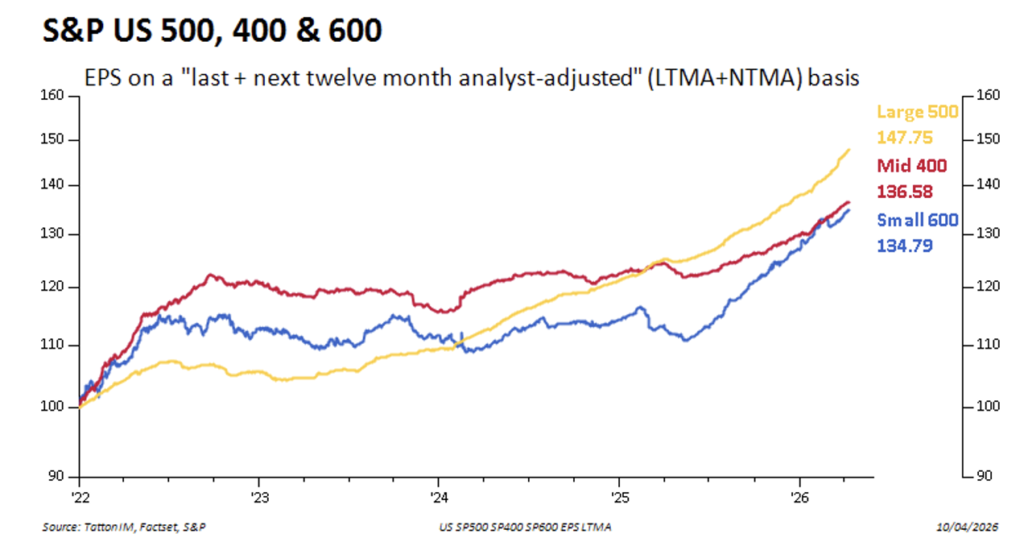

That is understandable when you look at the health of the US economy, where most of the world’s largest stocks derive most of their revenue. US citizens are angry about fuel prices and there are signs of slowing ‘real’ spending, but there is no sign of stress in the labour market data. Going into the Q1 corporate earnings season, earnings growth expectations are high. There not much evidence that companies have been hit by the war. On the contrary, growth has accelerated across small, mid and large cap companies. The chart below shows US equity indices’ earnings per share, on our favoured metric (combined last twelve month and expected next twelve month earnings, all indexed to the start of 2022):

That has helped equity price-to-earnings valuations. US stocks are currently where they were last October, but earnings growth has powered ahead. Previously, for international investors, this earnings strength was counteracted by the weakness of the dollar. But now that the dollar has strengthened, from a valuation point of view US stocks look very attractive.

Bearish or bullish on bonds is the big question

US stocks look like good value, but that is somewhat offset by higher long-term government bond yields (higher ‘risk free’ bond returns make equities less attractive by comparison). Yields have not come down as much as you might expect this week, given the strength of other assets. The danger, for the US, is that both short-term interest rates and long-term bond yields stay high – not because of a global supply shock, but because of the strength of the economy. Coupled with Trump’s clear desire to borrow more (covered in a separate article), that is a concern for US treasury bonds.

In fact, the push for extra defence spending could mean fiscal indiscipline everywhere. The UK has tried to maintain greater fiscal discipline (compared to the US) through the Chancellor’s fiscal rules, but these will be tested by next month’s local elections, which Labour are expected to lose heavily. Regardless of whether Starmer and Rachel Reeves keep their jobs, there will be pressure to change or abandon the fiscal rules.

That is not to say that yields will not come down if and when Middle Eastern tensions fade – just that falling yields are not a given. What happens to bonds will have knock-on effect on how markets deal with their previous anxieties: AI disruption and private credit woes. Given Trump’s predilection for weekend drama, we go into this weekend as worried as usual. Hopefully, that drama is building to a happy ending and, with any luck, we will be back to worrying about the old themes by May.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.