Investing in your Child’s future: Without planning ahead, the cost can be a huge money sink.

While many parents value the standard of education offered by independent schools or universities, the costs can be daunting. However, with careful planning, it may be possible to avoid a huge outstanding student loan or tax burden.

A good education will give your children or grandchildren the best start in life. With more parents choosing to opt out of state schools and educate their children privately, plus some children continuing their education into their early twenties, the costs can carry on for many years.

FINANCIAL SACRIFICE

The overall cost for just one child can end up being about the same as buying an average home in the UK. That’s a massive financial sacrifice for many parents, leading them to wonder if it’s better to pay for their child’s education or save the money to help them onto the property ladder later in life. In any case, without planning ahead, the cost can be a huge money sink or lead to further borrowing. Since 2004, private school fees have increased by 70% – at a much faster rate than inflation and UK salary growth.

Private school fees continue to rise much faster than inflation or average earnings, making it more important than ever for parents considering taking this route to plan ahead.

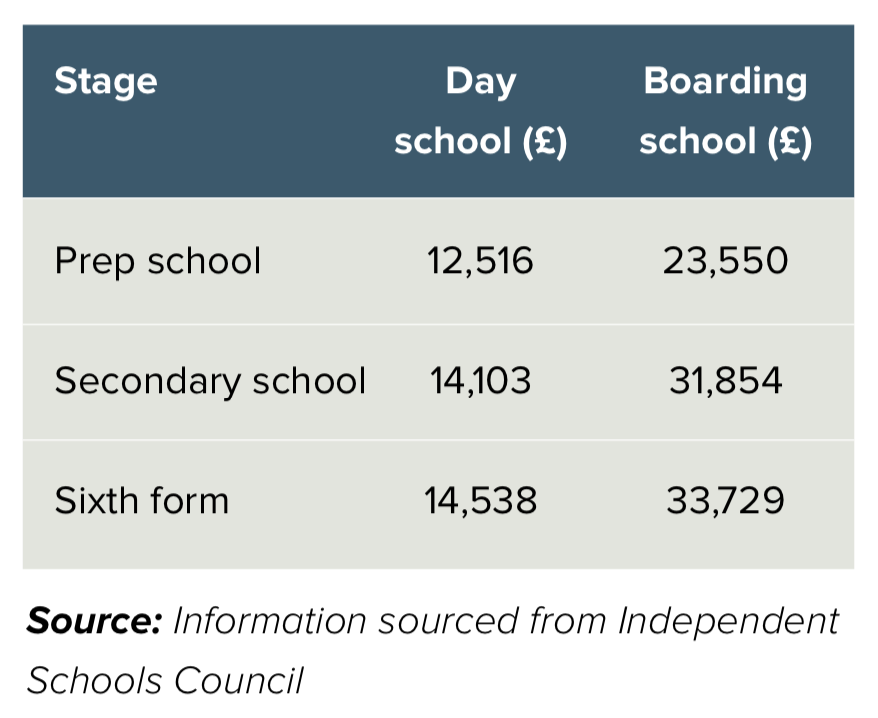

FEES BREAKDOWN TABLE:

WHAT TO CONSIDER:

Expect fees to rise– on average around 3.5% a year – Inflation, growth in salaries and increased amount of interest from wealthy families in Asia and Russia wanting to send their children to English boarding schools, mean that private education fees may continue to grow.

Don’t assume the cost will end at fees – School uniforms and regular school trips

all add up. There will be extra-curricular activities like art, drama, music, and sport to absorb as well.

Boarding can be more than double the cost of day school – By deciding not to board, annual savings of around £15,000 annually per child can be made. So, consider the location of the school, and consider whether it is feasible to commute every day or weigh up the advantages of relocating close to the chosen school.

Mixing private education with state education – Many parents are now delaying private education until secondary school to reduce the cost to below £100,000.

Planning for and researching the right school is often the exciting element, particularly when Open Days allow tours of delightful schools in bucolic surroundings. The hard work starts when analysing how the long-term annual costs are going to be paid for.

SUGGESTIONS ON HOW TO MANAGE THE COSTS:

Start planning early – put simply, the financial planning can’t start early enough, even to the extent of allocating money before any children are born. Simply paying school fee costs from current income or capital removes the ability to benefit from the 8th wonder of the world (according to Einstein), which is the magic of compounding returns.

Advance schemes – if you can afford to pay for several years in advance, you may be able to get yourself a good deal from the school. Some schools offer to put that lump sum in low-risk investments – and because of their charitable status, they’ll avoid paying capital gains tax on any returns they make. In exchange for pre-payment, a fee discount will be offered by the school. There are terms and conditions and strings attached, but this is worth investigating.

Bank of grandparents – grandparents may want to consider helping to pay for grandchildren’s school fees or additional extras such as schoolbooks, trips and uniforms. If grandparents do have the capacity to help financially, this could mean that a useful by-product could be a reduction in their own Inheritance Tax liability, along with the joy of the gift.

Discounts and scholarships – although discounts aren’t always publicised and can sometimes be discretionary, it costs nothing to ask. A lot of private schools are willing to provide discounts for enrolling multiple children or even paying fees by monthly direct debit. Always ask about any scholarships or bursaries your child might be eligible for. According to the Independent Schools’ Council, a third of children educated at a private school now receive some sort of help with fees.

GOOD ALTERNATIVE OPTION:

Private education is not a feasible option for every family, and with an excellent selection of state schools on offer, it doesn’t have to be the only good option. There are many other ways to invest in your child’s future. For example, if you invested the money you would have spent on day school fees for a full 14 years on your child’s behalf, you could provide a sum that could be used to potentially fund university, buy them a house, learn a new skill or set up their own business.

MOST VALUABLE GIFTS PARENTS OR GRANDPARENTS CAN GIVE:

Providing a good education can be one of the most valuable gifts parents or grandparents can give to children. And for those parents hoping to send their children to private school, it is essential to start working out how they will cover costs as soon as possible. To discuss your requirements, or to arrange a meeting, please contact us.

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.